GAIA, INC’s Fiscal 2025 Review: Operational Losses, Cash Flow Trends, and Governance Changes

GAIA recorded moderate revenue growth in 2025 but continued to face net losses and liquidity constraints, prompting leadership shifts and recalibrated capital strategies.

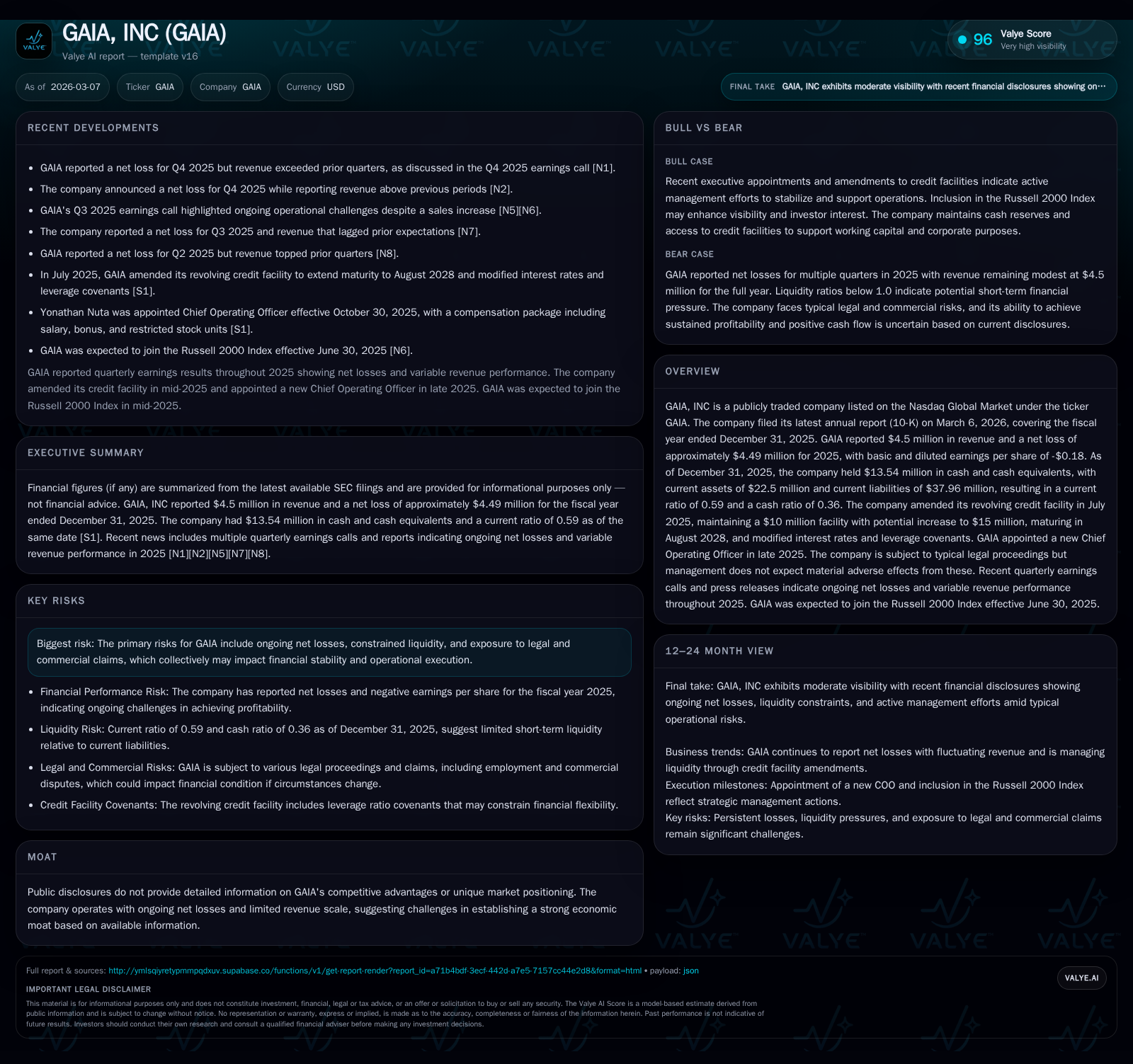

In fiscal 2025, GAIA, INC’s revenue grew by 12.5% to $4.5 million despite persistent operating losses of $5.1 million and a net loss of $4.49 million. Liquidity remained tight, with a current ratio under one and cash reserves at $13.54 million, while the company amended its credit facility extending maturity to 2028 with adjusted covenants. The appointment of Yonathan Nuta as COO in October signals a potential operational pivot amid ongoing legal exposures deemed non-material by management. Capital allocation reflected modest free cash flow compression driven by elevated capex relative to operating cash flows.

Historical Trajectory: Revenue Growth Against Persistent Operating Losses

GAIA's financial performance in the fiscal year ending December 31, 2025, illustrates a nuanced picture where top-line improvement coexists with sustained operating losses. The company reported revenues of $4.5 million for 2025, reflecting an increase of approximately 12.5% from $4.0 million in the prior year, signaling modest organic or strategic growth within its operations [F1]. However, this revenue runway has yet to translate into operating profitability; operating income remained negative at -$5.1 million despite improving roughly 14% from -$5.93 million in 2024 [F1]. This persistent operating loss underscores difficulties leveraging fixed costs or scaling efficiently.

Net income followed a similar trend with a narrower loss of about $4.49 million compared to roughly $5.40 million in the previous year, improving roughly 16.7% year-over-year [F1]. Such margin dynamics indicate an incremental reduction in net burn but remain distant from break-even levels amidst limited revenue scale.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 5 | -4 | 6 | -5 | +12.5% | +16.7% |

| 2024 | 4 | -5 | 7 | -6 | +48.1% | +3.5% |

| 2023 | 3 | -6 | 6 | -5 | -80.8% | |

| 2022 | -3 | 12 | 0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($) | ROE% |

|---|---|---|---|

| 2025 | -377000 | -5.1 | |

| 2024 | 169000 | 1941000 | -6.7 |

| 2023 | 169000 | 596000 | -6.5 |

| 2022 |

Source: SEC companyfacts cache [F1].

Operating leverage remains a challenge for GAIA; incremental revenue gains have yet to offset fixed and variable expenses adequately enough to drive positive operating income.

Recent Executive Appointment Signals Tactical Shift in Operations

A significant governance development occurred in late October 2025 with GAIA appointing Yonathan Nuta as Chief Operating Officer [N1][S12]. Mr. Nuta brings experience from executive product roles at Babylon.com and Fabric.io, and notably had prior tenure with GAIA between October 2016 and May 2021 [S12]. His reintroduction suggests an intent toward operational recalibration possibly focusing on product innovation or efficiency enhancements.

His compensation package comprises a base salary of $425,000 plus an annual target bonus up to the same amount and long-term incentives via RSUs vesting over four years starting late-2026 [S12]. This mix aligns senior leadership incentives closely with long-term shareholder value creation through ROIC improvements or scalable growth.

This leadership movement could mark a pivotal moment for GAIA’s operational trajectory if coupled with disciplined capital management given persistent losses thus far.

Liquidity Headwinds: Examining the Current Ratio, Cash Reserves, and Debt Covenants

Despite steady nominal cash balances totaling $13.54 million as of December-end 2025, liquidity pressures are evident when juxtaposed against current liabilities approximating $37.96 million—resulting in a suboptimal current ratio of roughly 0.59 and a cash ratio near 0.36 [F1]. Such metrics reveal constrained short-term liquidity potentially affecting working capital dynamics.

In July 2025, GAIA amended its credit arrangements with KeyBank National Association refinancing and extending its revolving credit line up to $10 million initially—with potential expansion to $15 million—and rolling maturity forward until August 25, 2028 [S7][S10]. The amendment revised interest rates removing previous SOFR index adjustments and introduced a maximum leverage covenant capped at a debt-to-EBITDA ratio of no more than two times per calculation period.

These covenant modifications reflect lender receptiveness coupled with heightened caution addressing leverage ratio maintenance amid ongoing losses—a common feature when managing extended credit facilities within loss-making entities.

Navigating Ongoing Legal Exposure: Impact on Financial Stability

GAIA acknowledges exposure to various legal proceedings encompassing employment disputes, contractual disagreements, commercial claims, and tax matters including non-income tax related issues per its latest Form 10-K filing [S1][S4]. The company maintains accruals based on probable losses aligned to reasonable estimations under accrual accounting principles.

Management assesses these pending matters would not lead to material adverse effects on financial condition or cash flow assuming outcome probabilities continue as estimated and settled accordingly [S1].[S4]

This risk mitigation stance underscores robust internal controls over contingent liabilities that partially insulate financial stability despite legal uncertainties.

Capital Allocation Review: Deconstructing Cash Flows, Buybacks, Dividends, and ROE

Operating cash flow trended downward by about eighteen percent from $6.92 million in FY24 to $5.67 million in FY25 reflecting some compression of operational liquidity generation despite higher revenues [F1]. Concurrently capital expenditures surged over twenty percent year-on-year reaching $6.05 million indicative of investment scaling possibly towards product or capacity enhancements.

Resultantly free cash flow reflects slight negative absorption around $377 thousand (CFO minus capex), signaling tight funding margins amid incremental growth investment [F1]. GAIA continues abstaining from dividend payments; last dividends recorded date back over a decade ago with only minimal share repurchases seen recently ($169k), suggesting cautious capital deployment prioritizing reinvestment or liquidity preservation over shareholder returns presently [F1][S11][S12].

Return on equity remains negative near -5.1%, consistent with continuing net losses albeit supported by substantial equity reserves above $87 million as of year-end [F1], illustrating shareholder capital base absorbing operational deficits without impairments thus far.

Projected Horizons: Near-Term Milestones and What Investors Should Watch

Explicit guidance is absent within publicly available documents; however key indicators warranting future attention include compliance trajectories against revolving credit facility covenants through August 2028 maturity given leverage caps imposed [S7][S10].[N1] Monitoring quarterly revenue trends alongside operating margin movements will be essential to assess any turnover towards positive operating leverage.

Integration progress under COO Yonathan Nuta’s leadership may yield identifiable shifts in operational protocols or product/service offerings impacting scalability or cost structures post-October appointment [N1].[N2]

Lastly, developments surrounding litigation outcomes may subtly influence contingent liability profiles though management maintains confidence regarding their non-material status.[S4]

Synthesis: Strategic Implications for GAIA’s Path Forward

GAIA’s fiscal results for calendar year 2025 narrate the story of restrained growth intersecting with persistent unprofitability characteristic of early-stage scaling companies confronting multiple operational headwinds simultaneously.

The incremental top-line ascendancy against entrenched losses underscores complex dynamics hampering effective operating leverage capture; meanwhile constrained liquidity metrics signal funding pressures requiring prudent financial stewardship enabled through refreshed credit arrangements.

Executive leadership changes embody proactive measures aimed at catalyzing operational momentum potentially enhancing margins through improved efficiency or innovation output.

On the capital front, steady albeit compressed free cash flow amid rising investment hints at measured discipline balancing growth ambition against funding limits without shareholder return dilution currently.

Overall, GAIA stands positioned at a strategic inflection point where operational execution under new governance combined with vigilant financial management will be critical determinants shaping prospects beyond the immediate fiscal horizon.

This analysis is based exclusively on publicly available SEC filings and corporate disclosures as referenced; it does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments