BXP, Inc.’s High-Leverage Office Portfolio Faces Economic and Interest Rate Headwinds

BXP's stable revenue growth and concentrated urban portfolio are challenged by rising interest rates, high leverage, and shifting office demand dynamics.

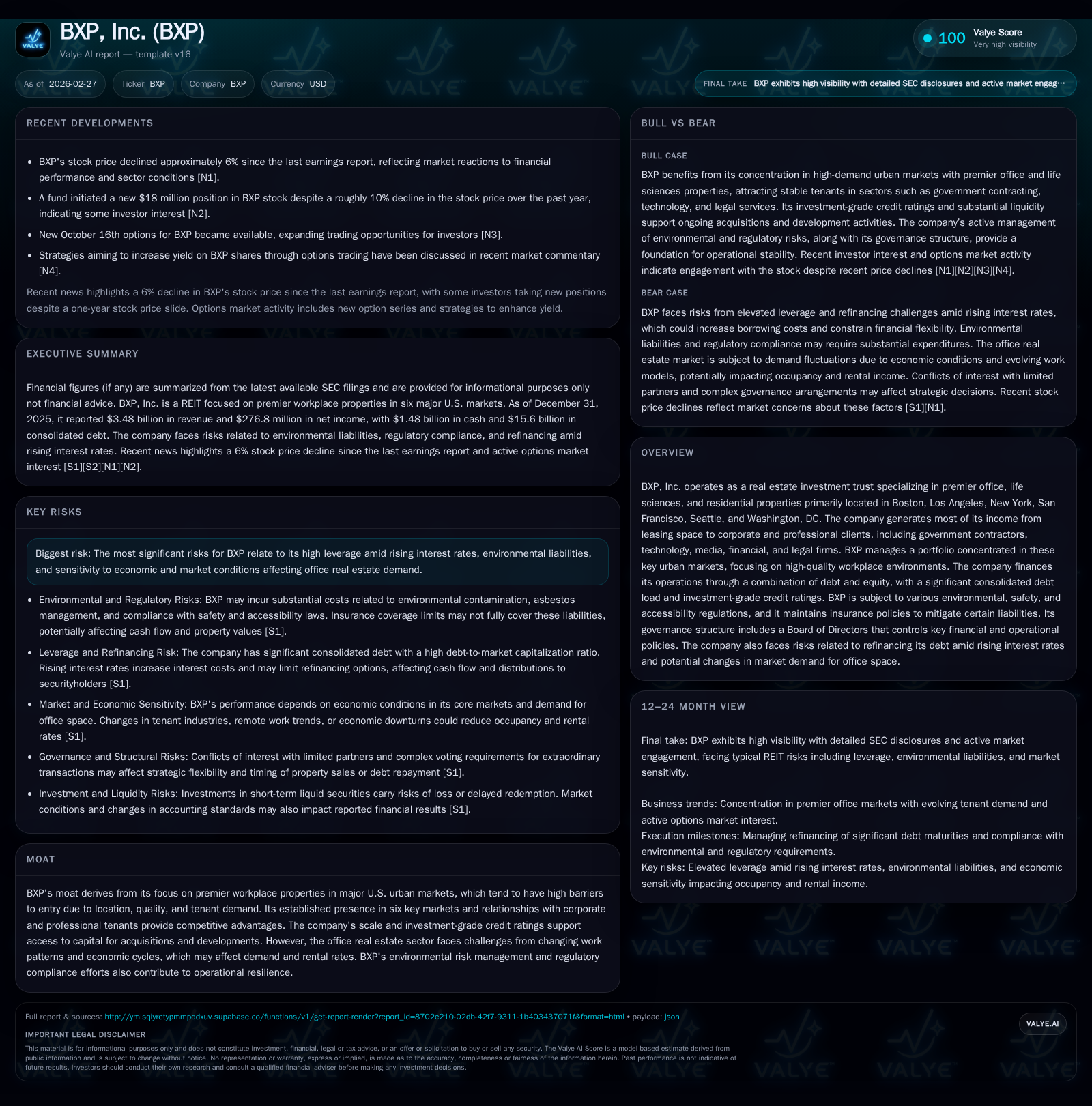

Boston Properties (BXP) operates a premier office-focused REIT concentrated in six major U.S. markets, generating steady revenue growth over recent years. Despite reaching $3.48 billion in revenue for FY2025 and maintaining stable operating cash flow, the company faces pressure from rising interest rates, asset impairments, and leverage risks. Future growth hinges on navigating evolving workplace trends and capitalizing on its urban market foothold, while managing refinancing risks posed by elevated debt levels near $15.6 billion. Monitoring BXP's ability to refinance debt on favorable terms and maintain tenant demand will be critical.

Company Overview

Boston Properties (BXP) is a real estate investment trust specializing in premier office, life sciences, and residential properties concentrated primarily in six major U.S. markets: Boston, Los Angeles, New York, San Francisco, Seattle, and Washington, DC [S1]. The firm generates most of its revenue from leasing space to corporate tenants including government contractors, technology firms, media companies, financial services providers, and legal practices [S1]. This concentration on high-quality workplace environments across top-tier urban centers constitutes BXP’s main competitive edge.

Historical Financial Performance

BXP has exhibited steady top-line growth over the past several years with revenues rising from approximately $3.11 billion in FY2022 to $3.48 billion in FY2025. This corresponds to an approximate compound annual growth rate of around 4% over this period but more specifically a 2.2% year-over-year increase from FY2024 to FY2025 [F1]. Net income has been more volatile; it fell sharply to $14 million in FY2024 influenced heavily by asset impairment charges but rebounded strongly to $277 million in FY2025 [F1][S1]. Operating cash flow has remained resilient around the $1.25 billion mark despite these pressures.

Capital expenditures have fluctuated significantly—a reduction of over 1400% year-over-year from about $50 million spent in FY2024 versus previous years’ capex levels that ranged between $25 million and $97 million [F1]. This drop may reflect project completions or strategic pacing of development spending given the uncertain macroeconomic backdrop.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 3.5 | 277 | 1245 | +2.2% | +1839.5% | |

| 2024 | 3.4 | 14 | 1235 | -51 | +4.1% | -92.5% |

| 2023 | 3.3 | 190 | 1302 | 4 | +5.3% | -77.6% |

| 2022 | 3.1 | 849 | 1282 | 98 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 643 | 5.4 | |

| 2024 | 690 | 1285 | 0.3 |

| 2023 | 688 | 1298 | 3.2 |

| 2022 | 685 | 1185 | 13.8 |

Source: SEC companyfacts cache [F1].

Note: Capital expenditures are negative when reflecting net investment/disposal or accounting classifications.

Debt Profile and Capital Structure

As of February 2026, BXP’s consolidated debt stood at approximately $15.6 billion excluding unconsolidated joint ventures [S4][S8]. Combined with total equity valued near $10.8 billion based on stock price and partnership units outstanding as of the same date, this yields a debt-to-market capitalization ratio of about 59% [S4][S8]. Such leverage levels are significant for a REIT and expose BXP to refinancing risks especially given current elevated market interest rates [S4][S10][S15]. Roughly $2.3 billion of outstanding indebtedness bear variable interest rates with partial hedging via interest rate swaps [S9][S10].

Debt covenants impose limits on total debt-to-assets ratios and require minimum coverage metrics that if breached could precipitate defaults or force unfavorable asset sales [S6][S10][S23]. Moreover, agreements related to tax protection for certain limited partners may restrict flexibility in repaying or refinancing secured debt [S5][S8]. While BXP benefits from investment-grade ratings from two agencies currently [S4], maintaining these ratings is not assured given external volatility.

Operational Moat and Competitive Advantages

BXP’s moat derives largely from its focus on premier workplace properties situated within major metropolitan hubs where barriers to entry are high due to land scarcity, zoning restrictions, and tenant preferences for well-located high-quality office buildings . Established relationships with corporate tenants across multiple sectors—particularly government contracting in Washington DC; technology and media on the West Coast; and financial/legal firms in New York—provide stability internally even as some end markets fluctuate [S1]. Economies of scale enable access to capital for acquisitions or developments at favorable terms.

Industry Trends and Market Risks

The office real estate sector faces fundamental challenges post-pandemic stemming from altered work patterns such as hybrid remote models that compress space requirements or delay lease renewals [N1]. Economic cycles also influence demand volatility especially in cyclical industries that underwrite corporate leases driving occupancy.

Concentration risk is material since almost all revenue flows from six metropolitan areas sensitive individually to downturns driven by federal budget changes (notably Washington DC), technology sector health (West Coast), or financial market sentiment (NYC) [S1]. Additionally, potential regulatory restrictions around rent control for residential components could weigh on those portfolio segments [S22]. Environmental liabilities exist tied to hazardous substance contamination remediation costs which could become substantial despite pollution legal insurance coverage up to $20-$40 million per incident/aggregate respectively depending on claim circumstances [S14].

Growth Outlook and Catalysts

Future growth prospects hinge on BXP’s ability to leverage its sizable presence within these key metros by enhancing building amenities that appeal to evolving tenant needs post-pandemic—such as wellness spaces or smart building technologies—and securing long-term leases that hedge against fluctuating occupancy trends . Strategic acquisitions or select developments can contribute incremental rentable square footage though financing terms may constrain pace temporarily due to tight credit markets.

Monetization of life sciences assets or repositioning select holdings towards emerging industries within innovation districts offer niche upside though require capital deployment balanced against deleveraging priorities . Tenant diversification efforts may soften reliance on more vulnerable sectors.

Capital Allocation & Returns

BXP distributed approximately $643 million in dividends during FY2025 representing a prudent payout considering net income recovery post-impairments and steady operating cash flows [F1][S18][S19]. Free cash flow after capital expenditures is estimated near $1.30 billion reflecting operational robustness despite cutbacks in capex spending likely due to project cycle timing or cost management adjustments [F1].

No recent broad share buyback plans have been publicly announced though some limited redemptions related primarily to employee stock compensation occurred ensuring modest treasury stock movements without significant impact on overall shares outstanding [S2][S18][S19].

ROE based on reported net income over equity stood around a modest estimated ~5% for FY2025 consistent with capital-intensive nature typical for large diversified REITs yet trailing peak periods due partly to heightened impairment provisions seen recently [F1].

What To Watch Going Forward (Analysis)

- Refinancing Risk: Upcoming maturity schedules will test BXP's ability to refinance substantial portions of its ~$15.6bn debt amidst persistently high interest rates which could increase cost of capital materially impacting profitability.

- Leasing Momentum: Lease renewal rates alongside new leasing velocity particularly in tech-influenced West Coast markets will indicate tenant appetite returning or further decline in demand.

- Impairment Charges: Given prior impairments exceeding ~$85 million annually coupled with one unconsolidated JV recording ~$145M 'other than temporary' impairment recently, watch for recurring write-downs signaling asset value pressure.

- Dividend Sustainability: Monitoring ongoing dividend policy relative to operating cash flow headroom amid cyclic pressures will reveal management priorities balancing shareholder return vs balance sheet resilience.

- Regulatory Environment: Changes in environmental laws affecting cleanup obligations or rent control statutes could alter operational costs or net property values especially within residential holdings.

Conclusion

Boston Properties remains a dominant player in U.S. office-centric REITs with geographic concentration providing both moat benefits through location quality and exposure risks tied closely to economic cycles affecting demand for urban workspace post-pandemic disruption. Steady top-line growth paired with strong operating cash flow reflects resilient core operations yet high leverage introduces refinancing vulnerabilities amid rising rates compressing margins.

Investors should follow the company's management execution addressing leasing challenges compounded by sector transformation along with prudent balance sheet management aiming at maintaining investment-grade credit status while funding development pipelines selectively where returns justify incremental risk.

Disclaimer: This report presents an analysis based exclusively on publicly available information without offering investment advice or recommendations regarding buying or selling securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments