Choice Hotels' Leverage and Brand Expansion Ambitions Shape 2025 Financial Outcomes

Choice Hotels leverages a diversified franchising portfolio and strategic owned hotel initiatives to drive growth while managing debt and shareholder returns.

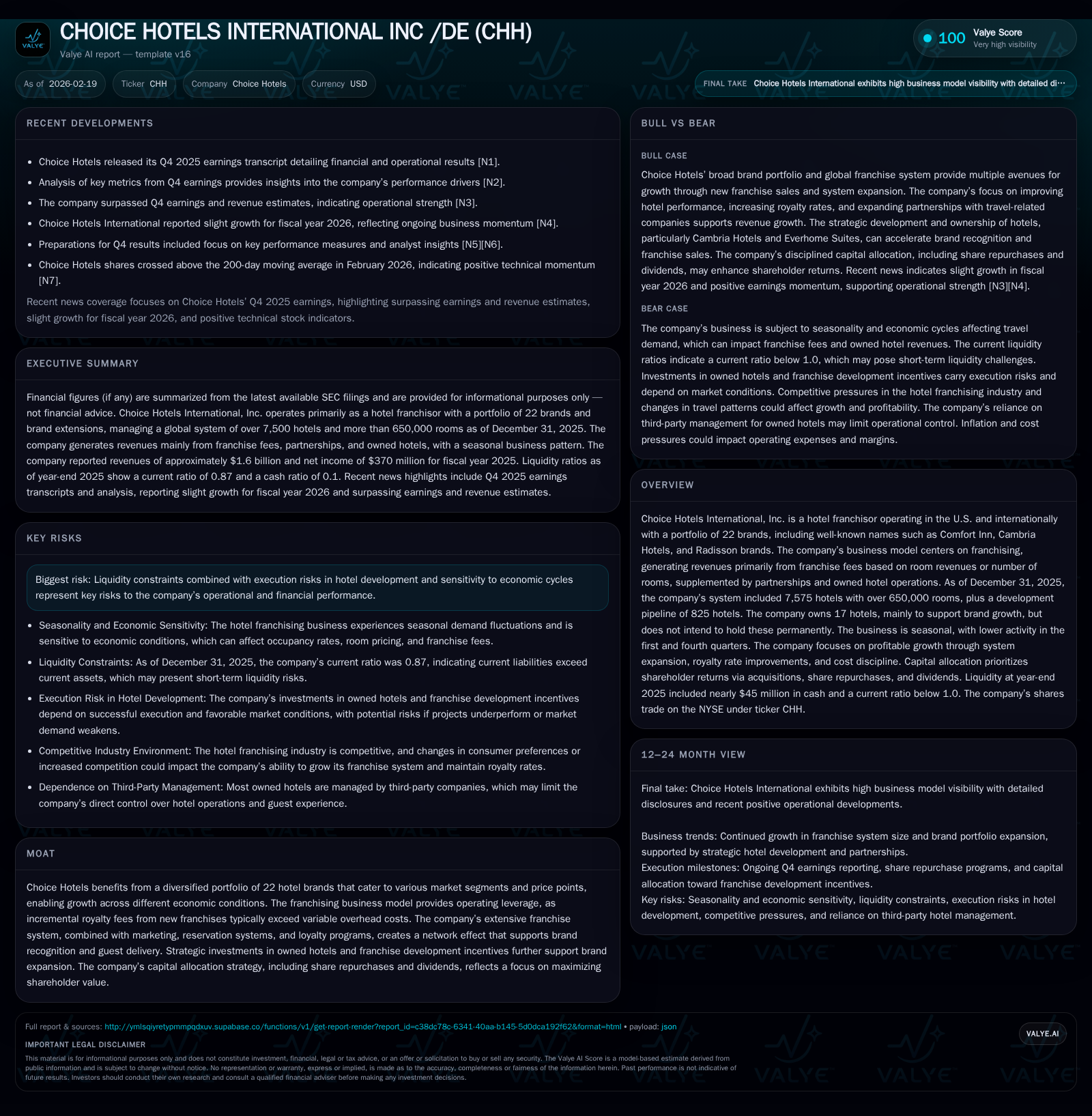

Choice Hotels International, Inc. operates primarily through franchising with a substantial portfolio of 22 brands and maintains owned hotels to support brand presence, focusing on Cambria and Everhome Suites. The company posted modest revenue growth of 0.8% in 2025, driven by franchise fees and partnership services, though operating income slightly declined by 3.3%. Net income grew significantly by 23.5%, supported by efficient capital allocation and tax impacts. Choice's balance sheet reflects substantial long-term debt, including a $600 million note due 2034 and revolving credit facilities, but remains compliant with covenants. Capital allocation priorities include dividends, share repurchases, and franchise development investments totaling over $667 million in brand support activities. Future growth will depend on franchise system expansion, development incentives, and economic conditions impacting the lodging sector.

Company Overview

Choice Hotels International operates as a major hotel franchisor across the U.S. and international markets with a broad portfolio of 22 brands ranging from economy to upper-midscale segments, including Comfort Inn, Cambria Hotels, Radisson Blu, RED, and Everhome Suites. The company’s core revenues derive from franchise fees based on room sales or fixed fees per room as well as ancillary partnership services. As of the end of 2025, Choice managed an extensive system with over 7,500 hotels representing over 650,000 rooms plus a development pipeline encompassing more than 800 additional properties [S1][N1].

Choice also owns a limited portfolio of hotels (17 at the end of 2025), concentrated mainly around Cambria Hotels and Everhome Suites brands aimed at accelerating brand presence in key markets and enhancing franchise appeal [S1][S17]. These assets are not intended for permanent holdings but serve strategic purposes supporting franchising growth ambitions.

Historical Financial Performance

The company’s historical financial trajectory through FY2022-25 shows steady top-line expansion driven by franchise system growth and steady fee income diversification:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1597 | 370 | 270 | 448 | +0.8% | +23.5% |

| 2024 | 1585 | 300 | 319 | 464 | +2.6% | +15.9% |

| 2023 | 1544 | 259 | 297 | 375 | +10.1% | -22.2% |

| 2022 | 1402 | 332 | 367 | 479 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 53 | 138 | 204.1 |

| 2024 | 55 | 381 | -661.9 |

| 2023 | 56 | 363 | 726.2 |

| 2022 | 53 | 435 | 214.8 |

Source: SEC companyfacts cache [F1].

Note: Key capital structure metrics including equity were volatile; FY2024 showed negative equity impacted by acquisitions or accounting adjustments [F1].

Revenue growth slowed considerably in FY2025 compared to prior years reflecting macroeconomic pressures on travel demand but benefitted from expanded franchise fees and partnership business lines [N1][S1]. Operating income saw a modest contraction tied partly to increased expenses associated with owned hotel operations and incentive programs.

However, net income rebounded strongly aided by favorable tax treatments and reduced non-operating charges [F1][S21]. Operating cash flow declined mainly due to working capital timing and one-off tax installments but remained positive supporting investment activities.

Strategic Owned Hotel Portfolio

Choice continues investing selectively in owned hotels predominantly under the Cambria Hotels and Everhome Suites banners to catalyze branded growth in targeted U.S markets [S1][N13]. These assets underpin the company’s efforts to enhance brand awareness, boost guest loyalty and embed superior guest experience models.

Owned hotel operations are mostly managed by third-party operators except for four properties under internal oversight, emphasizing cost efficiency through performance tracking rather than direct management expansion [S1].

Approximately $667 million was outstanding on investments supporting these efforts as of end-2025; management aims to recycle such investments roughly every five years via dispositions to franchisees under long-term agreements [S24]. This strategy balances asset-light franchising scalability with strategic brand footprint control.

Industry Context Analysis

The hotel franchising model benefits from operating leverage as incremental royalty fees largely fall through after fixed overhead coverage—a fact Choice exploits across its differentiated brand tiers catering from economy stays up to upscale options.

Notably, inflationary trends pose risks to margins but also allow rate enhancements which Choice monitors closely given the sensitivity of consumer discretionary travel spend.

Franchise development incentives are common competitive tactics given the capital-intensive nature of new hotel construction amid fluctuating lending environments—Choice’s sizeable outlays here underscore its commitment to sustained system growth [S24].

Debt Profile & Liquidity

Choice maintains substantial long-term debt obligations yet demonstrates prudent covenant compliance and liquidity management:

- Outstanding long-term debt totaled approximately $1.9 billion as of December 31, 2025, consisting of senior unsecured notes maturing between 2029-2034 ($400M in 2019 Notes; $450M in 2020 Notes; $600M recent Senior Notes), complemented by about $470 million outstanding under its revolving credit facility [S6][S18][F1].

- The total leverage ratio stood at a moderate 2.86x below covenant thresholds (max covenant ~4.5x–5.5x) ensuring continued access to capital markets at investment-grade ratings [S4][S6][S18].

- Available liquidity included roughly $57 million cash plus undrawn capacity under the $1 billion revolver enabling flexibility for capital needs ranging from debt refinancing to share repurchases or acquisitions [S8][F1].

- Short-term debt maturities are minimal with major obligations from notes scheduled beyond five years providing ample refinancing runway [S18].

This structure supports balanced risk while funding shareholder returns alongside strategic brand investments.

Capital Allocation & Returns

Choice follows a disciplined approach balancing shareholder returns with reinvestment:

- Paid annual dividends aggregating approximately $53 million ($1.15 per share) during FY2025 consistent with prior years; dividend sustainability governed by board discretion intertwined with credit agreement restrictions during default scenarios [S9][S16].

- Executed share repurchases totaling about $138 million in FY2025 following elevated buyback volumes in prior years; remaining authorization permits further repurchases signaling ongoing capital return focus despite macro uncertainty [S9][S25].

- Franchise agreement acquisition costs deployed strategically as incentives amounted substantially fueling new franchise contracts across key brands like Cambria and Everhome Suites [S24].

- Operating cash flows continue exceeding capex outlays significantly (estimated free cash flow roughly $213 million), endorsing robust internal funding capabilities despite near-term fluctuations in trading volumes or expenses [F1].

Return on equity based on latest net income relative to reported stockholders’ equity is inflated (~204%) due largely to negative equity periods influenced by non-operating factors such as acquisition accounting adjustments rather than purely operational efficiency—caution warranted interpreting ROE amid these structural considerations [F1].

Growth Prospects & Monitoring Points

Key near-to-medium term drivers include:

- Continued expansion of franchise system via organic development incentivized through capital support programs tied especially to midscale/upscale brands Cambria Hotels and Everhome Suites potentially adding hundreds of rooms annually as development pipelines mature [N13][S24].

- Improvement or stabilization of royalty fee yield per room counterbalancing incremental costs associated with owned hotel support functions.

- Broader macroeconomic conditions impacting travel demand elasticity including inflation-adjusted room rate acceptance.

- Execution quality on brand positioning, marketing efficiency leveraging network effects from superior reservation technology platforms and loyalty programs maintaining competitive advantage versus peers.

- Debt servicing costs sensitive to interest rate volatility requiring ongoing financial discipline given sizable fixed charge commitments.

Absent explicit guidance updates post-FY2025 filings, observers should monitor Q1-Q2 metrics around new franchise awards issued rate, owned hotel occupancy/profitability normalization post-recent developments, covenant compliance indicators amid evolving economic cycles, plus any adjustments in share repurchase authorizations or dividend policies signaling shifts in capital deployment preference [N11][N12][S9].

Risks Summary

Principal risks confronting Choice comprise:

- Economic sensitivity inherent in discretionary travel sectors which could constrain demand or delay new franchise builds.

- Execution complexities related to newly developed owned hotels acting sometimes as incubators for new brands demanding sustained operational expertise.

- Liquidity constraints emerging from aggressive share buybacks or escalated debt levels potentially constraining financial flexibility if adverse market shocks occur unexpectedly.

- Competitive pressures nationwide from other large-scale franchisors exerting pricing/incentive wars diminishing fee margins.

- Technological disruptions or cybersecurity risks that could impair reservation systems or guest data integrity threatening reputation [S1][S27].

Conclusion

Choice Hotels International balances a robust portfolio-driven franchise model augmented by selective owned-hotel investments within an overarching framework of conservative leverage management and shareholder value maximization through dividends plus buybacks. While revenue growth moderated recently amidst cost headwinds reducing operating margin slightly, net profitability gains alongside significant strategic capital deployment reveal adaptability within competitive lodging markets marked by inflationary pressures and shifting consumer trends. The company's large-scale system footprint combined with ongoing brand development incentives lay groundwork for future moderate expansion contingent upon economic cycles supporting discretionary travel recovery. Debt maturity profiles coupled with significant revolver capacity ensure financial resilience pending continued compliance with covenants while allowing optionality on investments or repurchases. Monitoring future quarterly updates for development pipeline progress alongside evolving macro hospitality dynamics will signal trajectory shifts essential for stakeholders analyzing Choice's operational vitality beyond headline earnings stats.

This analysis is based solely on publicly available financial disclosures as referenced herein and does not constitute investment advice or recommendations regarding CHOICE HOTELS INTERNATIONAL INC /DE (CHH). Readers should consider multiple data sources before drawing conclusions about the company's prospects or financial position.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments