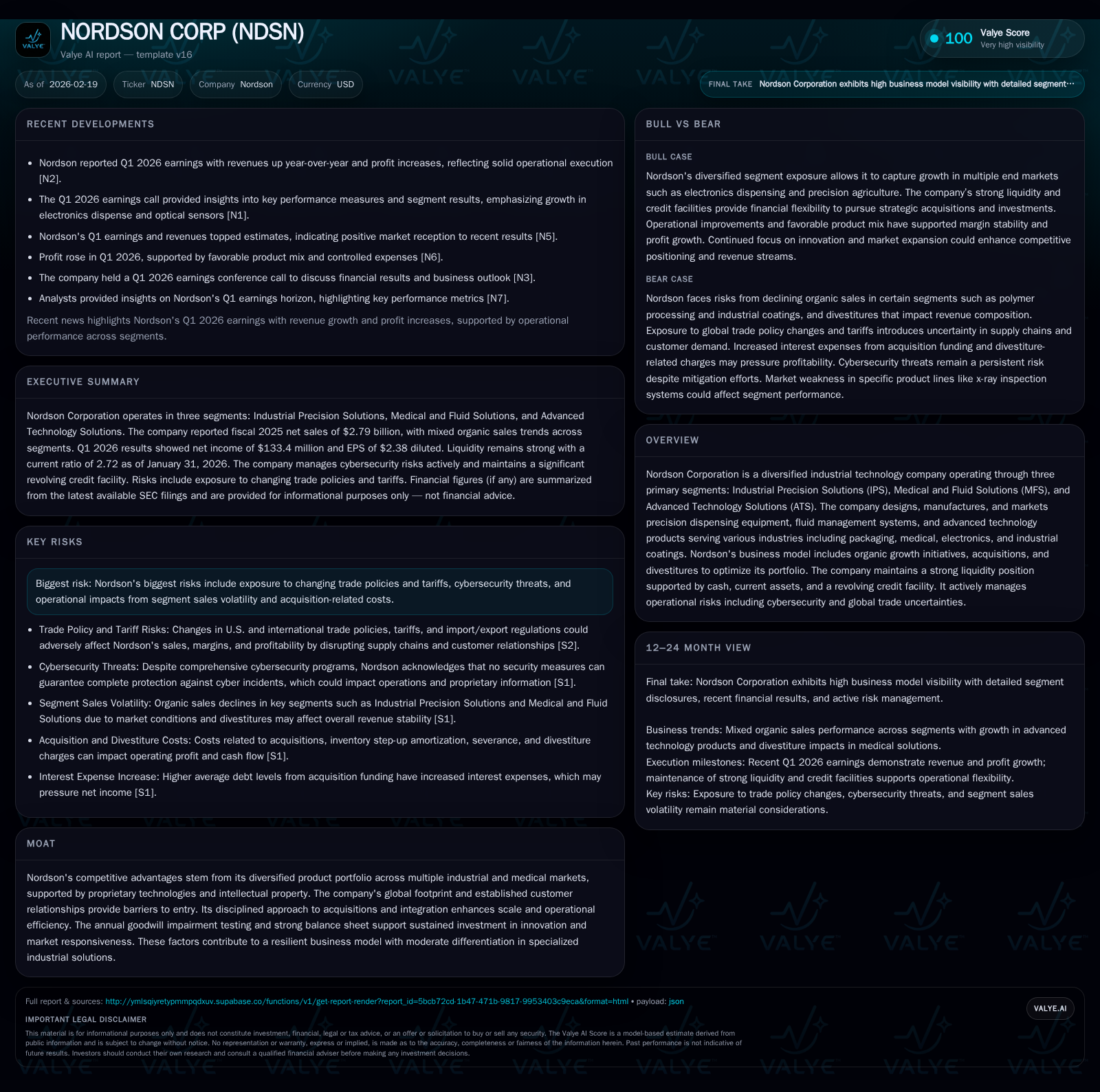

Nordson Extends Precision Solutions Leadership with Steady Earnings and Aggressive Buybacks

Nordson’s multi-segment industrial technology platform delivers resilient financial results supported by strong cash flow and disciplined capital allocation.

Nordson Corporation continues to solidify its position in precision dispensing and fluid management technologies through consistent revenue and earnings growth. The company's diversified Industrial Precision, Medical Fluid, and Advanced Technology segments contribute to a steady operating income expansion despite macroeconomic headwinds. Robust free cash flow generation underpins substantial share repurchases and dividend growth, reflecting disciplined capital deployment. Operational risks remain focused on trade uncertainty and cybersecurity, but Nordson’s strategic innovation investments and longstanding customer relationships maintain its competitive edge.

Historical Financial Performance: Robust Growth Across Segments

Nordson Corporation's fiscal 2025 performance showcased steady expansion in operating profitability alongside moderate net income growth. Total operating income increased by 5.6% year-over-year to approximately $711.7 million from $674.0 million in 2024 [F1], reflecting effective cost controls despite acquisition-related expenses.

Net income rose by 3.7% to $484.5 million, aided by a favorable tax rate shift and ongoing share repurchases enhancing EPS metrics [F1][S15]. Revenue growth was more nuanced; overall sales increased 3.8% primarily buoyed by inorganic contributions and currency effects amid slight organic softness in Industrial Precision Solutions.

Inventory step-up amortization and acquisition costs decreased relative to previous years, contributing to improved margins at the consolidated level [S14][S15]. Operating cash flow rose robustly by nearly 30%, providing a healthy buffer for both capital expenditures and shareholder distributions.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 484 | 719 | 712 | 58 | +3.7% |

| 2024 | 467 | 556 | 674 | 64 | -4.1% |

| 2023 | 487 | 641 | 673 | 35 | -5.0% |

| 2022 | 513 | 513 | 702 | 51 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 179 | 306 | 661 |

| 2024 | 161 | 33 | 492 |

| 2023 | 150 | 90 | 607 |

| 2022 | 126 | 263 | 462 |

Source: SEC companyfacts cache [F1].

Note: Capex figures for FY2018 unavailable; Operating income and net income for FY2018 not provided.

Drivers Behind Nordson’s Continued Operating Income Expansion

Nordson’s disciplined business model focuses heavily on proprietary innovations within precision dispensing technologies that serve diverse markets such as packaging, medical devices, electronics manufacturing, and industrial coatings [S11]. This specialization enables premium pricing power supported by intellectual property protections that collectively sustain margin expansion even amid raw material cost pressures.

The company's global footprint allows it to leverage production efficiencies while remaining close to key customers worldwide—an important factor given varying regional demand dynamics.

Management's acquisition strategy demonstrates integration synergies that progressively reduce overheads and improve cross-segment operational leverage [S1]. Strategic revenue recognition policies also ensure stable earnings visibility amidst short-term contract variations typical in fixed-price manufacturing environments.

Segment-Specific Outlook: Industrial Precision, Medical Fluid, & Advanced Technologies

The Industrial Precision Solutions (IPS) segment saw a modest revenue decline of around -4.8%, largely due to softness in polymer processing and industrial coatings lines offset by areas like precision agriculture and packaging which showed resilience [S19]. Meanwhile, Medical and Fluid Solutions (MFS) grew strongly (+20%) fueled by bolt-on acquisitions such as Atrion boosting market share even as organic sales saw slight declines related to divested contract manufacturing components [N1][N4].

Advanced Technology Solutions (ATS), focused on electronics dispensing products and optical sensors, returned to growth with a ~5% increase supported by gains in electronic processing though tempered partially by weaker x-ray inspection demand [N13][S19].

Organic growth initiatives remain prioritized across all segments but are balanced carefully against ongoing geopolitical challenges that temper capital expenditure decisions among end markets.

Operational Risks: Trade Policy Uncertainty and Cybersecurity Vigilance

Nordson continues navigating a complex risk landscape including variability in global trade policies, tariffs impacting supply chains, and currency fluctuations that can influence margins adversely [S6][S17]. Its exposure is mitigated somewhat through diversified geographies—with approximately two-thirds of sales generated outside the U.S.—but remains a concern given variable regulatory environments.

Cybersecurity threats pose increasing risks especially given the company’s extensive R&D efforts that rely on protecting intellectual property assets from infiltration or data breaches [S22]. Executive leadership actively oversees these areas via regular board committee reviews incorporating defensive protocols aligned with industry frameworks led by seasoned IT executives.

Capital Allocation Discipline: Buybacks, Dividends, and Debt Management

Reflecting strong free cash flow generation capacity, Nordson sharply escalated share repurchases in FY25 with approximately $306 million spent compared to $33 million the prior year—a near tenfold increase emphasizing value returned directly to shareholders alongside dividends totaling $179 million (up from $161 million in FY24) [F1][S29].

Leverage ratios remain well within covenant bounds supported by a robust liquidity profile including $120 million+ cash on hand plus credit facilities exceeding $1 billion recently extended through January 2031 providing significant borrowing flexibility if needed [S4][S16]. Debt reductions also proceeded via term loan repayments totaling around $224 million during FY25 evidencing proactive balance sheet management.

Cash Flow Strength Enabling Investment in Innovation and Capacity

Strong operational cash flows reached nearly $720 million last fiscal year marking a significant increase of approximately +29% versus the prior year which underscores Nordson's ability to self-finance both internal development projects and selective acquisitions without excessive external dependencies.

Capital expenditures moderated slightly (-9.9%) yet remain focused not only on maintenance but also innovation-driven process automation upgrades supporting future productivity gains—reflecting prudent capital intensity relative to sector peers managing plant floor technological advancements [F1][S8].

Key Metrics to Monitor: Revenue Trends, Margins, and Free Cash Flow

Forward-looking indicators include quarterly revenue trajectories within each segment against macroeconomic sentiment shifts especially order backlog health which can signal near-term demand strength or stress points [N1][N13]. Operating margin sustainability is critical amid inflationary cost pressures while any deviation may indicate challenges preserving incremental returns following acquisitions.

Moreover integration milestones related to recent additions like Atrion should be assessed closely for evidence of expected synergy realization lowering overhead burdens further [S2]. Currency fluctuations will also remain an external factor influencing reported financials alongside raw material supply tightness scenarios common in precision equipment manufacturing supply chains.

Nordson’s Moat: Intellectual Property and Long-Term Customer Relationships

The core of Nordson’s competitive advantage resides in its extensive portfolio of patents across precision dispensing systems designed for multiple industries where accuracy and reliability are paramount—factors difficult for new entrants to replicate swiftly without substantial R&D investment commitments [F1] [(valye_report_excerpt)].

Longstanding relationships with global OEMs generate recurring revenues often embedded deep within manufacturing processes where switching costs create further client lock-in sustaining defensibility amid competition.

This intellectual property fortress combined with multi-industry diversification yields predictable revenue streams that justify valuation premiums reflective of quality industrial technology platforms.

Conclusion: Balancing Growth Prospects with Operational and Market Risks

Nordson exhibits a well-calibrated approach balancing organic investment initiatives alongside opportunistic acquisitions aimed at expanding addressable markets within its precision solutions portfolio — anchored on robust free cash flow utilization supporting shareholder returns through dividends and buybacks.

Nevertheless, vigilance towards external risk factors linked principally to trade policy volatility alongside evolving cybersecurity threat landscapes remains paramount for sustained financial performance integrity [N2][S18]. Future monitoring should emphasize execution against integration plans paired with maintaining technological leadership amidst competitive advances.

This analysis is intended solely for informational purposes based on publicly available data as of early 2026; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments