OPENLANE’s Strategic Technology Transformation Challenges Growth and Profitability in Automotive Remarketing

The company balances significant IT investments and competitive pressures amidst evolving used vehicle market dynamics.

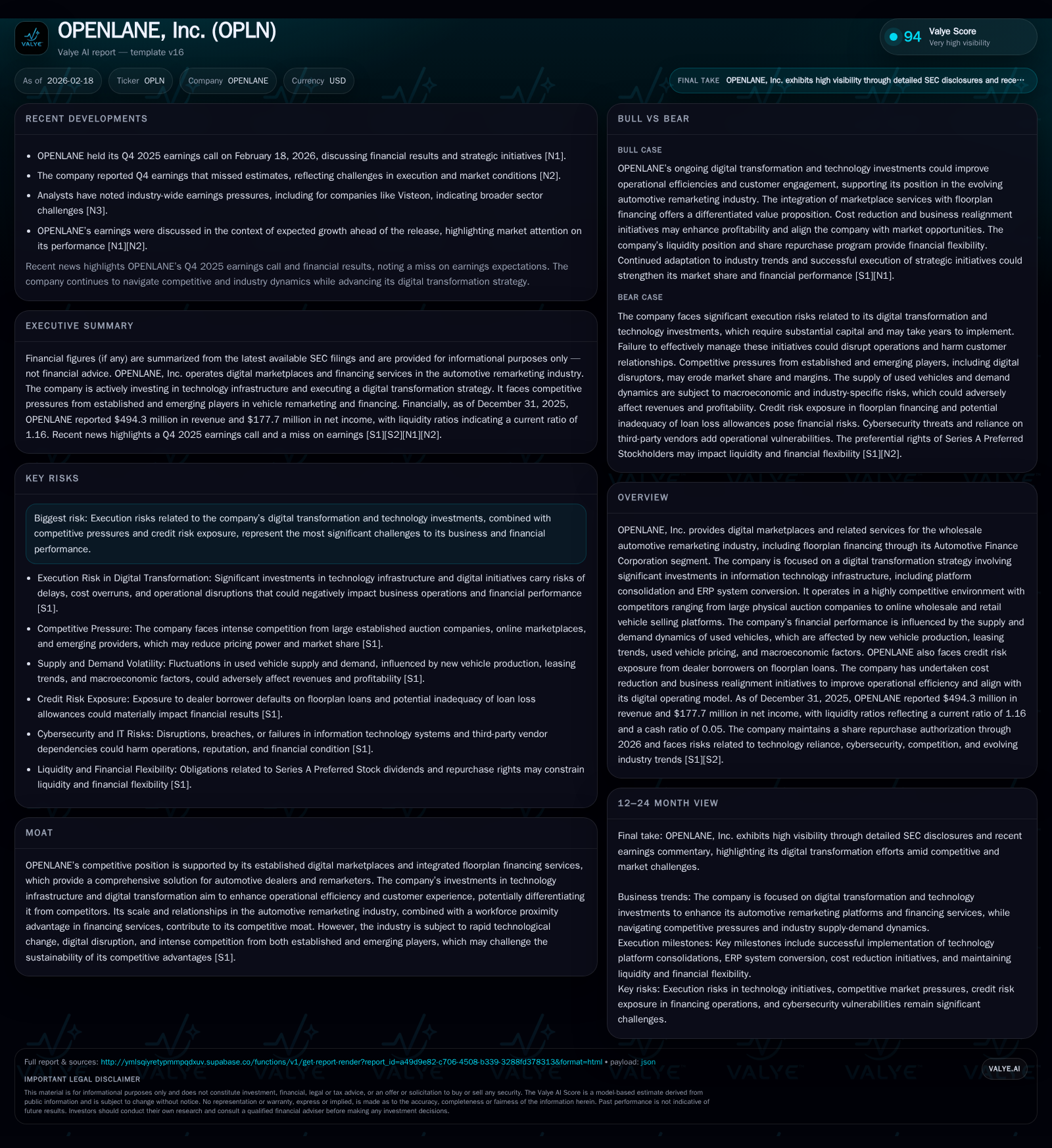

OPENLANE, Inc. operates digital marketplaces and provides floorplan financing for automotive wholesale remarketing, navigating a complex industry influenced by macroeconomic factors and intense competition. Its recent years have seen steady revenue growth but declining operating income amid heavy investment in digital transformation initiatives, including technology platform consolidation and ERP conversion. Credit risk exposure and ongoing cost management efforts add layers of operational complexity. The company’s future hinges on successful execution of its tech strategy and adapting to rapid industry changes while managing credit risks from dealer financing.

Company Overview

OPENLANE, Inc. is a key player in the wholesale automotive remarketing sector through its digital marketplaces that connect dealers for vehicle resale transactions, augmented by its Automotive Finance Corporation (AFC) segment focused on floorplan financing—providing short-term loans against inventory primarily for dealers. The business model leverages technology to address dealer pain points such as inventory movement efficiency and financing convenience, placing OPENLANE at the nexus of vehicle remarketing and financing.[S1]

The company has undertaken an ambitious digital transformation strategy centered around modernizing its underlying information technology (IT) infrastructure. This encompasses consolidating multiple technology platforms into unified systems and implementing an enterprise resource planning (ERP) system to streamline operations. While these initiatives aim to enhance customer experience and operational scalability, they introduce execution risks that have already influenced short-term profitability.[S1][S12]

Historical Financial Performance

OPENLANE has demonstrated consistent top-line growth over the past several years with revenues increasing from approximately $373 million in FY2022 to $494 million in FY2025, representing a compounded annual growth rate near 9%. This growth is attributable to increased vehicle transaction volumes across its marketplace platforms alongside the expansion of floorplan loan originations.[F1]

However, operating income trends reveal pressure points caused by the company's step-up in expenses related to IT modernization efforts as well as competitive pricing dynamics. After peaking at $87.7 million in FY2022, operating income declined sharply to $42.5 million by FY2025 despite higher revenues. This suggests increased operating leverage strain or margin compression linked to strategic investments.[F1]

Net income figures tell a more complex story due to volatility including a substantial loss recorded in FY2023 (-$154 million), potentially tied to impairment charges or one-off items often encountered during transition phases. Recovery ensued with net income at $177.7 million in FY2025, indicating some normalization possibly aided by cost reduction measures or improved AFC performance.[F1]

Financial Summary Table:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | OpInc ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 494 | 178 | 43 | 55 | +8.6% | +61.7% |

| 2024 | 455 | 110 | 79 | 53 | +16.3% | +171.3% |

| 2023 | 391 | -154 | 57 | 52 | +5.0% | -163.9% |

| 2022 | 373 | 241 | 88 | 61 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): CFO, Div, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 46 | 14.3 |

| 2024 | 30 | 8.2 |

| 2023 | 22 | -11.6 |

| 2022 | 182 | 15.9 |

Source: SEC companyfacts cache [F1].

Note: Operating cash flow (CFO) data not consistently available; dividends omitted due to no payments reported.

Capital Allocation and Returns

Despite profitability challenges, OPENLANE has maintained disciplined capital deployment focused on share repurchases—executing buybacks totaling $45.6 million in FY2025—which signals commitment toward enhancing shareholder value amid structural transitions.[F1][S6]

No dividends have been paid recently; this aligns with corporate priorities centered on reinvestment into digital transformation programs and managing debt levels safely.[F1][S5]

Equity holders have witnessed fluctuating book values reflective of earnings volatility and capital activities; equity stood at roughly $1.24 billion as of end-2025 compared to $1.52 billion at end-2022.[F1] Approximate return on equity based on net profits stood near 14% for FY2025—a moderate indication of capital efficiency considering ongoing strategic restructuring.[F1]

Liquidity and Debt Position

OPENLANE carries significant debt obligations totaling about $550 million exclusive of AFC-related securitization liabilities at the end of calendar year 2025.[F1][S4][S8] These borrowings impose constraints including restrictive covenants that limit additional leverage capacity and necessitate careful cash flow management.

The blend includes term loans with floating interest rates indexed to SOFR benchmarks plus margins ranging between roughly +150 to +250 basis points.[S25] This exposes OPENLANE to interest rate risk especially if rates climb further.

The company maintains approximately $410 million remaining borrowable capacity under lines of credit after letter-of-credit commitments.[F1] Nonetheless liquidity remains sensitive given capital expenditure commitments around IT infrastructure updates supplying long lead times and uncertain immediate payoff.[S12]

Industry Competitive Environment

OPENLANE operates within a fragmented ecosystem featuring legacy physical auction firms alongside burgeoning online wholesale platforms delivering dealer-to-dealer sales solutions.[S13]

Digital disruption is reshaping dealer behaviors; new entrants leveraging AI-driven insights or mobile-first user experiences intensify competition not only for transaction volumes but also financing wallet share within floorplan lending.

AFC faces rivals like NextGear Capital plus regional banks targeting similar dealer segments with tailored credit products.[S13] Price sensitivity combined with demands for seamless integration creates both opportunity and risk for incumbents.

Competitive Moat Considerations

OPENLANE benefits from a vertically integrated model merging marketplace technology with embedded finance offerings via AFC—a combination that can foster stickier customer relationships through bundled services delivering convenience and efficiency gains.[S1]

Proximity-based workforce servicing local markets also differentiates AFC services further than purely remote lenders might achieve.[S13]

Nevertheless rapid advances by competitors adopting AI-powered analytics or blockchain-based provenance tracking could erode defensibility unless matched promptly by OPENLANE’s technology transformations.[S1]

Key Risks Impacting Business Prospects

Execution risk looms large around digital transformation projects: failed or delayed platform rollouts could disrupt business continuity hurting customer retention or revenue streams via transaction volume loss or longer sales cycles.[S1][S12]

Credit risk inherent in floorplan lending amplifies uncertainty—macroeconomic downturns driving dealer insolvencies could trigger elevated loan defaults beyond current allowance estimates threatening profitability.[S18]

Cybersecurity threats grow along with reliance on complex integrated IT systems holding sensitive data; breaches could result in reputational damage or costly regulatory penalties given evolving privacy regulations worldwide.[S9][S11]

Industry shifts including changes in new vehicle production rates, leasing penetration influencing used vehicle supply/demand balance, fluctuation in used car pricing trends combined with macroeconomic conditions such as inflationary pressures represent external growth constraints difficult for OPENLANE to control fully but critical to monitor closely.

Future Growth Outlook—What To Watch For

Management has not provided explicit quantitative guidance recently but commentary emphasizes continued prioritization of completing ERP conversions along with platform consolidations within the next few years as pivotal milestones affecting operational scaling and long-term profitability improvement.[N1][S1]

Monitoring quarterly updates around technology deployments’ impact on transaction throughput times or unit economics will serve as practical barometers.

Tracking AFC’s portfolio quality metrics such as delinquency rates or charge-offs remains vital given their direct effect on earnings stability amid tightening credit conditions.

Given nearly flat quarter-over-quarter revenue gains historically coupled with volatile operating margins, investors should look for inflection signals demonstrating bottom-line stabilization post-investment cycle.

Liquidity availability under committed credit facilities versus looming scheduled principal repayments constitutes another critical aspect impacting strategic flexibility.

Conclusion

OPENLANE stands at an inflection point mapped between transformative ambition and prevailing challenges presented by intense competition, operational overhaul requirements, credit market volatility, and regulatory complexity. Its historical revenue growth evidences underlying demand strength along with brand presence fortified through integrated marketplace-finance capabilities offering unique value propositions. However, substantial investments weighing on margins reflect typical tradeoffs incumbent upon executing large-scale tech upgrades — outcomes not guaranteed absent meticulous project governance paired with adaptive market strategies. Key drivers shaping OPENLANE's medium-term trajectory include realizing expected benefits from IT modernization efforts while maintaining prudent credit risk discipline amidst fluctuating used vehicle industry dynamics. Share repurchases indicate confidence but also caution given constrained dividend policy reflecting reinvestment priorities aligned toward sustainable competitive positioning. Ultimately, OPENLANE’s ability to harness innovation effectively without losing sight of core operational resilience will determine whether it emerges more competitively advantaged from the ongoing digital disruption reshaping automotive remarketing.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice or recommendations regarding securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments