Avis Budget Group Navigates Fleet Cost Volatility and Competitive Pricing in Challenging 2025

Fiscal 2025 results reflect pressures from fleet cost fluctuations, competitive dynamics, and regulatory challenges impacting profitability and capital allocation.

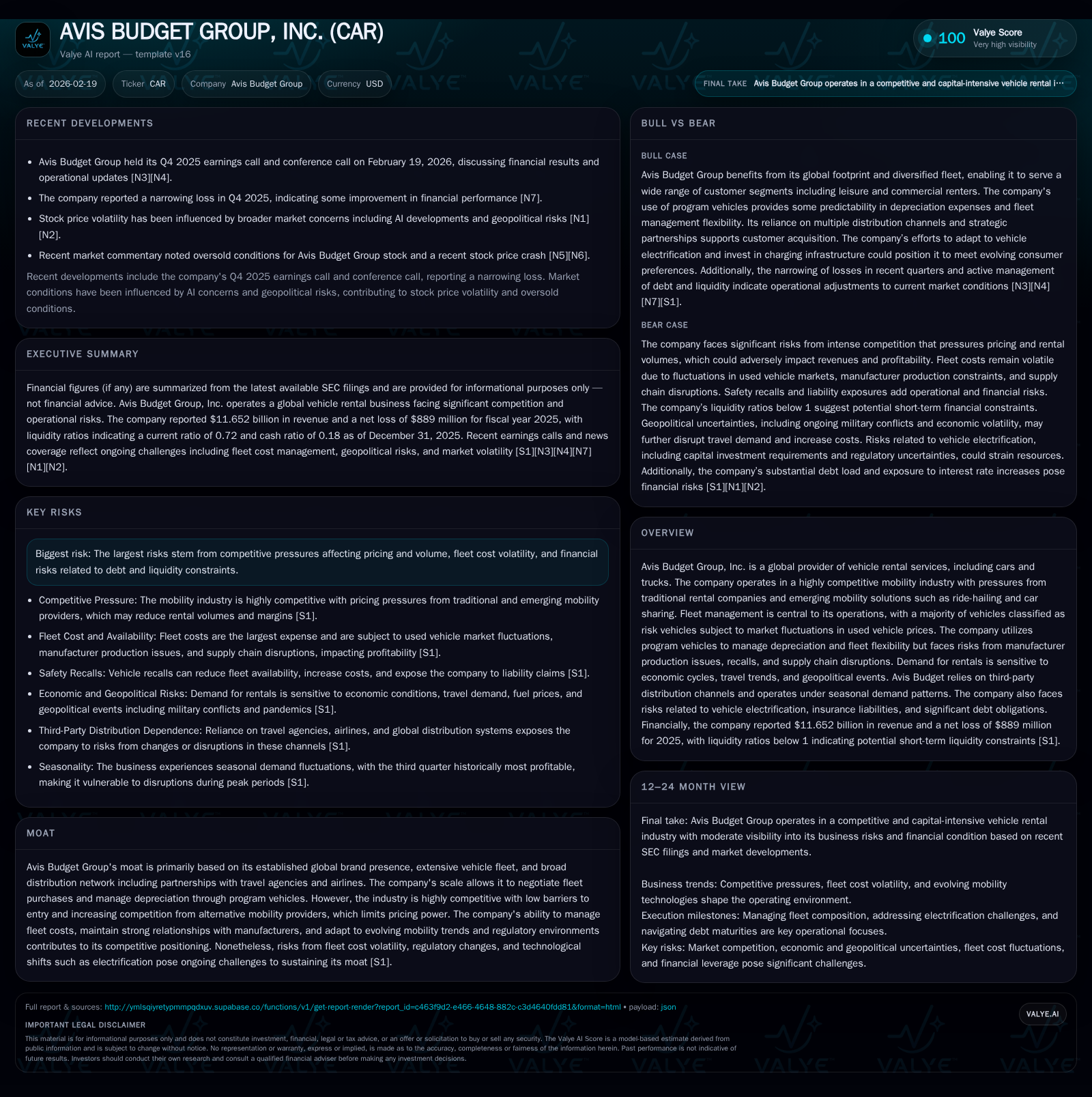

Avis Budget Group reported a slight revenue decline to $11.65 billion in FY2025 alongside narrowing net losses of $889 million, improving from a $1.82 billion loss in 2024. Operating cash flow remained positive at $3.3 billion despite margin compression. The company’s fleet, dominated by risk vehicles vulnerable to used car market swings, faces ongoing supply chain and pricing pressures amid intensifying competition from emerging mobility services. Capital deployment shifted significantly with share repurchases sharply curtailed and no dividends paid since FY2023, reflecting a focus on liquidity amid negative equity and substantial debt. Regulatory compliance, geopolitical risks, and seasonal demand cycles underscore the operating environment's complexity as Avis seeks to leverage scale and technology to sustain its market position [F1][S1][S4][S6][S17].

Historical Performance

Avis Budget Group’s revenues have shown a gradual decline over recent years, falling from $12.0 billion in 2023 to $11.65 billion in 2025—a 1.2% decrease year-over-year—reflecting intense pricing competition within the global vehicle rental industry [F1]. Net income swung from strong profitability of $2.76 billion in 2022 through losses of $1.82 billion in 2024 to a narrower net loss of $889 million in 2025, signaling persistent operational headwinds albeit with some improvement [F1]. Operating cash flow also contracted by 6.3% to $3.30 billion in 2025 but remains positive, supporting ongoing operations despite margin pressure.

The company’s stockholders’ equity position is negative at -$3.13 billion as of fiscal year-end 2025, deteriorating further from -$703 million in 2022 due primarily to accumulated net losses and impairment charges linked to accelerated depreciation policies on fleet assets including electric vehicles (EVs) [F1][S21]. This negative equity highlights balance sheet stress amidst substantial debt levels exceeding $25 billion.

Summary Financials (USD millions)

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|

| 2025 | 11.7 | -0.9 | 3.3 | -1.2% | +51.2% |

| 2024 | 11.8 | -1.8 | 3.5 | -1.8% | -211.6% |

| 2023 | 12.0 | 1.6 | 3.8 | +0.1% | -41.0% |

| 2022 | 12.0 | 2.8 | 4.7 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): OpInc, Capex, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($bn) | ROE% |

|---|---|---|---|

| 2025 | 0 | 0.0 | 28.4 |

| 2024 | 0 | 0.1 | 78.3 |

| 2023 | 355 | 1.0 | -467.6 |

| 2022 | 3.3 | -393.2 |

Source: SEC companyfacts cache [F1].

Note: Capital expenditure data is not available from provided tags.

Core Business Dynamics

Avis Budget operates through a global vehicle rental network offering passenger cars and trucks supported by extensive brand recognition and distribution partnerships encompassing airlines, travel agencies, global distribution systems (GDS), and online platforms [S4][S14]. These channels provide critical access especially at airport concessions—high-value locations requiring competitive lease bids.

The mobility industry landscape is increasingly competitive with new entrants such as ride-hailing firms and car sharing services backed by automakers or tech companies challenging traditional rental volumes through alternative mobility options or aggressive pricing strategies [S1][S14][S25]. Pricing sensitivity is acute particularly in the truck rental segment where fleet size adjustments lag demand shifts.

Fleet management is central: about 84% of Avis’ vehicles are "risk vehicles," whose residual values fluctuate with used car market conditions influenced by macroeconomic factors like inflation and fuel costs [S1][S15][S26]. Program vehicles offer some residual value guarantees but represent a smaller portion of the fleet.

Operational vulnerabilities include supply chain disruptions (e.g., semiconductor shortages), safety recalls necessitating vehicle removals that constrain rentable inventory and elevate costs [S15][S16], and demand variability tied closely to economic cycles—particularly impacting summer leisure travel contributing disproportionately to third-quarter earnings [S4][S18].

Growth Outlook & Constraints

Future growth depends on:

- Effective fleet acquisition balancing program versus risk vehicles mitigating depreciation volatility;

- Technology investments enhancing reservation systems and telematics for optimized fleet utilization;

- Maintaining favorable airport concession leases amid competitive bidding;

- Adapting proactively to regulatory changes including emissions standards driving electrification while managing asset impairment risks tied to EV lifecycle adjustments observed recently [S21];

- Leveraging scale for procurement efficiencies while innovating customer offerings such as loyalty programs or flexible rentals.

Challenges include potential tightening of financing markets affecting asset-backed securitizations essential for fleet purchases; heightened interest rate exposure on approximately $6 billion of unhedged variable rate debt as of end-2025; geopolitical instability influencing fuel prices; cyclical travel demand fluctuations; increasing compliance costs related to data privacy laws (GDPR/CCPA), environmental regulations, insurance product liabilities; plus cybersecurity threats requiring ongoing IT investment [S6][S7][S8][S9][S10][S17].

Capital Allocation & Returns

While ROE calculation is complicated by negative equity balances, net losses narrowed significantly year-over-year suggesting improving returns relative to prior periods (approximate ROE derived as net income divided by negative equity is about -28%) based on available data [F1].

The company ceased dividend payments after FY2023 reflecting a conservative stance on liquidity preservation amid balance sheet constraints. Share repurchases dropped markedly from $951 million in FY2023 to just $7 million in FY2025 indicating cautious capital deployment under current conditions [F1][S17].

Operating cash flows remain solid though trending downwards consistent with a capital-intensive model reliant on regular fleet replacement through sales channels sensitive to used vehicle market dynamics.

Industry Context & Risks

The car rental sector remains cyclical with exposure not only to internal execution risks but also external factors such as fuel price volatility impacting consumer rental behavior and operating costs; shifting consumer preferences favoring ride-hailing solutions; tightening urban emissions regulation mandating fleet electrification; plus mounting cybersecurity risks necessitating continuous IT security investments—all demanding agile management responses.

What To Watch Next

Avis has not provided explicit forward guidance or multi-year projections in recent filings or earnings calls [N1][N9]. Key areas for investor monitoring include:

- Trends in used vehicle residual prices critical for forecasting depreciation impacts;

- Progress toward Advanced Pricing Agreements with tax authorities potentially stabilizing transfer pricing exposures currently subject to audit risk [S10];

- Outcomes of upcoming airport concession lease negotiations affecting prime location access;

- Regulatory developments around corporate responsibility initiatives influencing capex toward sustainable fleets;

- Competitive pricing actions from emerging mobility providers impacting volume elasticity;

- Financing market conditions affecting asset-backed securitization refinancing given clustered maturities within five years totaling over $25 billion debt portfolio;

- Cybersecurity incident disclosures given elevated threat landscape implications for reputation and operational continuity.

This analysis is strictly based on publicly available information up through February 19th, 2026 including SEC filings and news transcripts without any speculative forecasts or investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments