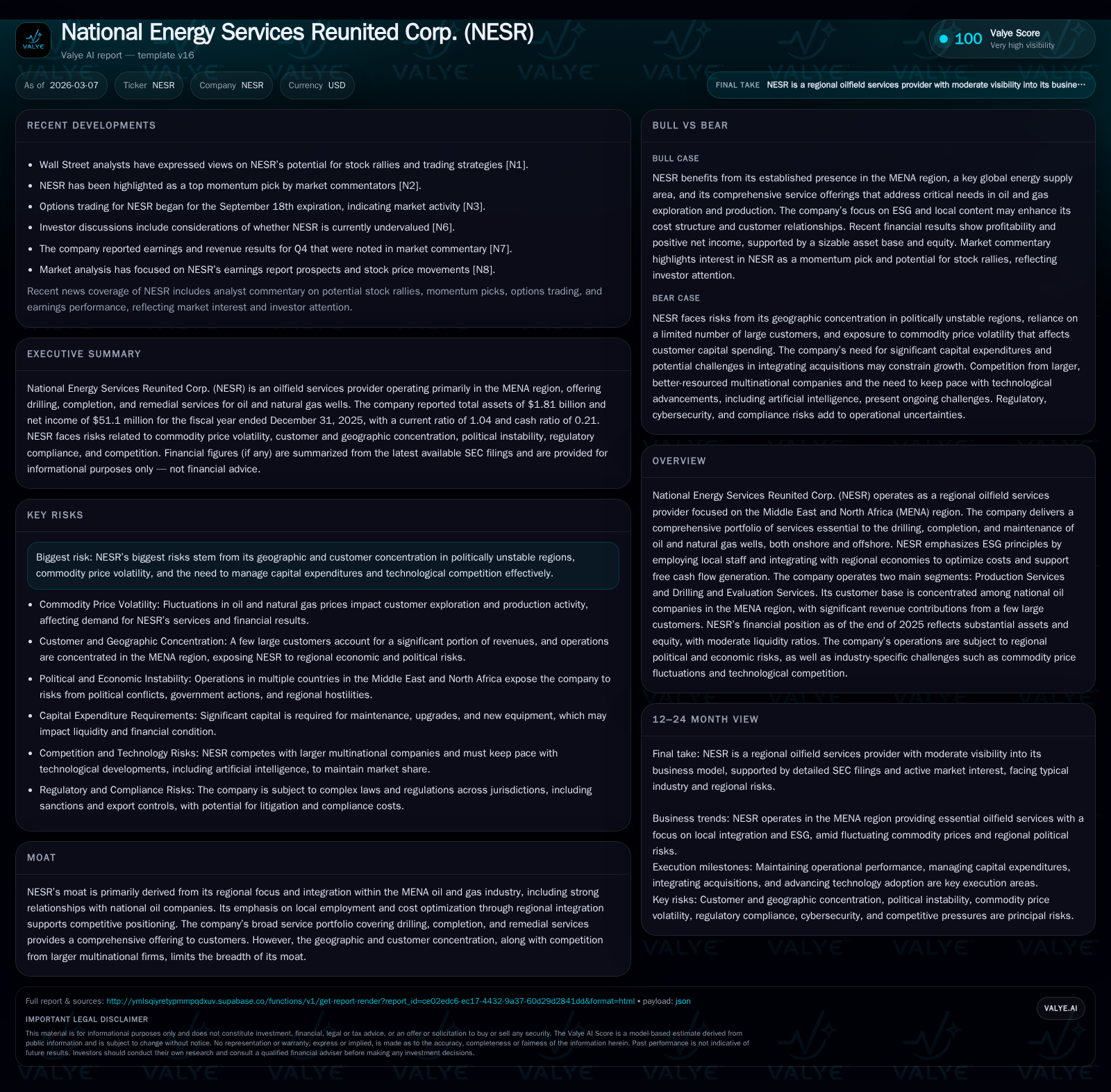

National Energy Services Reunited: Balancing Regional Focus with Growth Ambitions

NESR’s financial path reflects its embedded MENA regional niche, underscored by concentrated customer ties and capital discipline shaping growth prospects.

National Energy Services Reunited Corp. (NESR) operates predominantly in the Middle East and North Africa oilfield services market with notable customer revenue concentration among a few national oil companies. Following a turnaround from losses in 2022, NESR achieved profitability but saw a pullback in operating income in 2025, while generating robust operating cash flows that surpass ongoing capital expenditures. The company faces distinct risks from geopolitical instability, contract concentration, and competitive pressures yet leverages regional integration to sustain cash flow and cost optimization. Future growth hinges on regional upstream activity, contract renewals, and technological adaptation amid cautious market sentiment.

Financial Trajectory: Gains, Setbacks, and Regional Market Dependency

National Energy Services Reunited Corp. (NESR) has demonstrated a marked financial turnaround since FY2022 when it reported an operating loss of $0.9 million and a net loss of $36.4 million. This sharp reversal culminated in a positive net income of $51.1 million for FY2025 despite a notable contraction in operating income compared to FY2024 ($138 million down to $98 million), representing a -28.6% year-over-year decline [F1]. The company's ability to remain profitable amid such fluctuations highlights operational resilience anchored by its regional positioning in the MENA oilfield services industry.

Cash flow generation further accentuates this stability — operating cash flow grew 15.2% YoY to $264 million in FY2025 outpacing capital expenditure increases of 36.5% ($143 million), thereby delivering free cash flow (operating cash flow less capex) near $121 million [F1]. This cash flow strength underscores efficient working capital management despite macroeconomic uncertainties within the MENA region.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 51 | 264 | 98 | 143 | -33.0% |

| 2024 | 76 | 229 | 138 | 105 | +506.6% |

| 2023 | 13 | 177 | 81 | 68 | +134.5% |

| 2022 | -36 | 93 | -1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) |

|---|---|

| 2025 | 121 |

| 2024 | 124 |

| 2023 | 109 |

| 2022 |

Source: SEC companyfacts cache [F1].

Customer Concentration and Its Implications for Revenue Stability

NESR’s business model substantially depends on a limited set of major national oil companies (NOCs) based primarily within the MENA region. According to disclosures for FY2023 to FY2025 periods, four customers contribute approximately 49%, 54%, and 44% of consolidated revenues respectively—with the top client alone accounting for close to half of total revenues [S4]. This concentration anchors NESR's relationship moat by fostering deep integration with key regional players but inherently confines diversification.

This concentration carries material risk profiles referred to as "contract churn risk" where termination or renegotiation of any significant contract could materially impact revenues. Additionally, geopolitical instabilities inherent to MENA elevate such risks given that these customers are subject to government decision-making processes influenced by volatile political climates [S4][S12]. Thus while concentrated ties reinforce NESR’s competitive positioning locally via long-standing relationships and localized operations,

this exposes revenue streams to potential abrupt disruptions absent client diversification.

Assessing Future Growth Potential in the MENA Oilfield Services Market

Looking ahead into the broader energy landscape where NESR operates—the region continues upstream investment momentum as several countries pursue new exploration and production expansion plans detailed in publicly available forecast commentary ([N1], [N2]) and internal strategic filings ([S1], [S10]). Analysts convey measured optimism around NESR’s revenue growth prospects tied primarily to Production Services segment expansion and integrated project offerings targeting sustained NOC capital expenditure.

However notable constraints persist including geopolitical unpredictability highlighted by ongoing tensions involving Iran and neighboring states as well as regulatory uncertainties imposing compliance burdens ([S8], [S10], [N9]). Moreover technological competition from multinational service providers capable of introducing advanced drilling evaluation tools or AI-enhanced reservoir analytics poses incremental pressure on NESR to continuously innovate or risk losing market share ([S17]).

Hence future growth is bounded both by external economic-political factors and internal capabilities emphasizing adaptation while leveraging its entrenched regional presence.

Capital Structure, Liquidity, and Financial Risk Management

As of December 31st, 2025 NESR held approximately $312 million in borrowings subject primarily to floating interest rates tied to SOFR or SAIBOR benchmarks plus margins ranging from approximately 2.6-3.0%. These loan agreements incorporate restrictive covenants including maximum leverage ratios (Net Debt/EBITDA capped near 3.50x), minimum debt service coverage ratios above 1.25x and interest coverage requirements no lower than EBITDA/Interest of 4x ([F1], [S5], [S6], [S7]).

Liquidity metrics indicate current assets at $630 million against current liabilities nearing $605 million yielding a current ratio roughly around 1.04—a ratio signaling adequate short-term liquidity but little excess buffer if stressed against adverse macro conditions ([F1]). The covenants limit subsidiaries’ ability to freely distribute funds upstream potentially constraining holding company level flexibility.

Floating rate exposure means rising global interest rates could increase finance costs materially influencing net margins under downturn scenarios so active refinancing strategies or swift deleveraging would be critical levers going forward.

Cash Flow Dynamics and Capital Expenditure Trends

Robust operating cash flows exemplify NESR’s capacity for self-funding maintenance plus growth investments—$264 million generated in FY2025 represented a +15.2% improvement versus prior year despite profitability headwinds ([F1]). Company spending on capital expenditures jumped sharply (+36.5%), reflecting investments likely segmented between maintenance capex—needed upgrades/refurbishment especially relevant across MENA operations—and growth capex targeting expansion or technology enhancements.

Free cash flow emerges as substantial at roughly $121 million annually enabling the company discretionary capacity albeit without declared dividends or share repurchases currently noted ([F1]). Strong cash flow profiles strengthen the company’s ability to service debt obligations while simultaneously supporting essential asset upkeep amid constrained capital budgets within the sector.

What Investors Should Watch: Contract Renewals, Market Conditions, and Technological Advances

Key upcoming catalysts lie chiefly in contract renewal outcomes with principal NOCs amid altered pricing or scope parameters representing pivotal inflection points for top-line sustainability ([N4],[N9],[S8],[S12]). Given dependency on these contracts—any substantial deleveraging could impair revenues abruptly.

Regulatory developments related to ESG standards may impose additional compliance costs or operational changes across NESR’s footprint while technological advancement efforts—particularly AI-driven drilling evaluation tools—bear watching as potential differentiators enhancing competitive positioning or eroding incumbent advantage elsewhere ([N4],[N9],[S8],[S17]).

Lastly geopolitical dynamics including conflict flare-ups or sanctions regimes affecting trade flows will remain perennial systemic risks warranting continual monitoring.

Concluding Observations on NESR’s Strategic Positioning and Investment Considerations

NESR occupies a clear niche role as an indigenous MENA-centric oil services provider whose broad service suite across drilling/completions/production integrates tightly with local economies—enabling cost efficiencies unavailable to many multinationals (). This localized business model delivers resilient operational cash flows evidenced financially despite considerable political-economic headwinds.

Nonetheless heavy customer concentration paired with geographic exposure underscores latent vulnerabilities requiring prudent contract management and diversification initiatives overtime ([S4],). Meanwhile elevated capex demands necessitate balancing reinvestment priorities with debt servicing obligations given existing leverage profiles ([F1],).

Investor focus should center on execution against contract renewals with major NOCs paired with steps toward technology adoption advancing service differentiation coupled with steady capital structure stewardship—factors central to unlocking sustainable future growth trajectories amid inherent sector cyclicality ([N3],[N4],).

This report is prepared for informational purposes only based on publicly available data; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments