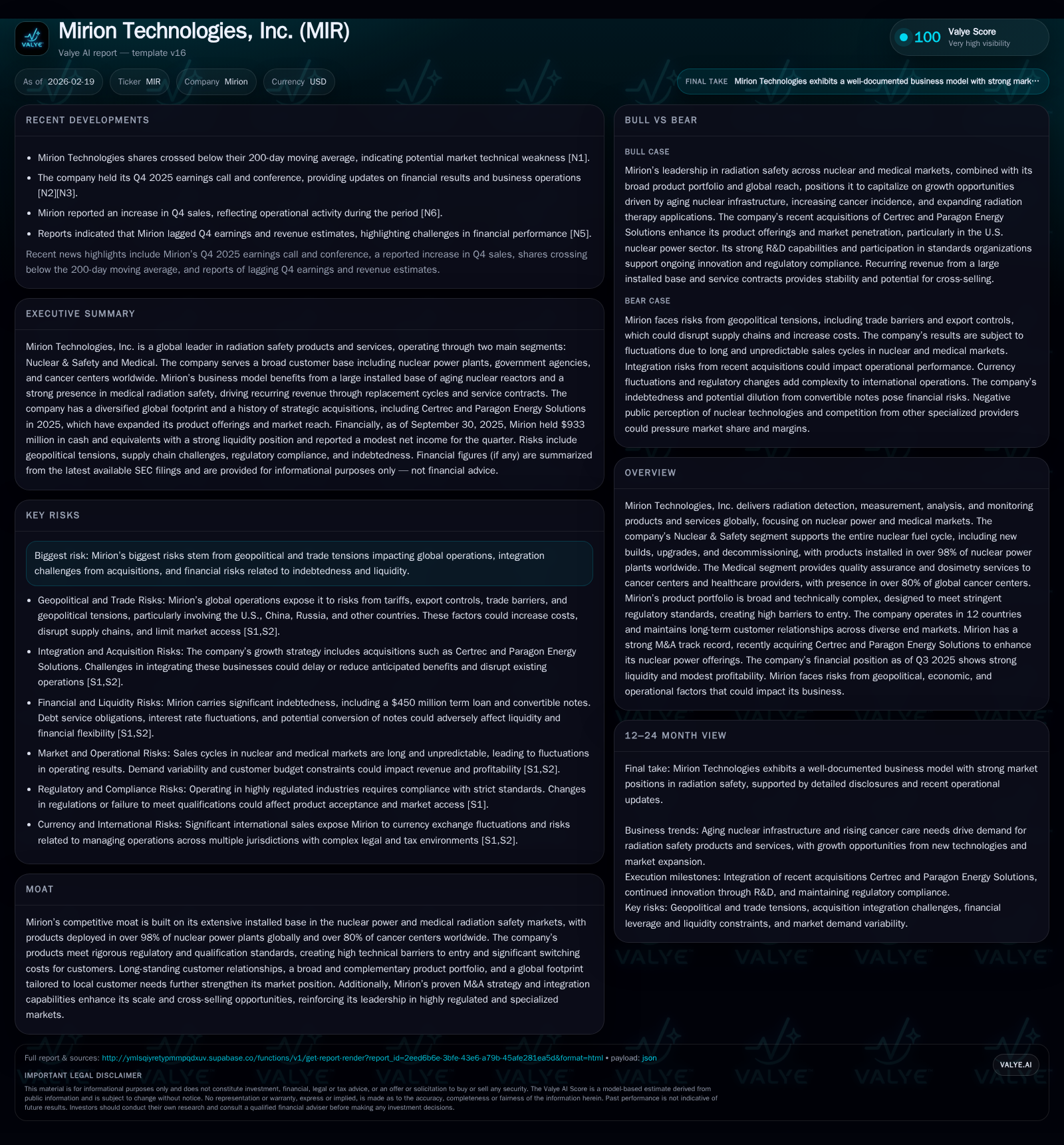

Mirion Technologies Boosts Profitability via Strategic Acquisitions and Nuclear Market Expansion

Mirion leverages its strong nuclear and medical installed base alongside M&A to drive revenue growth and margin recovery.

Mirion Technologies, a leader in radiation detection and safety, reversed multi-year operating losses to generate $51.5 million operating income in 2025, driven by acquisitions and nuclear market demand. Its products serve over 98% of global nuclear power plants and 80% of cancer centers, creating high barriers to competition through regulatory complexity and long-term customer relationships. Growth is expected to come from ongoing integration of Certrec and Paragon acquisitions, expansion into underpenetrated markets, and increasing nuclear new builds. However, geopolitical risks and regulatory compliance remain key challenges. The company’s capital allocation shows increased buybacks amid solid cash flows, with a modest return on equity reflecting ongoing operational investments.

Company Overview

Mirion Technologies positions itself as a critical enabler of radiation safety and measurement technologies with a dual focus on the nuclear power cycle and medical markets. It boasts a twentieth century legacy rooted in ionizing radiation expertise, offering solutions that address highly complex regulatory standards globally. Headquartered in Atlanta with operations spanning twelve countries including U.S., Europe, and Asia Pacific, Mirion’s footprint caters to localized market needs while maintaining strong global reach [S1][S4].

Segment Focus

- Nuclear & Safety: Covers the full range of the nuclear fuel cycle—from mining to waste management—serving over 98% of nuclear power plants worldwide. Recent acquisitions of Certrec (regulatory compliance software) and Paragon Energy Solutions (U.S. nuclear market expansion) fortify this segment’s product portfolio enhancing digital capabilities and service offerings [S5][S6].

- Medical: Focuses on radiation safety applications within cancer centers, diagnostic imaging, dosimetry services, reaching approximately 80% of global cancer centers. This segment relies heavily on product innovation backed by nearly eighty issued patents worldwide protecting its cancer diagnostics and therapeutics technologies [S1][S19].

Historical Financial Performance

Mirion’s historical P&L reveals a pronounced turnaround after several years of net losses. The company reported operating losses throughout FY2022-2023 with an especially steep operating loss of -$297.8 million in 2022 mostly attributable to acquisition-related amortization charges [F1]. By FY2025, operating income rebounded strongly to $51.5 million alongside net income turning positive at $28.8 million per year-end disclosures [F1].

Cash flow generation improved steadily; operating cash flow rose from $39.4 million in FY2022 to $143.3 million by FY2025, reflecting stronger underlying operations after integrating recent acquisitions [F1]. Capital expenditures moderated from $48.8 million (FY2024) down to $36.4 million (FY2025), implying more efficient capital deployment as scale increased [F1].

Share repurchases escalated sharply with nearly $50 million spent in FY2025 compared to minor levels earlier indicating management confidence supported by healthy free cash flow estimated around $107 million [F1]. Equity stood at $1.87 billion at the end of FY2025 yielding an approximate return on equity near 1.5%, which remains modest likely due to intangible asset amortizations from acquisition accounting [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 29 | 143 | 52 | 36 | +179.8% |

| 2024 | -36 | 99 | 25 | 49 | +62.7% |

| 2023 | -97 | 95 | -22 | 37 | +65.0% |

| 2022 | -277 | 39 | -298 | 34 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 50 | 107 | 1.5 |

| 2024 | 2 | 50 | -2.4 |

| 2023 | 1 | 58 | -6.5 |

| 2022 | 5 | -19.8 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures not disclosed in accessible tags; dividends data unavailable.

Growth Prospects

Mirion's growth trajectory hinges largely on leveraging its dominant position within the nuclear lifecycle market bolstered by strategic acquisitions:

- Acquisitions Integration: The recent addition of Certrec enhances compliance software capabilities critical for evolving regulatory regimes targeting nuclear power operators [S5]. Paragon Energy Solutions extends Mirion’s reach within the U.S., enabling access to integrated product suites for existing customers investing in infrastructure modernization [S5].

- Nuclear New Builds & Upgrades: With approximately 70 reactors under construction globally and another 115 planned within the next decade per World Nuclear Association data, Mirion is well positioned to capitalize on utilities expanding or refurbishing their fleets [S10]. Increasing global electricity demands driven partially by AI data center buildouts support potential upside if nuclear energy uptake accelerates.

- Medical Market Expansion: R&D investments foster innovation in quality assurance products for radiation therapy that could expand footprint beyond leading oncology centers into emerging markets like India where Mirion plans targeted expansion leveraging partnerships with reactor design firms [S6][S7].

- Cross-Selling Opportunities: Mirion benefits from recurring revenues tied to installed equipment requiring recalibration, maintenance, or upgrades creating stickiness amidst highly regulated environments which disincentivize vendor switches [S10].

Potential constraints include dependence on government budget cycles influencing contract timing particularly with U.S.-based agencies [S1], geopolitical tensions introducing tariff risks or supply chain disruption especially given export controls enforced across some product lines [S23], as well as ongoing compliance costs tied to complex FDA regulations for medical devices [S15][S19]. Seasonal fluctuations also pose short-term forecast challenges with spike demand concentrated in Q4 aligned with outage schedules at nuclear plants [S19].

Forecasts & Milestones to Watch

While explicit forward guidance was not provided within recent SEC filings or public releases, monitoring several indicators will be pivotal:

- Progress integrating Certrec’s digital offerings alongside Paragon’s product suite post-acquisition.

- Order backlogs remain significant with over $1 billion remaining performance obligations as of Dec 31, 2025; close tracking of order conversion rates will reveal momentum sustainability [S21].

- Regulatory approvals for new or modified medical device innovations impacting market share expansion.

- Geopolitical developments influencing trade policies particularly between U.S., China, Russia could impact international sales channels given Mirion’s ~37% revenues sourced outside North America [S23].

- Outsourcing trends among government customers potentially expanding addressable service markets.

Returns & Capital Allocation Philosophy

Despite substantial investments related to acquisitions causing prior net losses, Mirion has generated improving returns:

- Operating income doubled year-over-year (+107% from FY24 to FY25), net income swung positive by almost $65 million marking a significant earnings improvement trajectory [F1].

- Cash flows have outpaced capex since FY22 resulting in growing free cash flow supporting buyback activity that accelerated notably from $2 million (FY24) to nearly $50 million (FY25), signaling capital discipline balanced against growth investments [F1].

- The current ratio above 2.8 indicates solid short-term liquidity cushioning operational risks linked to seasonality or macro uncertainties [F1].

- No dividend payments were disclosed suggesting reinvestment preference while executing share repurchase programs.

Continued careful management of leverage covenants remains important given debt incurred from acquisitions; adherence reduces refinancing risks while allowing selective future investments [S12]. Executive leadership’s engineering-driven approach combined with participation in standards organizations aids product durability assuring longer customer lifecycles driving sustainable margins [S6][S9].

Risks Overview

Key risk considerations identified include:

- Geopolitical & Trade Risks: Tariffs, export controls, sanctions relating mainly to Russia-China-U.S trade frictions create cost pressures and market access uncertainty potentially affecting revenues from overseas sales constituting roughly one-third of total revenues [S8][S23]. Supply chain disruptions linked to conflict zones or border restrictions could also impede manufacturing timelines.

- Regulatory Compliance Burden: FDA approvals governing medical device development introduce uncertainty regarding timing and costs impacting new product introductions; non-compliance could trigger recalls risking financial penalties and reputational damage [S15][S16][S19]. GDPR data privacy regulations similarly increase compliance costs.

- Integration Execution Risk: Mirion relies heavily on acquisitions for technology breadth; poor integration or failure to realize synergies from newly acquired companies such as Certrec or Paragon could weigh on margins or distract management focus [S5][S12].

- Market Cyclicality & Seasonality: Unpredictable capital spending patterns by governmental customers can cause quarterly fluctuations making earnings less predictable year-round while reliance on outages for peak sales may limit revenue stability outside Q4 periods [S19].

- Litigation & Intellectual Property Risks: Patent infringements (especially within medical segment), evolving open-source software risks expose potential legal costs or forced technology shifts affecting sales continuity or profitability [S8][S11].

Industry Context Analysis (Non-fact)

Radiation detection equipment suppliers operate within extended product cycles often dictated by multi-decade operational lifespans of nuclear facilities or long clinical adoption timelines for medical devices—which emphasizes value continuity over rapid product churn common in other tech sectors. Barriers are reinforced through complex qualification processes involving ISO certifications and regulatory testing standards such as NRC Appendix B or FDA's Quality System Regulation protocols imposing high certification costs deterring entry. Furthermore, shifts toward Small Modular Reactor (SMR) technology generate opportunities but require specialized instrumentation adaptations reflective of unique scale and safety profiles. Cross-sector digitalization—leveraging IoT-enabled sensors integrated with cloud analytics—continues reshaping monitoring service offerings adding incremental revenue streams but necessitates significant R&D investment commitments.

Conclusion

Mirion Technologies stands at a pivotal juncture following successful operational recovery driven by targeted M&A activity augmenting established dominance in highly regulated global radiation measurement markets across nuclear power generation and medical protection spheres. Its unique competitive position benefiting from entrenched installed bases creates dependable recurring revenues buttressed by extensive patent protections and regulatory compliances difficult to replicate. While geopolitical headwinds, fluctuating government budgets and regulatory hurdles pose tangible near-term risks requiring vigilant management execution, the combination of expanded addressable markets via recent acquisitions alongside strong operating cash conversion provides a foundation for moderate profitability growth trajectories going forward. Close monitoring of integration milestones alongside sensitivity to external policy environments will be essential variables defining its medium-term success landscape.

This analysis is based solely on publicly available information including SEC filings ([S#]), industry data, recent earnings calls ([N#]), and financial statement facts ([F1]). It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments