Southern Company’s High Capex and Regulatory Dynamics Define Growth and Returns in 2025

Southern Company reports strong revenue growth in 2025 amidst rising regulatory scrutiny and elevated capital expenditures impacting free cash flow.

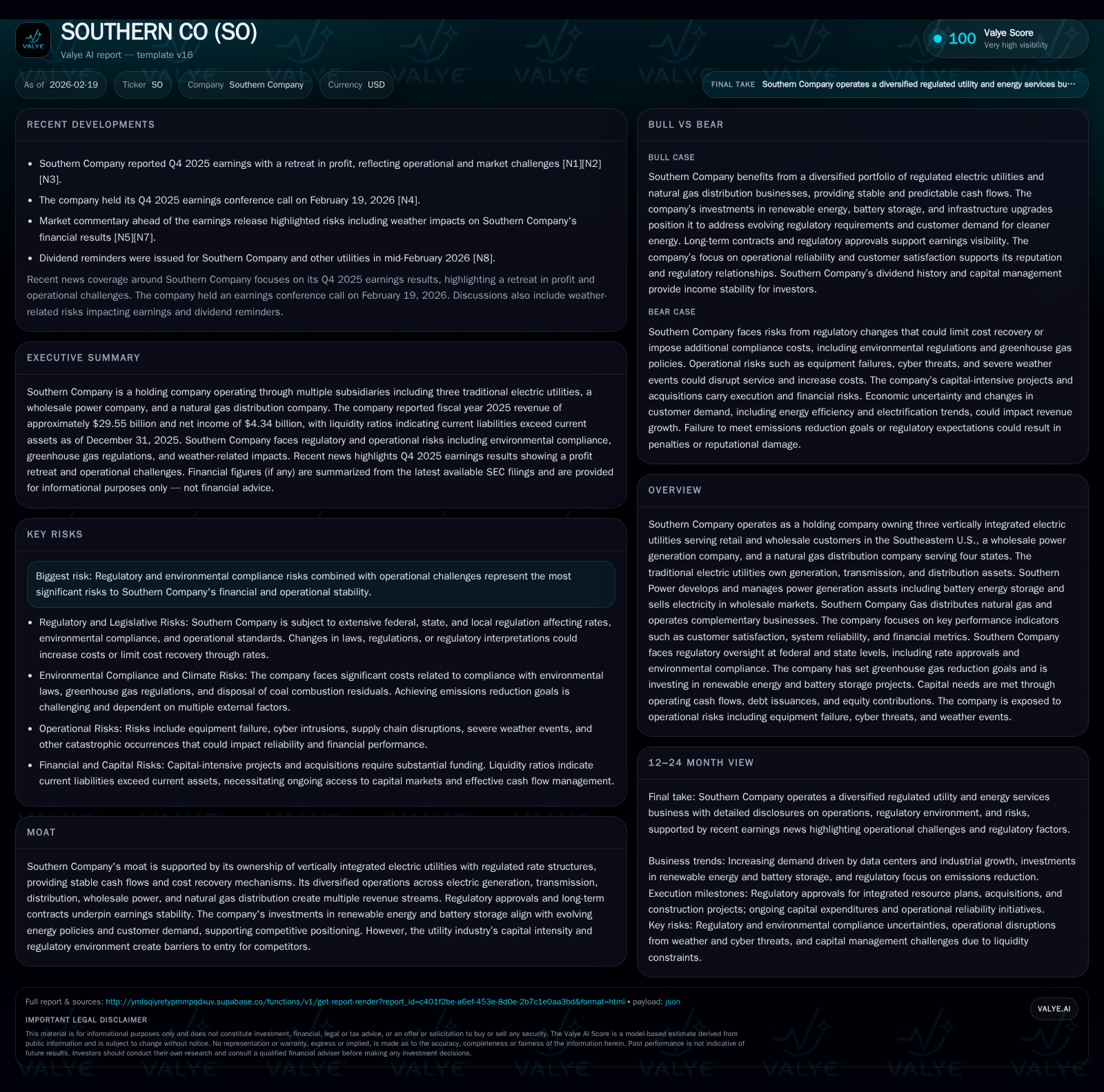

Southern Company, a vertically integrated utility holding company serving the Southeastern U.S., demonstrated a 10.6% revenue increase to $29.55 billion in 2025, driven by expanded customer contracts and wholesale power sales. Operating income rose modestly by 3.1%, while net income surged nearly ninefold year-over-year, supported by improved operational efficiencies and regulatory rate approvals. However, the company’s elevated capital spending of $12.74 billion—a 42% increase over 2024—resulted in negative free cash flow, highlighting ongoing investment demands in infrastructure and renewable integration. Regulatory risks persist as the company navigates cost recoveries amid evolving environmental compliance obligations and expanding load from large customers, especially data centers.

Company Overview

Southern Company (SO) operates as a holding company owning three vertically integrated electric utilities—Alabama Power, Georgia Power, and Mississippi Power—which serve retail and wholesale customers across the Southeastern United States. These regulated utilities own generation, transmission, and distribution assets fundamental to their business model. Complementing this is Southern Power Company, which develops, owns, and operates competitive wholesale power generation assets including battery energy storage projects sold at market-based rates.

Additionally, Southern Company Gas distributes natural gas through utilities in Illinois, Georgia, Virginia, and Tennessee while operating complementary energy businesses [S15]. Together, these segments create diversified revenue streams anchored in regulated cost recovery mechanisms that bolster the company’s moat . Southern Company also manages supporting subsidiaries such as Southern Nuclear (nuclear plant operations) and PowerSecure (distributed energy solutions).

Historical Performance Trends

Southern Company delivered consolidated revenues of $29.55 billion for fiscal year 2025, marking a robust 10.6% increase over $26.72 billion in 2024 [F1]. Operating income grew more modestly by 3.1% to $7.29 billion compared to $7.07 billion year-over-year, reflecting margin pressure from rising operating costs despite top-line expansion.

Most notably, net income soared approximately 886.6% from $436 million reported previously (2019 is the last comparable net income figure before sharp increases) to $4.34 billion in the most recent fiscal year [F1]. This substantial profitability improvement is influenced by operational gains and successful regulatory recovery strategies enabling Southern Company to recoup increased expenses through rate adjustments.

Operating cash flow showed remarkable stability at around $9.8 billion, nearly flat versus prior year despite significant revenue growth [F1]. In contrast, capital expenditures climbed sharply by over 42% from $8.95 billion to a sizeable $12.74 billion in 2025 [F1], primarily reflecting investments in new generation assets—including renewables—transmission expansions, and system upgrades tied to load growth.

The heavy capex outstripped CFO producing negative free cash flow of approximately -$2.94 billion for the first time in recent years . Equity rose steadily to $36.0 billion from $33.2 billion in one year indicating retained earnings accumulation alongside equity issuances or valuation effects [F1].

Annual Financial Snapshot

Historical performance (annual)

| FY | Rev ($bn) | CFO ($bn) | OpInc ($bn) | Capex ($bn) | Rev YoY |

|---|---|---|---|---|---|

| 2025 | 29.6 | 9.8 | 7.3 | 12.7 | +10.6% |

| 2024 | 26.7 | 9.8 | 7.1 | 9.0 | +5.8% |

| 2023 | 25.3 | 7.6 | 5.8 | 9.1 | -13.8% |

| 2022 | 29.3 | 6.3 | 5.4 | 7.9 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Net, Buybacks, ROE%. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($bn) | FCF ($bn) |

|---|---|---|

| 2025 | 3.0 | -2.9 |

| 2024 | 3.0 | 0.8 |

| 2023 | 3.0 | -1.5 |

| 2022 | 2.9 | -1.6 |

Source: SEC companyfacts cache [F1].

Drivers Behind Past Growth

The revenue uptrend reflects broad-based strength across Southern Company’s vertically integrated utilities benefiting from rising electricity demand throughout the Southeast region, supplemented by wholesale power contracts managed through Southern Power [S17]. The company has secured new large-load customer contracts—primarily data centers—that collectively account for about eight gigawatts of incremental electric load ramping up through and beyond calendar year 2028 [S13][S17]. These long-term agreements often include provisions like minimum bills and early termination fees mitigating credit risk.

On the natural gas side, Southern Company Gas sustains growth via increasing customer counts in four states enhanced by gas marketing services subject to weather-driven seasonal fluctuations [S22].

Operating margin expansion was supported by efficient performance metrics such as plant availability improvements at traditional utilities and controlled equivalent forced outage rates at Southern Power facilities [S2]. Federal Energy Regulatory Commission (FERC) oversight supports stable wholesale tariffs although market volatility remains a factor for Southern Power’s market-based sales.

Future Growth Prospects

Going forward, Southern Company appears poised for continued top-line growth anchored on several vectors:

- Expansion of electric load primarily driven by nascent data center deployments servicing AI/digital economy needs.

- Incremental industrial load increases linked to advanced manufacturing projects like electric vehicles and battery plants located within its service territories [S13].

- Ongoing buildout of renewable generation capacity and battery energy storage assets through Southern Power to meet increasing regulatory clean energy mandates as well as customer demand shifts.

- Infrastructure upgrades across transmission and distribution grids crucial for accommodating electrification trends including transportation.

- Continued growth of natural gas distribution networks barring accelerated electrification policies that could constrain demand.

However, these prospects face limitations:

- Regulatory risk persists as state public service commissions may resist approving rate increases necessary for rapid capital investment recoveries given current inflationary pressures [S5][S19].

- Environmental compliance costs remain high with requirements tightening around greenhouse gas emissions control and coal combustion residual management potentially elevating operational expenses without guaranteed cost pass-throughs [S18][S19].

- Demand projections carry inherent uncertainty: if anticipated large-load project ramps slow or contract terminations occur unexpectedly, stranded asset risk grows [S16][S21].

- Wholesale power markets expose Southern Power’s earnings to commodity pricing risk if market prices fall below forecasted levels during contract renewals or expirations [S16].

Collectively these dynamics underscore a balancing act between aggressive infrastructure expansion supporting growth versus navigating regulatory approvals ensuring cost recovery.

Forecasts & Milestones to Watch

Southern Company has outlined multi-year capital expenditure plans exceeding $14 billion at Georgia Power alone through the end of this decade focused on resource additions certified via regulatory-approved Requests for Proposals (RFPs) process designed to ensure prudency [S10]. Notably, Alabama Power received permitting approval for acquisitions that broaden its asset base enhancing retail service capacity starting calendar year 2026 [S7].

Analysts should monitor:

- Outcomes of upcoming base rate cases expected between now and early FY28 which will set allowed returns impacting profitability.

- Progress on environmental compliance projects mandated under EPA rules covering emissions reductions and coal ash landfill closures potentially creating timing mismatches between spending and recovery.

- Execution status of repowering wind projects undertaken by Southern Power representing material investment [$685M-$775M] aiming at extending operational life cycles [S10].

- Load factor realization of signed large customer contracts particularly within tech-driven sectors whose consumption patterns can be volatile.

- Short-term liquidity position relative to maturing fixed-rate bonds requiring remarketing or refinancing within next twelve months [S6][S9].

Absent explicit quantitative guidance beyond these milestones in filings or press disclosures, tracking these industry-/regulatory-linked events will offer critical insights into trajectory sustainability.

Capital Allocation & Returns Analysis

Southern Company's capital allocation reflects typical utility sector priorities emphasizing infrastructure investment complemented by shareholder distributions:

- Dividend payouts totaled approximately $3.02 billion for FY25 marginally rising versus prior year maintaining dividend consistency attractive for income-oriented investors [F1][N11][N14].

- Share repurchases have been negligible to nil over recent years limiting direct capital return via buybacks historically constrained by cash needs for capex commitments [F1].

- Capital expenditures surged materially due largely to renewable deployment projects plus grid modernization efforts causing free cash flow deficits (CFO minus Capex) amounting nearly -$2.94 billion in FY25 reflecting capex-intensive phase typical for utilities transitioning toward cleaner energy sources [F1][S10].

- Return on equity approximated at a solid ~12%, indicating healthy equity returns but balanced against growing leverage-related risk given rising debt-financed construction outlays [analysis based on net income/equity figures from F1 data].

- Liquidity benefits from robust operating cash flows nearing $9.8 billion underpin short-term working capital needs alongside substantial committed credit facilities (~$9 billion aggregated across subsidiaries) cushioning refinancing exposure related to upcoming bond maturities particularly at Alabama Power and Georgia Power units [S6][S24][S27].

This capital allocation approach aligns with regulated utility norms where sustained investment in infrastructure preserves franchise value while dividends satisfy historic shareholder expectations amidst limited share repurchase activity.

Industry Context & Sector Nuance Analysis

The Southeastern U.S., characterized by growing population density combined with expanding digital economy nodes such as hyperscale data centers representing concentrated megawatts demand clusters (upwards of hundreds of MW per center), creates a unique growth locus compared with more mature Northeast or West Coast markets [analysis; sourced from S13,S17 insights]. The challenge lies not only in scaling generation capacity but also grid resilience amid increased climate-induced storm risks affecting system reliability metrics critical under state PSC performance reviews.

Moreover, transmission planning complexities escalate given long lead times for grid hardening investments required prior to meaningful renewable integration—coupled with heightened stakeholder activism influencing siting delays creating potential 'regulatory lag' impacting financial recovery timelines for invested assets.

On the financial engineering front typical regulated returns on equity hover near mid-teens percentages justifying heavy capital expenditures balanced against incremental revenue assurances embedded within long-term rate case structures incorporating formula adjustments for inflationary cost passes plus environmental surcharges ensuring reasonable risk mitigation compared with merchant power producers exposed fully to market price fluctuations.

Southern Company's mix of regulated utility cash flows combined with market-based wholesale power segments provides diversification yet requires careful hedging especially around integrating intermittent wind/solar resource variability using battery energy storage systems—a fast-evolving domain attracting increasing technological scrutiny regarding competitiveness under changing Federal tax credit regimes and grid services markets pricing methodologies.

Conclusion

Southern Company's fiscal results for FY25 demonstrate its effectiveness capturing growth opportunities amid an intensifying capital investment cycle necessitated by expanding customer demands—especially from technology-intense industries—and tightening environmental rules driving higher compliance costs.[F1][S5][N9] The company's ability to sustain returns above cost of equity (~12%) benefits from vertically integrated rate-regulated franchises providing a defensive moat reinforced through state oversight allowing timely cost pass-through mechanisms.

Nonetheless, challenges remain salient around managing liquidity under negative free cash flow conditions amid record capex phases plus navigating potential shifts in regulatory acceptance amid affordability concerns heightened under inflationary cost pressures alongside evolving legislation related to carbon reduction targets.[S18]

Monitoring forthcoming rate case decisions across principal jurisdictions alongside milestones related to large industrial contract ramp-ups will provide clear indicators regarding Southern Company's capacity both to finance future infrastructure buildouts prudently and maintain its role supplying reliable power while transitioning toward clean energy configurations adapted for a rapidly digitizing Southeastern economy.

Disclaimer: This analysis is based on information publicly available as of February 19, 2026 including SEC filings and news reports provided herein; no forward-looking guarantees are implied.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments