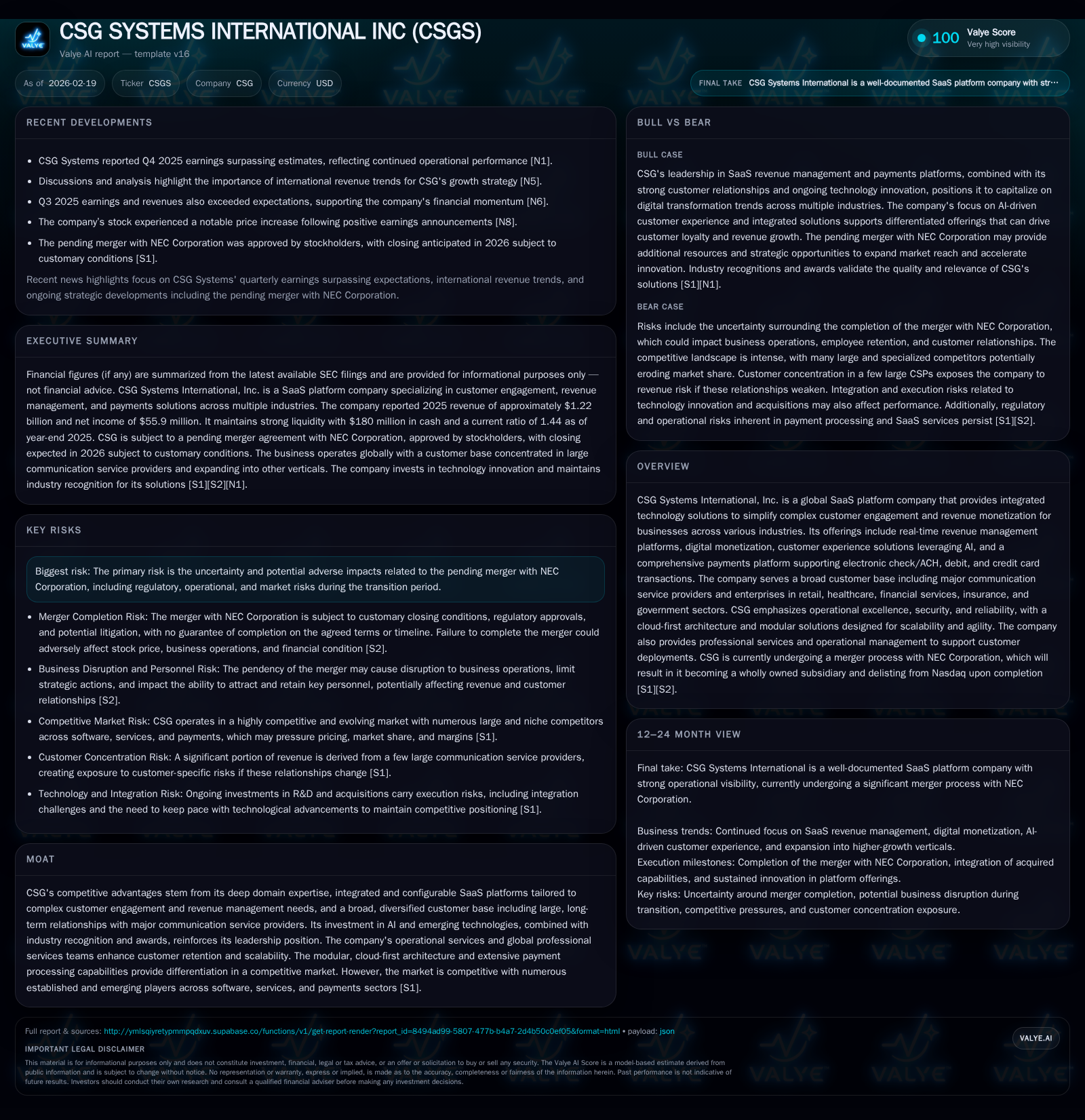

CSG Systems Faces Merger Uncertainties Amid Shifting Profitability and Capital Moves

CSG Systems reports slowing revenue growth and profit pressures alongside a pending merger with NEC, creating investor focus on cash flow strength and capital strategy.

CSG Systems International delivered a modest 2.3% revenue increase in fiscal 2025 but faced nearly 10% operating income decline and a substantial 35.7% net income drop amid higher acquisition and stock-based compensation costs. Operational cash flow grew by 14.9%, supporting dividends and share repurchases despite profitability pressures. Capital expenditures decreased sharply by over 35%, reflecting possible strategic shifts ahead of the pending merger with NEC Corporation, which carries regulatory and operational risks affecting execution. The company’s deep SaaS platforms across communications and expanding verticals remain competitive, with AI technology integration driving future growth potential. Debt structure includes a $600 million revolver and convertible notes, with liquidity ample for ongoing needs but constrained by merger restrictions. Shareholder returns via dividends and buybacks continue amid the transition, with a return on equity of approximately 15.7%.

Historical Revenue and Profit Trends Reflect Margin Pressure

CSG Systems International reported consolidated revenues of approximately $1.22 billion in fiscal year 2025, up only 2.3% from the prior year's $1.20 billion [F1]. This marks a notable deceleration relative to previous years that saw stronger top-line expansion driven primarily by SaaS platform adoption across communications service providers (CSPs) and expanding industry verticals [S16]. Operating income contracted by roughly 9.6% to $118.7 million from $131.3 million in fiscal 2024 [F1]. This decline reflects increased acquisition-related expenses including about $13.7 million in transaction costs tied to the NEC merger process alongside an $11.7 million rise in stock-based compensation costs [S23], which compressed operating margins from about 11% down to near 9.7% [F1]. Net income was impacted more severely, plunging approximately 35.7% year-over-year to $55.9 million due in part to a higher effective tax rate as well as these non-recurring merger-associated charges [F1][S23].

These dynamics suggest that while top-line growth remains positive albeit modest, profitability is under pressure from strategic investments related to merger execution as well as competitive market factors possibly affecting pricing power or contract renewals within key CSP relationships [S11][S13]. The revenue breakdown continues to be driven predominantly by SaaS and related solutions (around $1.1 billion) supplemented by smaller streams from software services and maintenance contracts [S16]. Such concentration underscores dependence on scaling cloud-first platforms while balancing cost discipline.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 56 | 156 | 119 | 15 | -35.7% |

| 2024 | 87 | 136 | 131 | 22 | +31.1% |

| 2023 | 66 | 132 | 124 | 28 | +50.4% |

| 2022 | 44 | 64 | 79 | 37 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, ROE%. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 37 | 83 | 141 |

| 2024 | 27 | 68 | 113 |

| 2023 | 34 | 127 | 104 |

| 2022 | 33 | 97 | 27 |

Source: SEC companyfacts cache [F1]. Not included (outdated snapshot)

Note: Data sourced from SEC company facts [F1]; metrics such as ROE derived from latest available data.

Operational Cash Flow Growth Supports Strategic Flexibility

Despite softening earnings metrics, CSG’s operating cash flows increased robustly by nearly 15% year-over-year to about $156 million in FY2025 [F1]. This divergence between net income decline and CFO growth can be attributed partly to working capital improvements or non-cash charges such as amortization of acquired intangibles related to acquisition activity [S25]. The resulting free cash flow—calculated by subtracting capex from CFO—remains strong at approximately $141 million, providing a vital liquidity buffer for ongoing dividend payments, share repurchases, and funding for strategic initiatives [F1][S20].

The solid free cash generation is particularly important given the pending deal with NEC Corporation which imposes both financial demands related to transaction costs as well as operational constraints restricting certain corporate actions without NEC consent after signing [S2][S12]. Maintaining healthy operational cash flows will thus support CSG's ability to navigate uncertainty during this transition period.

Capital Investment Pullback and Impact on Future Platform Innovation

Capital expenditures declined markedly by over one-third (approx -35%) down to around $14.5 million in FY2025 from a prior level exceeding $22 million [F1], indicating a significant pullback in fixed asset investment compared to earlier years when capex exceeded $27 million [F1]. This moderation likely reflects management’s dual imperative of preserving financial flexibility during the NEC merger process while prioritizing operational efficiency through cloud-first architecture enhancements rather than heavy physical infrastructure spend [S26].

Given CSG’s emphasis on modular SaaS platforms designed for scale across complex B2B2X ecosystems—leveraging microservices architectures supporting agile monetization—the capex decrease may represent a temporary operational shift rather than long-term innovation deprioritization [S11][S19]. However, sustained R&D investment will remain critical to protect CSG’s moat against emerging competitive threats in integrated digital monetization solutions including AI-driven customer journey orchestration [S23].

Navigating the Pending NEC Merger: Risks and Market Reactions

On October 29, 2025, CSG entered into an Agreement and Plan of Merger with NEC Corporation whereby CSG will become a wholly owned subsidiary following regulatory approvals expected by late-2026 [S1][S2][S3]. This transaction triggers several conditional terms including antitrust clearances under Hart-Scott-Rodino regulations along with contract approvals by CSG shareholders [S2].

Key risks include potential delay or failure to consummate the merger exposing CSG to hefty termination fees (~$82 million), disruption of business continuity, departure of key employees due to uncertainty about post-merger roles, erosion of client confidence triggered by competitor tactics exploiting integration doubts, plus ongoing legal and advisory expenses prolonging transition costs without benefit realization [S2]. As mandated under the agreement, CSG must operate within strict ordinary-course business parameters limiting opportunistic ventures prior to closing [S12].[N1]

Investors reacted cautiously despite an overall Q4 earnings beat reflecting these ambiguities coupled with market-wide technology sector pressures; watch for update disclosures on regulatory status and employee retention incentives announced alongside recent filings describing accrued retention bonuses totaling roughly $9 million for key personnel ahead of closing [N1][S25].

Customer Base Diversification and Technology Differentiation

CSG supports some of the largest names across global communications service providers including Charter Communications (19% revenue contribution), Comcast (17%), DISH Network L.L.C., alongside hundreds of other clients spanning retail giants like Walgreens, financial institutions such as JP Morgan Chase, healthcare providers, insurance companies, state & local governments — all linked via its integrated SaaS ecosystem designed for real-time revenue management & digital monetization spanning B2B/B2C/B2B2X models [S6][S7].

Their cloud-native products deliver granular capabilities—such as usage rating/charging mediation modules integrated into payment platforms handling billions in annual transactions across some ~163K active merchants globally—with PCI-compliant environments augmented by AI-powered fraud detection using behavioral profiling algorithms targeting loss minimization without compromising revenue recognition accuracy [S19].

While deep domain expertise ensures stickiness through decades-long client relationships supported by expansive professional services teams facilitating solution architecture design & deployment at scale,[S11] competition is intensifying from established OSS/BSS vendors alongside digital-first fintech disruptors targeting fragmented vertical niches requiring continuous innovation across platform capabilities including personalization engines & subscription management extensions flagged by industry analysts like IDC & Gartner[S23].

2026 Growth Outlook Amid Industry Competition and AI Leverage

Explicit guidance remains unavailable given merger uncertainties; however, AI integration is increasingly emphasized as a key catalyst enabling personalized customer experiences driving upsell opportunities within both legacy communication customers adapting to digital transformations plus high-growth vertical expansions outside telecom such as healthcare claims monetization or government payment modernization[N1].

What investors should watch include: renewal terms or amendments extending foundational CSP contracts observed recently with Charter through September 2031 featuring fixed price escalators enhancing recurring SaaS revenue visibility[S17]; indicators of successful AI-enabled product adoption reflected indirectly through license renewal lumpiness or professional services expansion; progress updates on regulatory clearances shaping the timing of full-merger benefits realization; reported changes in win rates vs competitors placing stress on market share gains[S2][N1].

Balance Sheet Review: Debt Structure and Liquidity Position

As of December end-2025,Cash stood at approximately $180 million supported by current assets over liabilities yielding a current ratio near healthy level of ~1.44[F1],[reflective of balanced short term liquidity.S4],[while total long-term debt comprised roughly $125M drawn under a new five-year revolving credit facility extended March-2030 charging SOFR + margin(approx combined rate ~5.18%), plus unsecured convertible notes ($425M principal amount due September-2028 paying fixed coupon at ~3.875%) offering some refinancing flexibility before potential conversion triggers linked to merger close[S4][S5][S21].

Liquidity headroom includes nearly half a billion dollars remaining availability under revolver less letters of credit commitments allowing buffer for working capital fluctuations.The debt covenants impose standard affirmative/negative restrictions limiting additional indebtedness or dividends absent lender consent.If NEC acquisition closes financing facilities will be settled terminating revolver commitments,and embedded options unwound affecting capital structure further[S21].

Capital Allocation Strategy: Dividends, Share Buybacks, and Returns

CSG has demonstrated commitment to shareholder returns through steadily rising dividends from approximately $26.6M paid in FY2024 up to nearly $37.4M in FY2025 respectively[F1][S20], alongside opportunistic yet moderated share repurchases totaling ~$83M last fiscal year.Downtrends vs peak repurchases above ~$127M seen previously imply cautious calibration aligned with merger-related governance limits[S20].

Free cash flow near $141M comfortably covers distributions preserving internal funding capacity for non-discretionary R&D spend still necessary amid technological race.Return-on-equity based on last reported equity levels (~$356M end FY22)[F1] reaches an estimated ~15.7%, signaling efficient equity utilization but constrained profit margins dampen total return accrual going forward absent margin improvement or accelerated top-line expansion.

Disclaimer:

This report is for informational purposes only without any recommendation or solicitation to buy or sell securities related to CSG Systems International Inc., or any other entity mentioned herein.It reflects analysis grounded strictly on publicly available information cited herein as per compliance guidelines.The future operational results and strategic outcomes discussed involve risks including completion uncertainties around the NEC merger that could materially affect company performance.All prospective readers should consider independently verified disclosures before forming opinions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments