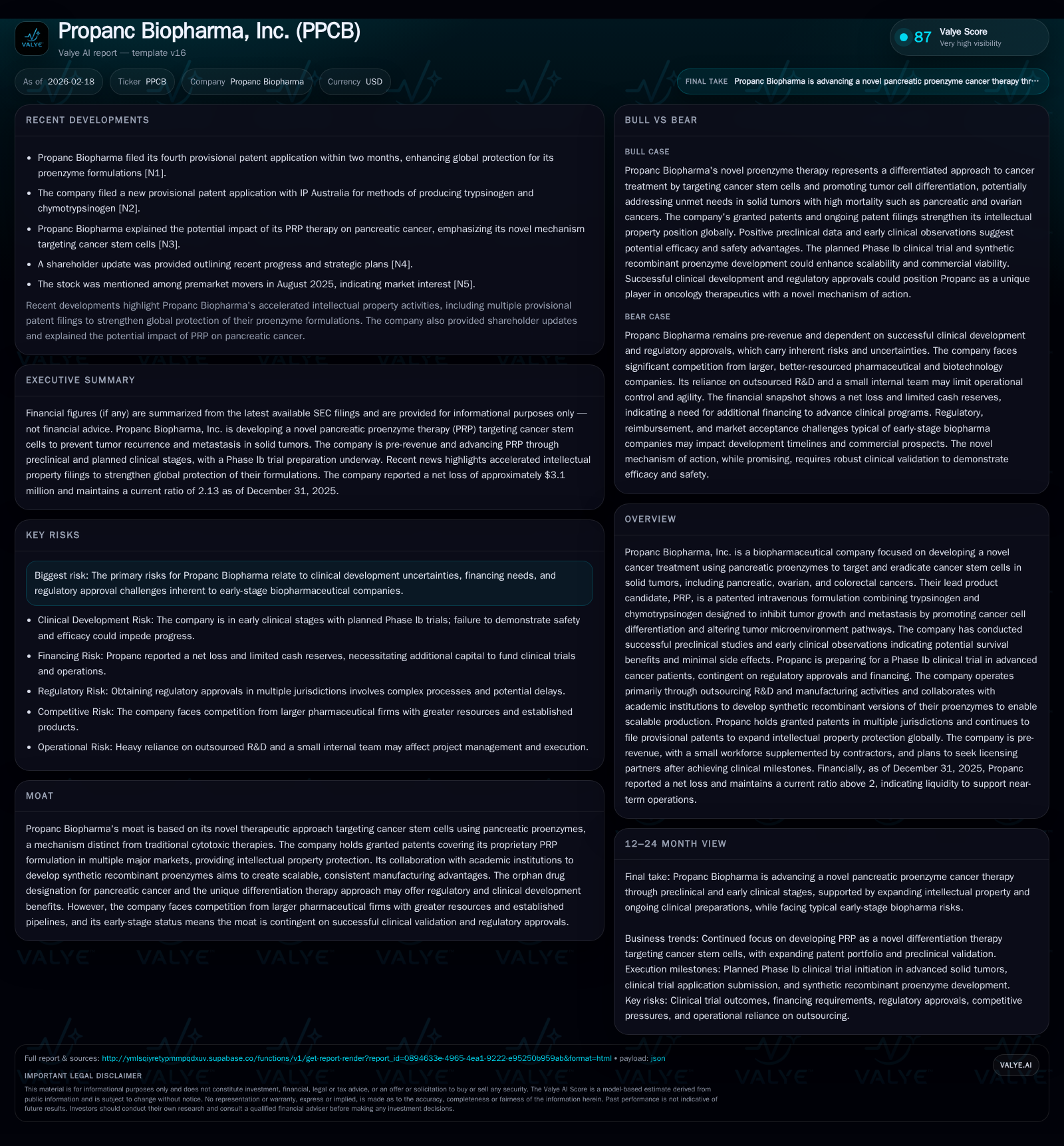

Propanc Biopharma Advances Proenzyme Therapy with Bold Patent Strategies and Clinical Ambitions

Propanc is advancing a novel cancer treatment leveraging pancreatic proenzymes, backed by accelerating patent filings and clinical trial preparations amidst significant financial challenges.

Propanc Biopharma, an early-stage biotech firm, is pioneering a unique therapeutic approach targeting cancer stem cells in solid tumors using its patented proenzyme formulation, PRP. Recent months have seen a surge in patent applications reinforcing its intellectual property moat, while the company prepares to initiate a Phase Ib clinical trial contingent on financing and regulatory approvals. Historically, Propanc has operated at escalating losses driven by increasing R&D investments typical of early clinical development. Its financials reveal reasonable short-term liquidity but limited cash reserves and deeply negative returns on equity, underscoring capital constraints as it advances toward key development milestones.

Innovative Therapeutic Platform Rooted in Pancreatic Proenzymes

Propanc Biopharma’s lead asset, PRP, is a patented intravenous formulation combining pancreatic proenzymes trypsinogen and chymotrypsinogen. This unique approach targets cancer stem cells within solid tumors such as pancreatic, ovarian, and colorectal cancers by promoting differentiation of these cells and altering tumor microenvironment pathways that govern metastasis and tumor growth [S1][N3]. The therapeutic premise diverges from conventional cytotoxic agents by focusing on cancer stem cell eradication — a subpopulation responsible for recurrence and drug resistance — providing potential for sustained suppression of tumor progression.

Preclinical validation conducted by Propanc reveals promising anti-cancer effects with minimal observed side effects. Additionally, PRP benefits from orphan drug designation granted by the FDA for pancreatic cancer in 2017 [S11][S18], affording regulatory incentives such as research grants, protocol assistance, tax credits, and potential market exclusivity. The orphan status underscores the high unmet medical need in pancreatic cancer due to low survival rates despite advances in standard treatments.

Academic collaborations underpinning Propanc's platform also focus on synthesizing recombinant proenzymes to ensure scalable, consistent manufacturing—an industry-critical factor given the complexity of biologics production [S14].

Historical Financial Trajectory: Operating Losses Widen Amid R&D Investment

In line with typical early-stage biopharmaceutical companies prioritizing R&D over revenues (which are not reported), Propanc has consistently operated at net losses historically with escalating expenditures aligned to its clinical ambitions. The fiscal year ending June 30, 2025 saw an unprecedented widening of operating loss to approximately $57.3 million compared with $1.54 million in FY2024 — a striking increase driven primarily by preparation costs for the planned Phase Ib clinical study including contract research organization (CRO) engagements, drug manufacture scaling, assay development, and site preparations [F1][S1].

Net income displayed a similar trajectory dropping to a negative $58.9 million in FY2025 from roughly -$1.82 million in the prior year. Meanwhile, operating cash flow losses improved year-over-year but remained negative at around -$405k [F1]. Equity increased markedly in FY2025 to over $13.9 million from negative equity positions previously, likely reflecting capital raises aimed at backing clinical development.

Given the persistent heavy losses relative to equity base, return on equity (ROE) remains deeply negative (~-424%), reflecting investment risk inherent in early-stage oncology drug developers before revenue generation (see Table below).

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -59 | -405168 | -57 | -3136.6% |

| 2024 | -2 | -935118 | -2 | +31.6% |

| 2023 | -3 | -1105251 | -2 | -0.1% |

| 2022 | -3 | -1436304 | -2 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Capex, Div, Buybacks, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -423.7 |

| 2024 | 48.2 |

| 2023 | 85.4 |

| 2022 | 87.9 |

Source: SEC companyfacts cache [F1].

Note: Revenue data not available; Capex negligible; dividends paid and share buybacks not reported in provided tags.

Accelerating Intellectual Property: Patent Activity and Global Protection

Propanc has notably intensified its patent filings early in 2026 with four provisional applications submitted within two months encompassing novel formulations and proprietary bioprocessing methods related to trypsinogen and chymotrypsinogen production [N1][N2]. This surge reflects a proactive IP strategy aiming to fortify barriers against competitive encroachment from larger pharmaceutical players who dominate oncology pipelines.

The existing patent portfolio includes granted claims across major jurisdictions including Europe (validated in multiple countries), Japan, Australia, Hong Kong among others [S16][S27]. This global coverage supports anticipated commercial expansion once clinical and regulatory milestones are achieved.

Close collaboration with academic institutions such as universities of Jaén and Granada complements efforts by developing synthetic recombinant versions of the proenzymes enhancing yield titers for scalable manufacturing—critical for consistent GMP supply required in clinical trials and eventual market supply [S14][S24]. Such scientific partnerships also generate mechanistic insights enabling follow-on drug discovery opportunities potentially broadening Propanc’s anticancer pipeline.

Pipeline Progress and Upcoming Clinical Milestones in Advanced Tumors

Following successful preclinical studies showing promising anti-tumor effects without significant toxicity [S28], Propanc is actively preparing for regulatory submissions to initiate a First-In-Human Phase Ib clinical trial projected for the second half of calendar year 2026 [S1][N4]. This study will enroll patients with advanced solid tumors — predominantly pancreatic and ovarian cancers — focusing primarily on safety profile characterization through multiple ascending dose protocols alongside pharmacokinetic assessments.

Prior to patient dosing initiation expected around October 2026 [S29], completion of comprehensive Investigational Medicinal Product Dossier compilation alongside selection of CROs and analytical labs is required during early-mid 2026. Trial sites include the Peter MacCallum Cancer Centre in Melbourne—Australia’s premier oncology center known for strict adherence to good clinical practice standards [S28].

Due to dependency on successful capital procurement and regulatory clearance across jurisdictions including Australia’s TGA and potentially FDA/EMA pathways (both noted as complex multi-step processes involving extensive documentation review) [S7][S8], timing uncertainty exists around trial commencement. Monitoring CTA submission status and patient enrollment metrics will be key near-term value inflections.

Subsequent plans include expanded Phase IIa trials designed as multi-center proof-of-concept studies evaluating PRP’s efficacy signals post-tolerability confirmation from Phase Ib cohorts [S28].

Competitive Landscape: Differentiation Against Established Oncology Therapies

Within an oncology environment dominated by cytotoxic chemotherapies complemented increasingly by targeted biologics such as monoclonal antibodies or kinase inhibitors , Propanc’s unique positioning stems from engaging cancer stem cells via enzymatic differentiation therapy using pancreatic proenzymes—a mechanism largely unexplored by existing products [S9]. This represents potentially first-in-class innovation which could deliver meaningful improvements in survival or quality of life if future clinical evidence supports current hypotheses.

Nonetheless competitive risk remains salient given entrenched pharmaceutical giants equipped with deep R&D budgets capable of rapid scale-up across global markets as well as accelerated regulatory pathways through investigational combinations. Additionally the reimbursement landscape exhibits intensifying cost containment pressures globally affecting pricing strategies even after product approvals [S4][S5].

The clinical validation bottleneck is pronounced because PRP must demonstrate compelling efficacy beyond safety before adoption gains momentum among oncologists accustomed to established treatment algorithms.

Capital Structure, Cash Flows and Capital Allocation Priorities

At fiscal year-end June 30th 2025 Propanc reported current assets of approximately $7.7 million against current liabilities near $3.62 million yielding a current ratio around 2.13—indicating reasonable short-term liquidity [F1]. However actual cash on hand was substantially lower at roughly $93k as measured on March 31st 2023 indicating constrained immediate liquidity requiring replenishment through capital raises or licensing arrangements.

No dividends or stock repurchases have been undertaken reflecting exclusive focus on preserving capital for ongoing R&D activities including preclinical testing support and upcoming clinical trial initiation [F1][S26]. Operating cash flow remains negative but improved year-over-year suggesting some efficiencies or timing adjustments amid increasing spending commensurate with advancing clinical stage programs.

Investors should watch announcements related to funding rounds or strategic partnerships which will be crucial enablers for sustaining momentum into late-stage studies necessary for pharmaceutical licensing deals or commercialization transitions.

Risks From Regulatory Complexity And Financing Constraints

Propanc faces several risks typical of small biotech firms but accentuated by its development stage:

- Clinical development risks include unknown efficacy outcomes or unforeseen safety signals that may delay or derail progress at any phase [S4][S15].

- Obtaining CTA approvals across multi-national trial sites involves complex regulatory landscapes requiring coordination with FDA (CDER), EMA centralized procedures after Brexit-related changes impacting European trial authorizations [S7][S8].

- Reimbursement uncertainty looms post-market approval since government payors may limit coverage or impose restrictive pricing undermining commercial viability despite favorable safety/efficacy profiles [S4][S5].

- Financing constraints persist given limited cash reserves necessitating external capital injections absent forward guidance thus exposing milestone-driven dilution risk [S26][N4].

- Reliance on contractors amplifies operational dependencies while small internal team size may pose challenges managing technical breadth needed across discovery-to-clinic continuum [S9].

- Competitive pressure from more resource-rich organizations with diverse oncology assets raises barriers for product uptake within entrenched prescribing patterns among clinicians.

These factors require thorough scrutiny when evaluating strategic positioning even as innovative science presents differentiation opportunities.

This analysis leverages publicly available data from SEC filings ([S#]), news releases ([N#]), and company facts snapshot ([F1]). It aims to contextualize Propanc Biopharma’s technological advances alongside financial dynamics without providing investment recommendations or price guidance.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments