NI Holdings’ Financial Strains and Strategic Retrenchment in Regional P&C Markets

NI Holdings confronts declining profitability and revenue contraction amid strategic exits from non-standard auto insurance, reshaping its regional insurance focus.

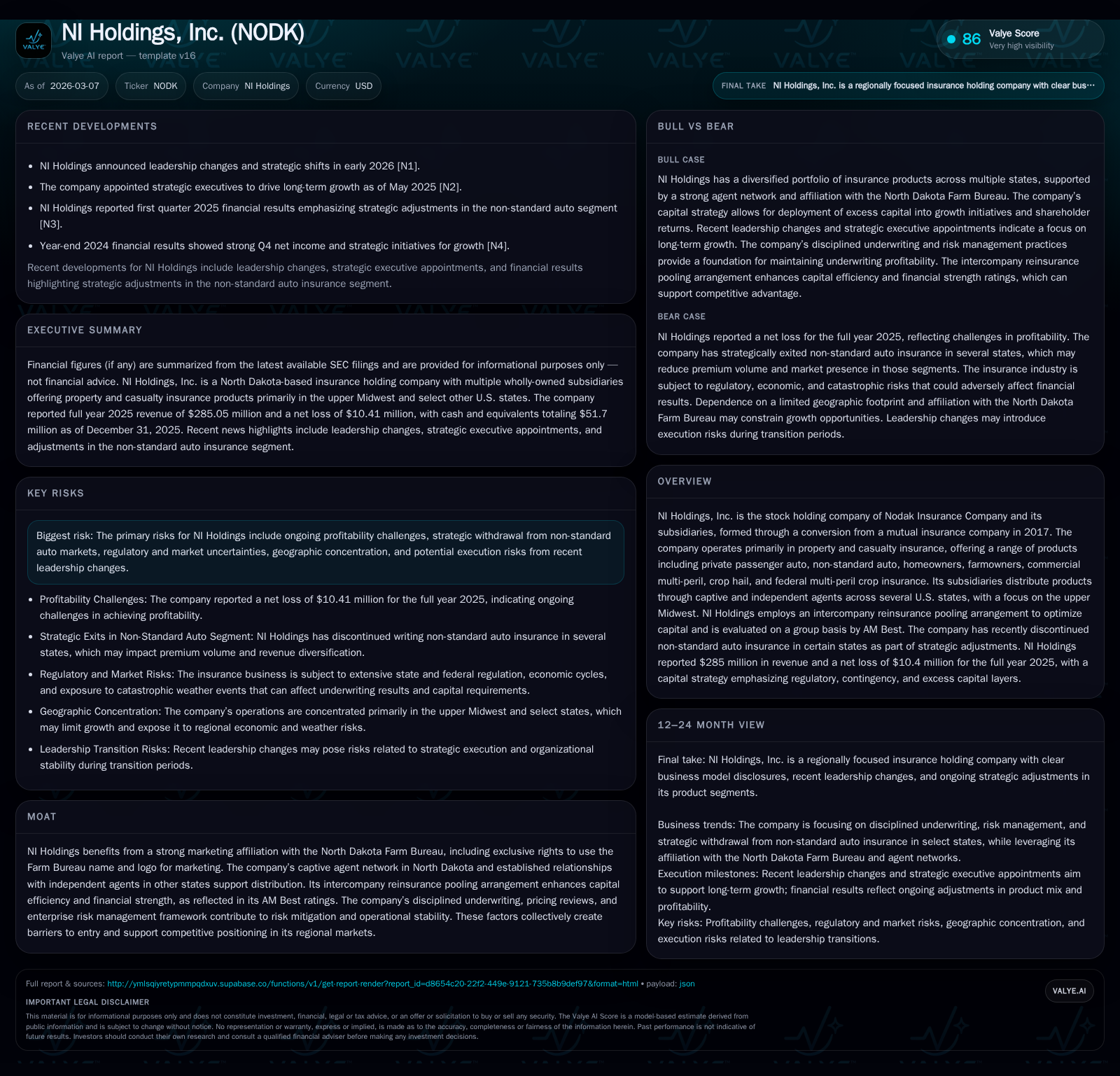

NI Holdings’ revenue declined to $285 million in 2025, down 12.3% year-over-year, alongside a significant widening of net losses to $10.4 million driven largely by strategic business exits and adverse underwriting results [F1]. The company has exited non-standard auto insurance in key states to stem persistent losses, focusing instead on core property & casualty lines supported by its captive and independent agent networks in the Upper Midwest [N1][F1]. Its capital strategy hinges on intercompany reinsurance pooling and disciplined risk management, yet operating cash flow turned sharply negative signaling operational challenges [F1][S1]. Leadership changes announced in early 2026 highlight execution risks as NI Holdings recalibrates its regional footprint and seeks to restore underwriting profitability [N1].

Financial Trajectory: Recent Performance Trends and Underlying Drivers

NI Holdings has experienced significant headwinds over the past three years culminating in a marked revenue contraction from $365.7 million in 2023 to $285.0 million in 2025—a decline of approximately 22% over the period—and a steep deterioration of profitability metrics. Specifically, net losses widened substantially to -$10.4 million for the full year 2025 compared to -$6.06 million in 2024, representing a near tripling of losses year-over-year despite prior improvements from previous multi-year deep losses (-$53 million in 2022) [F1]. This erosion reflects both the deliberate strategic exit from unprofitable segments—namely non-standard auto insurance—and elevated claims costs including catastrophe-related loss volatility.

This topline shrinkage was accompanied by an unwinding of positive operating cash flows recorded at $38.5 million in 2024 back into sharply negative territory (-$15.3 million) in 2025, underscoring operational liquidity strain originating primarily from underwriting setbacks rather than investment portfolio weaknesses given stable dividend income from investments [F1][S1]. Capital expenditure remained subdued reflecting conservative asset deployment priorities amidst financial retrenchment.

The discontinuation of non-standard auto products in certain states has materially impacted premium volumes, while claims severity pressures across retained lines continued to push loss ratios higher despite intensified underwriting discipline and pricing adequacy reviews as part of their enterprise risk management framework.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 285 | -10 | -15 | 217000 | -12.3% | -71.8% |

| 2024 | 325 | -6 | 39 | 991000 | -11.1% | -10.7% |

| 2023 | 366 | -5 | 26 | 974000 | +12.7% | +89.7% |

| 2022 | 324 | -53 | -30 | 1162000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) |

|---|---|---|

| 2025 | 7 | -15 |

| 2024 | 8 | 38 |

| 2023 | 25 | |

| 2022 | -32 |

Source: SEC companyfacts cache [F1].

Table: Historical Financial Summary: FY2022–2025 Revenue, Net Income, Operating Cash Flow, Capex (with YoY % changes) [F1]

Strategic Retrenchment: Exiting Non-Standard Auto and Focused Market Priorities

The company's decision announced around early 2026 to exit non-standard auto insurance lines in specific states such as Arizona and Illinois represents an explicit effort to curtail persistent underwriting losses linked with that segment reported under subsidiaries Primero Insurance Company and Direct Auto Insurance Company [N1][F1]. This retreat aims at restoring price adequacy and underwriting rigor through selective market pruning.

Previously active across multiple jurisdictions including key but highly competitive non-standard auto markets like Illinois—which had notable premium withdrawal impacting nearly $55 million direct premiums from that state alone down from $78 million—this contraction concentrates NI Holdings' footprint primarily within its strongerholds of North Dakota, South Dakota, Nebraska, Minnesota, and parts of Arizona now excluding non-standard auto lines where performance was subpar [S10][N1].

Such restructuring is supported by calibrated adjustments within their intercompany reinsurance pooling arrangement which benefits from diversified retention ($20 million per event) balanced against substantial excess-of-loss protections exceeding $120 million annually—optimized for the evolving risk profile induced by this portfolio realignment [S23][S1]. This approach reduces capital strain while maintaining financial strength metrics essential under AM Best oversight.

Growth Outlook: Opportunities and Headwinds in Core Product Lines

Post-retrenchment, growth prospects revolve around leveraging established property/casualty products such as homeowners’, farmowners’, better-performing private passenger auto (standard segment), commercial multi-peril policies as well as federal crop insurance offerings administered via affiliated American Farm Bureau Insurance Services (AFBIS) partnerships with deep ties to agricultural communities [N1][S21].

Leveraging exclusive marketing affiliation rights with the North Dakota Farm Bureau—a recognized durable moat—enables targeted outreach within rural economies where personal relationships between agents and clients compound retention rates and new business development potential . Accordingly, strengthening captive agents’ penetration complemented by independent agents’ network expansion remains central.

However, material headwinds persist notably stemming from geographic concentration vulnerabilities exacerbated by unpredictable severe weather events tied to emergent climate risks that inflate catastrophe loss frequency/severity beyond modeled assumptions impacting insurance industry-wide reinsurance pricing dynamics unfavorably; these remain key downside factors needing continual monitoring under NI's enterprise risk management protocols [S16][S26][S1].

Risk Management and Capital Optimization via Reinsurance Pooling

A critical structural element underpinning NI Holdings’ capital efficiency is its intercompany reinsurance pooling system effectively distributing catastrophe risk among its affiliated insurers while maintaining a $20 million event retention limit; beyond this threshold lies an aggregate excess-of-loss protection exceeding $120 million placed each policy year ensuring substantial loss absorption capacity without draining statutory capital reserves unnecessarily[S23][F1].

This layering arrangement offers several advantages—it smooths out volatility caused by large loss events enabling improved capital planning accuracy; maintains favorable AM Best financial strength ratings necessary for competitive positioning; and facilitates regulatory compliance vis-à-vis state surplus requirements while optimizing cost of risk transfer through calibrated treaty structures aligned with evolving risk appetites.

Capital Allocation: Dividends, Cash Flows, and Shareholder Returns

Despite ongoing underperformance at the net income level (-$10.4 million), NI Holdings maintained dividend payments albeit reduced modestly by approximately19% year-over-year to $6.7 million reflecting a cautious capital preservation stance amid shrinking free cash flow which stood at roughly negative $15.5 million (operating cash flow minus capex) for fiscal year ended December 31, 2025[F1][S9].

Return on equity approximated negative -3.4%, illustrating ongoing tension between shareholder expectations for returns against earnings erosion driven largely by underwriting losses rather than investment activities whose income streams remain relatively steady.

The company’s capital deployment philosophy underscores prioritization of:

- Preservation of regulatory capital buffers mandated across domiciliary states;

- Strategic reinvestment in existing product lines aligned with profitable growth catalysts;

- Opportunistic acquisitions consistent with risk-adjusted return targets;

- Controlled shareholder distributions balanced against liquidity constraints[S9][S17].

Given this backdrop combined with deteriorating operating cash flow trends signaling possible liquidity tightening scenarios absent significant improvement or external capital injections signals risk for dividend sustainability beyond near term periods unless underwriting stabilization is achieved.

Governance Shifts: Leadership Changes Impacting Execution Risk

In March 2026 NI Holdings publicly disclosed leadership transitions encompassing executive roles pivotal for strategy execution reflecting increased focus on turnaround pathways following recent operational setbacks[N1]. Such management refresh initiatives inherently bear execution risks including potential disruption to ongoing projects and cultural shifts challenging continuity but may also inject necessary impetus towards innovation and organizational realignment in response to market realities.

These governance adjustments must be carefully observed for their impact on pace and quality of implementation relating to pricing adequacy enhancements, product rationalization efforts especially concerning remaining P&C lines focus areas, reinsurance negotiations renewal strategies as well as enterprise wide cost control programs crucial for restoring profit margins.

Investment Portfolio Strategy amidst Market Volatility

NI Holdings’ investment assets are predominantly allocated into high-quality liquid fixed income instruments managed externally by Conning Inc., designed principally to support claims liabilities with sound asset-liability matching principles[S5]. This fixed income portfolio comprises diversified holdings across U.S government bonds, municipal bonds (taxable/exempt), corporate securities including agency mortgage-backed securities minimizing liquidity risks during claim payment cycles.

Smaller allocations to private debt placements and equity securities provide yield enhancement opportunities albeit at the cost of increased volatility requiring vigilant credit surveillance processes applying discounted cash flow models consistently reviewing allowance needs for potential impairments[S12][S24]. Effective duration management ensures interest rate sensitivity aligns with forecasted liability runoff horizons thereby stabilizing book values under fluctuating interest rates.

Such structured approach mitigates counterparty default threats while preserving overall liquidity profile essential under cyclically challenged insurance operating conditions.

What to Watch Forward: Key Metrics and Potential Catalysts

No formal management guidance exists explicitly forecasting turnaround milestones; hence analysis must prioritize directional indicators such as:

- Improvement trends in combined ratios notably underwriting loss ratios driven by claims frequency/severity control;

- Expense ratio containment evidencing successful cost optimization endeavors;

- Stability and renewal terms of catastrophe excess-of-loss reinsurance programs impacting net retained exposure costs;

- Regulatory developments potentially altering market conduct rules or premium rate approvals affecting pricing flexibility[S6];

- Competitive behavior dynamics within NI Holdings’ concentrated Upper Midwest markets influencing growth levers;

- Efficacy of newly instated leadership strategies reflected through quarterly operational KPIs[N1][F1].

Rigorous monitoring across these dimensions will illuminate whether NI Holdings can stem current financial strains while positioning for modest sustainable growth or if further retrenchment or restructuring remains necessary.

This analysis is prepared solely for informational purposes grounded exclusively on publicly available data as cited without offering investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments