Bausch Health’s Return to Profitability Highlights Shifts in Segment Performance and Capital Management

An appraisal of Bausch Health's financial rebound driven by Salix revenue growth amid ongoing clinical development and evolving balance sheet dynamics.

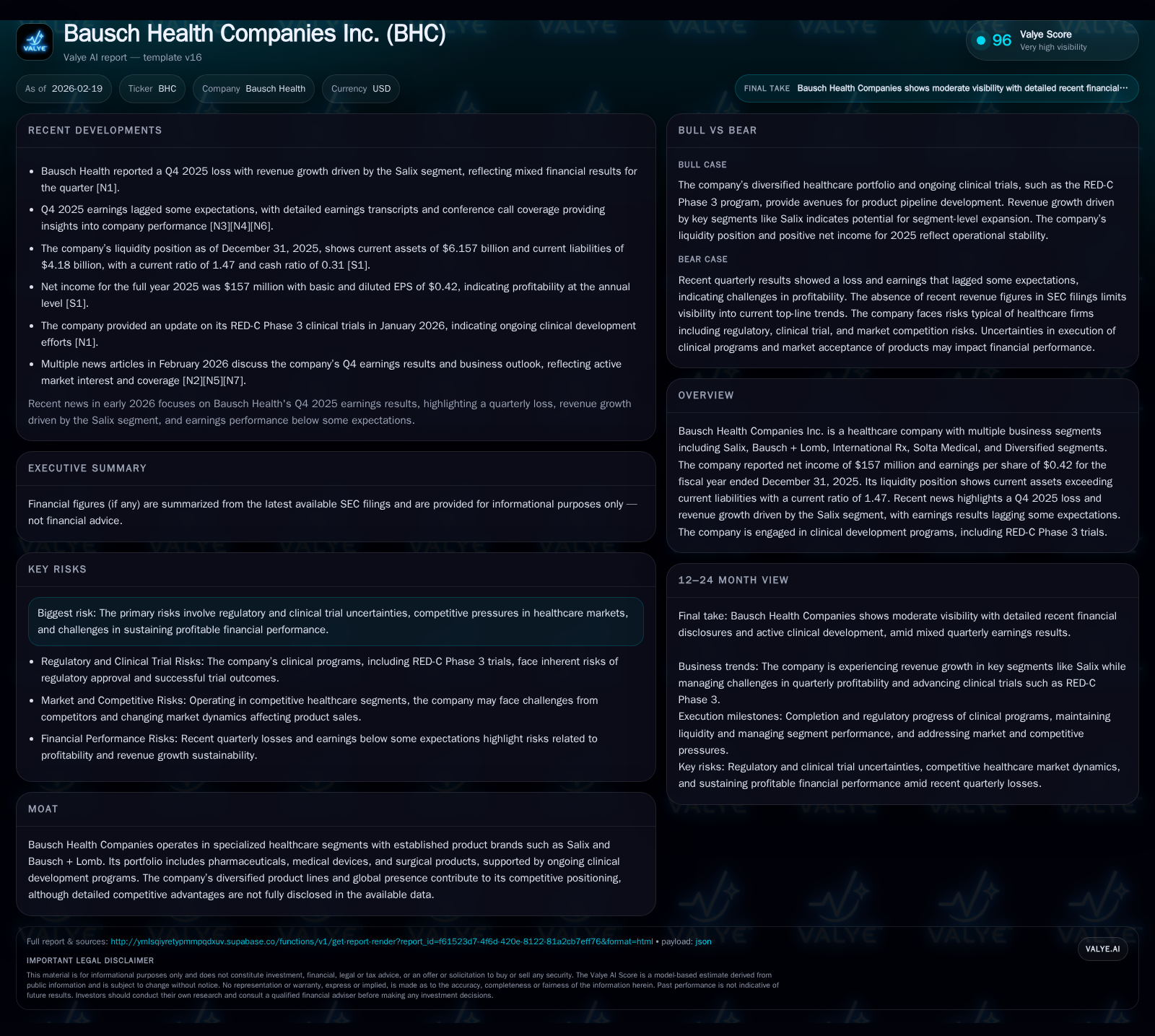

Bausch Health Companies Inc. concluded fiscal 2025 with a notable turnaround to profitability, reflecting a 441% year-over-year net income increase despite a challenging Q4 earnings miss. The Salix segment emerged as a critical revenue growth engine, offsetting softness in other businesses while the company progresses its RED-C Phase 3 clinical trials. Its capital structure shows improving liquidity and active debt management, though negative equity underscores continued leverage risks. Key future performance drivers hinge on clinical milestones, regulatory approvals, and effective capital allocation to sustain momentum.

From Loss to Profit: Bausch Health’s Progressive Financial Turnaround

The fiscal trajectory of Bausch Health Companies Inc. over recent years exhibits a compelling recovery arc culminating in profitability for the full year ended December 31, 2025. After consecutive years burdened by net losses — $225 million in 2022, expanding to $592 million in 2023 and narrowing to a $46 million loss in 2024 — the company achieved a $157 million net profit in FY2025, a striking 441% year-over-year improvement [F1]. Operating income margins also expanded significantly from $454 million in FY2022 to $1.81 billion in FY2025, representing a robust compound uplift exemplifying improved operational efficiency.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 157 | 1400 | 1813 | 397 | +441.3% |

| 2024 | -46 | 1597 | 1546 | 337 | +92.2% |

| 2023 | -592 | 1032 | 963 | 215 | -163.1% |

| 2022 | -225 | -728 | 454 | 218 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 1003 | -28.3 |

| 2024 | 1260 | 3.6 |

| 2023 | 817 | 57.9 |

| 2022 | -946 | 32.5 |

Source: SEC companyfacts cache [F1].

*Latest full-year revenue data available from public snapshots; full FY figures pending.

This rebound is emblematic of both structural realignment across business segments and tactical cost discipline acting upon the portfolio.

Salix Segment: The Key Driver Behind Recent Revenue Expansion

The Salix segment has been decisive for Bausch Health’s revenue growth narrative in FY2025, as recent earnings releases underscore [N1][N3][S1]. Specializing in gastrointestinal pharmaceuticals with established branded products, Salix leverages a favorable reimbursement environment and potential new product launches that have fueled top-line increases despite broader market headwinds.

Pharmaceutical sales growth within Salix benefits from reformulated drugs delivering extended patent protections and managed care contracts improving payer coverage — key nuances enhancing revenue sustainability beyond commodity generics competition absent here. This specialized unit’s ability to offset underperformance in other segments demonstrates effective portfolio balancing through focused therapeutic verticals.

Clinical Pipeline Focus: RED-C Phase 3 Trials and Their Market Implications

At the heart of Bausch Health's R&D efforts stands the RED-C Phase 3 clinical trials program—a crucial developmental milestone publicly disclosed for its potential to unlock novel treatment avenues [N1][S1]. Within pharmaceutical development lexicon, reaching Phase 3 denotes significant regulatory gatekeeping where safety, efficacy, and large patient datasets become paramount.

The trial outcomes pose traditional biotech binary risks: successful readouts can catalyze valuation uplifts via approval pathways while delays or failures weigh heavily on investor sentiment and pipeline valuation metrics. As such, RED-C functions as both an innovation fulcrum and risk vector shaping medium-term growth trajectories.

Segmental Diversification: Insights into Bausch + Lomb, International Rx, and Solta Medical

Bausch Health maintains diversified operations including the Bausch + Lomb vision care segment; International Rx focusing on pharmaceutical distribution across geographies; plus Solta Medical providing aesthetic medical devices [S17][S24][S25]. These segments collectively underpin geographic reach split between North America, Europe, emerging markets, and specialty channels.

While diversification offers natural hedging against single-market downturns or regulatory disruptions, differential currency exposures and reimbursement regimes introduce volatility vectors unique to each region’s health system architecture—e.g., disparities between U.S., EU centralized regulatory frameworks versus emerging markets’ heterogeneous controls.

Operationally, these segments exhibited mixed results with some pressure from competitive branded generics encroachment dampening margin expansion relative to Salix’s pharmaceutical gains [F1]. This interplay highlights the importance of portfolio composition appraisal when assessing sustainability of consolidated financial performance.

Capital Structure Analysis: Debt Profile and Liquidity Position as of 2025 Year-End

A critical dimension for Bausch Health surrounds its leveraged capital structure which continues to feature substantial indebtedness balanced against improving liquidity parameters [F1]. As of December 31, 2025, the company presented current assets at $6.16 billion against current liabilities of $4.18 billion yielding a current ratio of approximately 1.47—indicative of adequate near-term liquidity buffers.

Longer tenor debt largely consists of secured credit facilities with maturities staggered through January 2031 inclusive of revolving credit lines due mid-2030 and incremental term loan tranches allowing phased refinancing opportunities . Average interest costs include floating SOFR/EURIBOR-linked rates reflective of post-LIBOR benchmark transition typical within healthcare leveraged credit deals.

Covenant headroom appears sufficient given positive operating cash flows near $1.4 billion although negative equity (~-$554 million) signals residual balance sheet leverage risk warranting monitoring especially around covenant testing windows expressed typically on quarterly filings.

Navigating Regulatory Risks and Market Competition Amid Product Innovation

Regulatory environments impose consistent risks for Bausch Health given intricate FDA submission workflows compounded by intellectual property challenges such as Paragraph IV litigations noted historically within key brands like Xifaxan [S19][N3]. Approval timelines can be protracted affecting commercialization windows thereby influencing earnings visibility.

Additionally, increasing competition from biosimilars pressures pricing structures requiring strategic lifecycle management within pharmaceutical units while device-oriented segments face evolving compliance standards coupled with tightened reimbursement protocols impacting gross margins.

These factors collectively underscore the nuanced operational landscape where innovation must be aligned tightly with regulatory strategy to safeguard long-term market positions without excessive exposure to pipeline disruptions.

Future Outlook: Factors to Watch Beyond Reported Guidance

Without explicit fiscal guidance disclosed recently, stakeholders should keenly observe critical trajectory gating events including upcoming trial readouts from RED-C programs as well as planned debt refinancing or maturity extensions championed by treasury functions [N8].

Earnings season commentary may reveal incremental cues about segment ramp-ups or investment pivots particularly concerning new product launches within Salix or emerging market expansions that could swing revenue trajectories materially.

These inflection points serve as barometers for capital markets assessing sustained profitability restoration versus episodic performance fluctuations typical at mid-cycle biotech commercialization crossroads.

Returns to Shareholders: Dividends, Buybacks, and Free Cash Flow Trends

Capital allocation history at Bausch Health shows restrained shareholder distributions given legacy deleveraging priorities with no significant share repurchases or dividend payouts evidenced recently [F1][S28]. Operating cash flow generation remains healthy at approximately $1.4 billion yet investment activity maintains elevated capital expenditure outlays near $397 million earmarked for capacity expansion and technology upgrades.

The resultant free cash flow approximates $1 billion sustaining potential liquidity cushions underpinning gradual deleveraging initiatives without immediate shareholder return augmentation.

Return on equity remains negative (-28%) dragged down by residual book equity deficits; however positive operational cash metrics suggest management focus remains predominantly on balance sheet repair over yield enhancements currently.

This analysis is intended solely for informational purposes summarizing Bausch Health Companies Inc.'s historical financial performance, segment dynamics, capital structure position, risks factors, and outlook considerations based exclusively on publicly available filings and news disclosures as of February 19, 2026. This does not constitute investment advice or recommendations regarding any security or financial instrument related to the discussed entity.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments