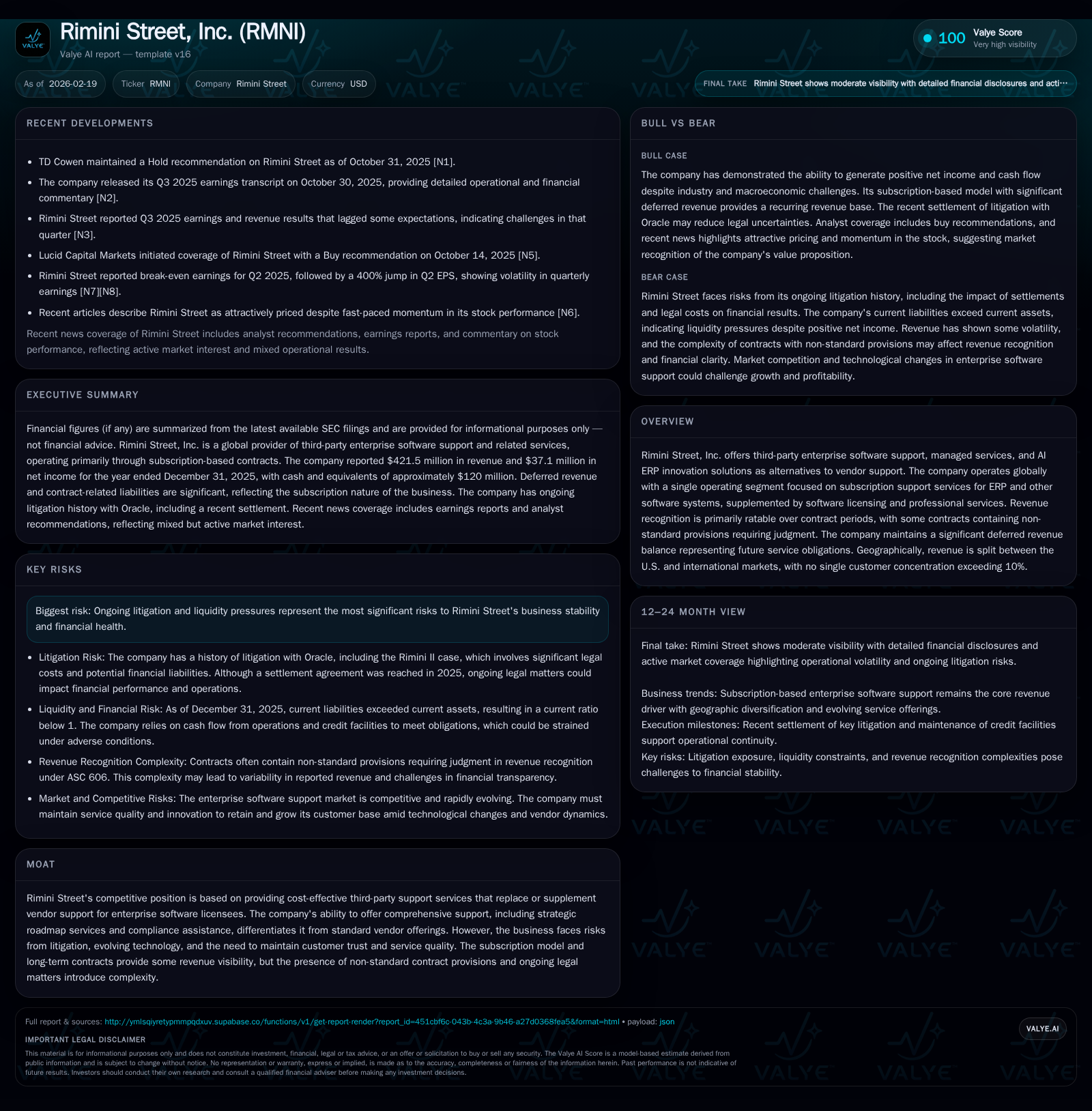

Rimini Street’s Financial Turnaround and Strategic Position Amid Legal and Liquidity Challenges

A detailed review of Rimini Street’s 2025 financial recovery, subscription revenue stability, legal settlement aftermath, and capital allocation strategy.

In 2025, Rimini Street reversed prior losses with $421.5 million in revenue and $59.9 million in operating income, supported by steady subscription services despite Oracle PeopleSoft support wind down. The company navigates ongoing litigation risks under a standstill agreement through 2028, while managing liquidity constraints with a restructured credit facility. Strong operating cash flow enabled share repurchases amid negative equity and elevated interest expenses. Emerging AI-driven ERP solutions suggest future growth potential, although contractual complexities and debt repayments remain key focus areas.

Subscription Services Sustain Revenue during Transition

Rimini Street's business model centers on third-party enterprise software support delivered primarily via subscription contracts recognized ratably over service periods. In fiscal year 2025, reported revenue was $421.5 million compared to $428.8 million in 2024—a slight decline (-1.7%) largely attributable to the wind down of Oracle PeopleSoft support services which historically comprised approximately 5-8% of total revenue [F1][S7][S18].

The company's customer base is geographically diversified with international revenues slightly exceeding U.S.-based revenues (54% vs. 46%) in 2025, supporting stable recurring income streams [S7]. Deferred revenue balances stood near $269 million at year-end—an important indicator of contracted future performance obligations yet to be recognized as income [F1][S4].

Recognition patterns adhere to ratable accounting principles consistent with subscription models but involve managerial judgment due to contract-specific provisions affecting timing—a complexity typical for software maintenance businesses that impacts earnings quality assessments [S4].

Legal Landscape: Settlement and Wind Down Period

Rimini Street’s operations remain influenced by extended litigation with Oracle related to third-party support services for Oracle products.

The Rimini II case culminated in a confidential settlement effective July 2025 that mandates an orderly cessation of PeopleSoft support by July 31, 2028; during this Wind Down Period, all active legal disputes are stayed under a Litigation Standstill agreement [S8][S13][S18].

Despite reducing immediate legal volatility, the company faces ongoing risks including potential breaches that could revive proceedings or affect client retention given Oracle's competitive position and related injunctions [S15][S21]. The company reports maximum potential liquidated damages around $8.2 million though no such liabilities have been incurred to date [S13].

These legal factors impose operational constraints particularly on marketing certain Oracle-related services and may influence contract renewals.

Financial Performance: Recovery from Prior Losses

Rimini Street’s financial turnaround between fiscal years 2024 and 2025 is significant:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 37 | 60 | 60 | +202.3% | ||

| 2024 | -36 | -39 | -32 | -239.2% | ||

| 2023 | 431 | 26 | 12 | 44 | +5.3% | +1150.8% |

| 2022 | 410 | -2 | 35 | 8 | +9.4% |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 8 | 56 | -137.3 |

| 2024 | 0 | -42 | 52.2 |

| 2023 | 1 | 5 | -66.0 |

| 2022 | 5 | 31 | 3.2 |

Source: SEC companyfacts cache [F1].

(Data derived from SEC filings as per [F1])

Operating margins expanded from approximately -7.5% in FY24 to +14.2% in FY25 due to improved gross profits on subscriptions coupled with lower legal expenses following settlements [F1][S2]. Sales and marketing expenses remained stable year-over-year while litigation costs shifted from charges to recoveries enhancing earnings leverage.

Net income reversal exceeded $73 million compared to the previous year reflecting effective cost controls and structural resolution of key legal matters.

Capital Structure: Refinancing and Liquidity Considerations

In April 2024, Rimini Street refinanced its credit facilities replacing a $90 million term loan with a new five-year senior secured credit facility comprising a $75 million term loan plus a $35 million revolving line of credit [S4][S5].

As of December 31, 2025, net long-term debt was approximately $63 million after scheduled principal repayments [$67 million gross], showing ongoing deleveraging efforts amid tight liquidity management [F1][S6]. The company faces annual principal payments escalating over the term culminating in balloon payments at maturity.

Annual interest expense totaled roughly $6.15 million reflecting effective rates near ~8%, inclusive of SOFR-based pricing plus applicable margins tied to leverage ratios—demonstrating financing cost pressures post-market rate increases [S6][S10].

Balance sheet liquidity remains adequate but constrained: cash & equivalents totaled about $120 million while current liabilities ($347M) exceed current assets ($300M), yielding a current ratio near 0.86 which is below traditional comfort levels for technology service firms [F1][S9]. Shareholders’ equity remains negative around -$27 million mainly due to accumulated deficits resulting in an approximate negative return on equity exceeding -130%, complicating capital return prospects despite recent profitability gains.

Deferred Revenue: Contractual Complexity and Visibility

Deferred revenue represents advanced billings for services not yet delivered totaling nearly $269 million within current liabilities as of year-end; this signals substantial contracted performance obligations expected to convert into revenue within the next twelve months providing topline predictability [F1][S4][S24].

However, subscription agreements include non-standard terms requiring management estimates impacting timing judgments under ratable recognition rules—introducing accounting complexity that affects earnings quality evaluation typical for enterprise software support models.

Active governance is necessary to ensure revenues realize consistently with contractual performance without risk of overaccrual.

Cash Flow Strength Enables Targeted Capital Returns

Operating cash flow rebounded sharply by approximately +255% reaching about $60.2 million in FY25 compared to an outflow near -$38.9 million in FY24 largely driven by litigation settlement inflows combined with operational improvements [F1][S25].

Capital expenditures remained controlled at roughly $4.6 million (up ~35%), focused on sustaining existing infrastructure rather than expansion.

Consequently free cash flow (operating cash flow minus capex) approximated $55.65 million empowering selective capital returns including open market share repurchases totaling $7.6 million during FY25 while maintaining approximately $36-37 million repurchase authorization capacity as extended through June 2029 by the Board of Directors [F1][S11].

No dividends were declared recently; buybacks appear calibrated balancing liquidity preservation against shareholder value enhancement.

Strategic Outlook: AI-Enabled ERP Support Innovation

Rimini Street is advancing strategic initiatives beyond traditional third-party maintenance through development of Agentic AI-powered ERP innovation solutions aimed at augmenting enterprise software ecosystems leveraging artificial intelligence capabilities outlined broadly in corporate disclosures .

This approach seeks to transcend pure cost-savings replacement toward enabling clients’ digital transformation strategies potentially unlocking higher-margin service verticals that differentiate Rimini Street amid evolving technological landscapes.

While contribution metrics or timelines remain undisclosed, this initiative aligns with broader industry trends favoring AI-enhanced IT operations automation presenting latent optionality for new growth inflections if market adoption accelerates.

Key Monitoring Points Going Forward

Investors should track:

- Completion progress toward the July 31, 2028 PeopleSoft support wind down per settlement terms which will formally conclude related litigation exposures affecting long-term client relationships;

- Renewal rates on existing subscription contracts materially impacting deferred revenue conversion patterns;

- Scheduled principal repayments mandated under refinancing agreements requiring continued robust cash flow generation;

- Developments regarding litigation standstill arrangements which could alter risk profiles;

- Market traction for AI-driven ERP innovation offerings potentially influencing future revenue diversification.

Transparency around these developments will be essential given their material impact on valuation amidst persistent legal and financial complexities.

Disclaimer: This analysis relies exclusively on publicly available SEC filings and does not constitute investment advice or forward-looking forecasts beyond cited data.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments