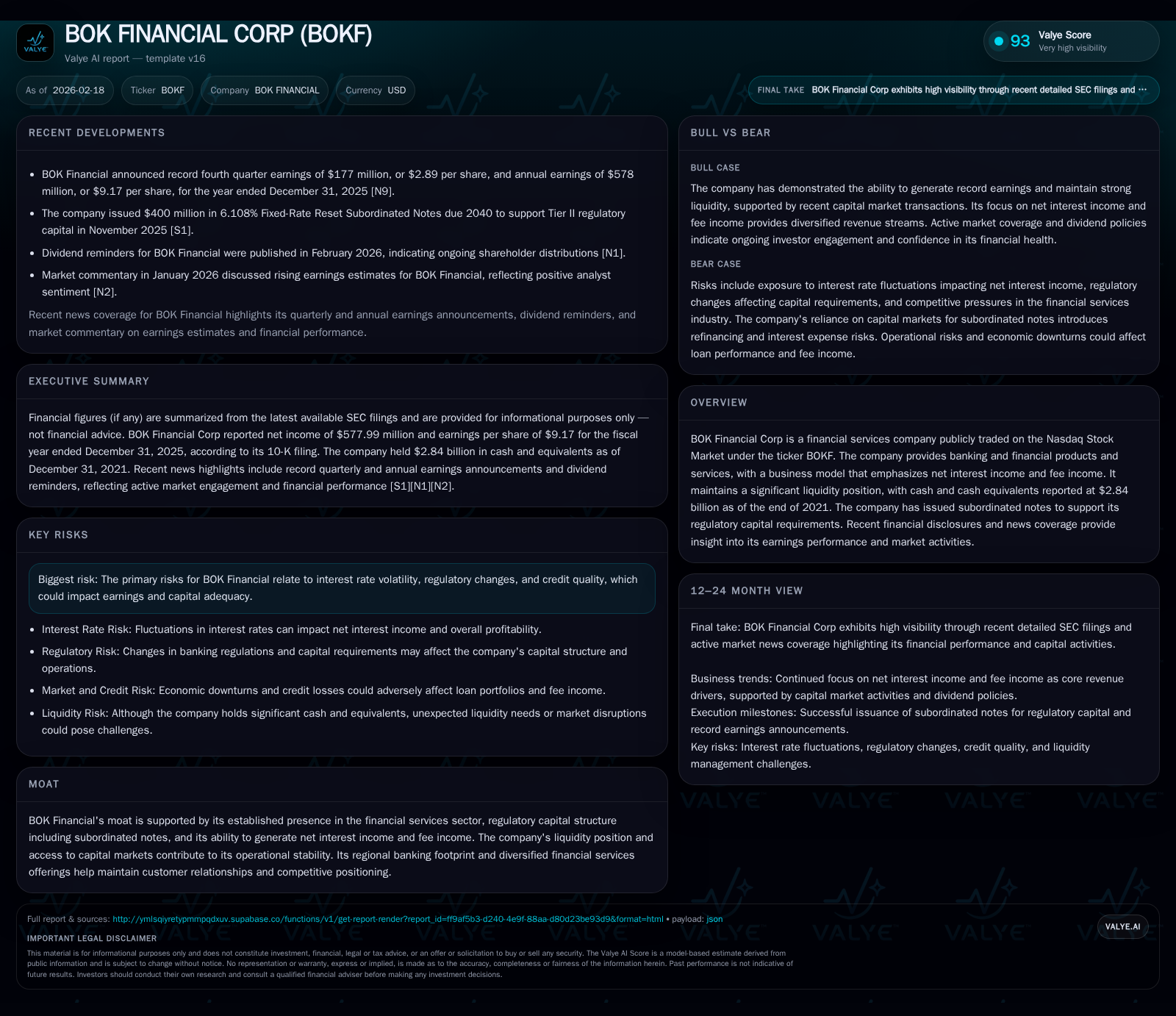

BOK Financial Corp Balances Strong Earnings Growth with Expanding Capital Structure

Record net income and strategic subordinated notes issuance define BOK Financial's recent performance and capital positioning.

BOK Financial Corp reported record earnings in 2025, driven primarily by increased net interest income and fee income, supported by a strong liquidity position. The company issued $400 million in fixed-rate reset subordinated notes in late 2025 to bolster regulatory capital, marking a significant development in its capital structure. While operating cash flow declined markedly in 2025 compared to 2024, free cash flow remained solid due to controlled capital expenditures. Dividend payouts have remained stable with growing share repurchases enhancing shareholder returns. Going forward, growth drivers include sustained net interest margins and fee income expansion, though risks from interest rate volatility and credit quality persist.

Company Overview and Recent Growth

BOK Financial Corporation operates as a regional financial services provider emphasizing traditional banking activities alongside diversified financial products. Its business model centers on generating net interest income (NII) and fee-based revenue streams, benefitting from an established customer base primarily located across the South Central U.S.

The company reported net income of approximately $578 million for the fiscal year ended December 31, 2025 [F1], representing an increase of roughly 10.4% compared with the prior year’s $524 million. This growth underscores a successful execution amid competitive regional banking conditions and above-average net interest margin expansion noted in recent earnings commentary [N12][N1].

While revenue figures are not directly available from disclosures, the emphasis on NII and fees aligns with sector trends where rising benchmark rates have supported loan yields without proportional increases in funding costs, thereby expanding spreads .

Financial Performance Summary

The table below consolidates key financial metrics spanning four years through FY2025 based on SEC-filed XBRL data:

Historical performance (annual)

| FY | Net ($mm) | CFO ($bn) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 578 | 0.7 | 164 | +10.4% |

| 2024 | 524 | 1.4 | 172 | -1.4% |

| 2023 | 531 | 0.1 | 166 | +2.0% |

| 2022 | 520 | 5.1 | 215 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, OpInc. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($bn) |

|---|---|---|---|

| 2025 | 148 | 413 | 0.6 |

| 2024 | 143 | 90 | 1.3 |

| 2023 | 143 | 177 | -0.1 |

| 2022 | 144 | 155 | 4.9 |

Source: SEC companyfacts cache [F1].

Note: Revenue and operating income unavailable from source data [F1].

Analysis of Cash Flows and Capital Allocation

Operating cash flow (CFO) showed significant volatility with a marked decrease from roughly $1.43 billion in FY2024 to $740 million in FY2025 [F1]. This drop likely reflects normalization following an unusually high inflow period rather than operational deterioration per se.

Despite this CFO contraction, capital expenditure management was consistent, resulting in free cash flow approximating $575 million in FY2025 (CFO minus Capex). This healthy FCF facilitates ongoing shareholder returns.

Dividend payments have remained stable around $143–148 million annually over recent years, supporting steady income for investors [F1][S21]. Notably, share repurchases surged dramatically to over $413 million in FY2025 from under $90 million the previous year, indicating management's commitment to returning excess capital amid robust earnings performance.

Return on equity for FY2025 was close to 9.8%, reflecting effective utilization of equity capital supporting earnings growth [F1]. The steady increase in equity base over the period—from about $4.7 billion in FY2022 to nearly $6 billion—suggests disciplined capitalization.

Capital Structure Developments

In November 2025, BOK Financial issued $400 million of fixed-rate subordinated notes due in 2040 at a coupon rate of approximately 6.108% [S9][S15]. These notes qualify as Tier II regulatory capital under banking regulations and bolster the firm’s capital adequacy ratios.

This strategic debt issuance enhances balance sheet flexibility while allowing continuation of shareholder-friendly policies such as dividends and buybacks without excessive dilution or strain on core liquidity.

Liquidity remains healthy with cash plus cash equivalents reported at around $2.84 billion as of end-2021 [F1][S7]. Though more current liquidity snapshots post-debt offering are not delineated explicitly, the company’s regular investor communications affirm ample liquidity buffers supportive of lending operations.

Drivers of Future Growth

Company-specific catalysts include sustained momentum in NII — fueled by historically higher interest rates which improve lending yields — alongside growth in fee income from diversified financial services such as asset management and treasury solutions [N12][N1].

Additionally, geographic diversity across mid-sized markets reduces concentration risk while maintaining strong client relationships given BOK Financial’s regional franchise moat [S5].

Growth may however moderate subject to macroeconomic factors: potential volatility in short-term rates could dampen net interest margins if deposit betas rise or loan demand softens [S6]. Credit quality trends remain critical given any cyclical headwinds affecting borrower performance could pressure provisions.

Near-Term Forecasts and Milestones to Monitor

While explicit guidance is not present within filings or news releases examined here, upcoming data points worth tracking include quarterly NII growth relative to peers (many regional banks recently reported positive beats on this measure), loan portfolio quality metrics including nonperforming assets ratios, and capital ratio trends given ongoing subordinated note amortizations .

Investor presentations released periodically provide insights into evolving strategic priorities and risk management practices [S3][S17][S20]. Monitoring both regulatory developments impacting capital standards and evolving macroeconomic indicators will be crucial for assessing BOKF's trajectory.

Industry Contextualization

The U.S regional banking industry continues navigating shifts from prolonged low-rate environments toward an era of elevated rates impacting deposit pricing pressures ('deposit beta'), loan repricing capacity, and hence net interest margin (NIM) elasticity—a focal point for profitability analyses within sector coverage .

Fee-based revenues serve as important stabilizers against NIM compression cycles; BOK's ability to expand these offerings strengthens its competitive moat amid increasing digital service adoption.

Conclusion

By blending prudent capital management—including a sizable subordinated debt issuance—with robust earnings generation primarily from net interest income and fees, BOK Financial has positioned itself strongly entering 2026.

Although some deceleration in operating cash flows warrants attention, free cash flows remain solid enabling continued dividends and accelerated share repurchases that enhance shareholder value deployability.

Key risks related to interest rate movements and credit quality require vigilant oversight but appear well-managed given BOK's conservative footing bolstered by ample liquidity and regulatory capital compliance.

Disclaimer: This analysis is provided solely for informational purposes based on publicly available data as of early 2026; it does not constitute investment advice or recommendations regarding securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments