Bridger Aerospace's Strategic Flight: From Turnaround to Growth Trajectory

Bridger Aerospace transitioned from steep losses to profitability through fleet enhancement, technology integration, and refinancing, setting the stage for growth amid wildfire industry volatility.

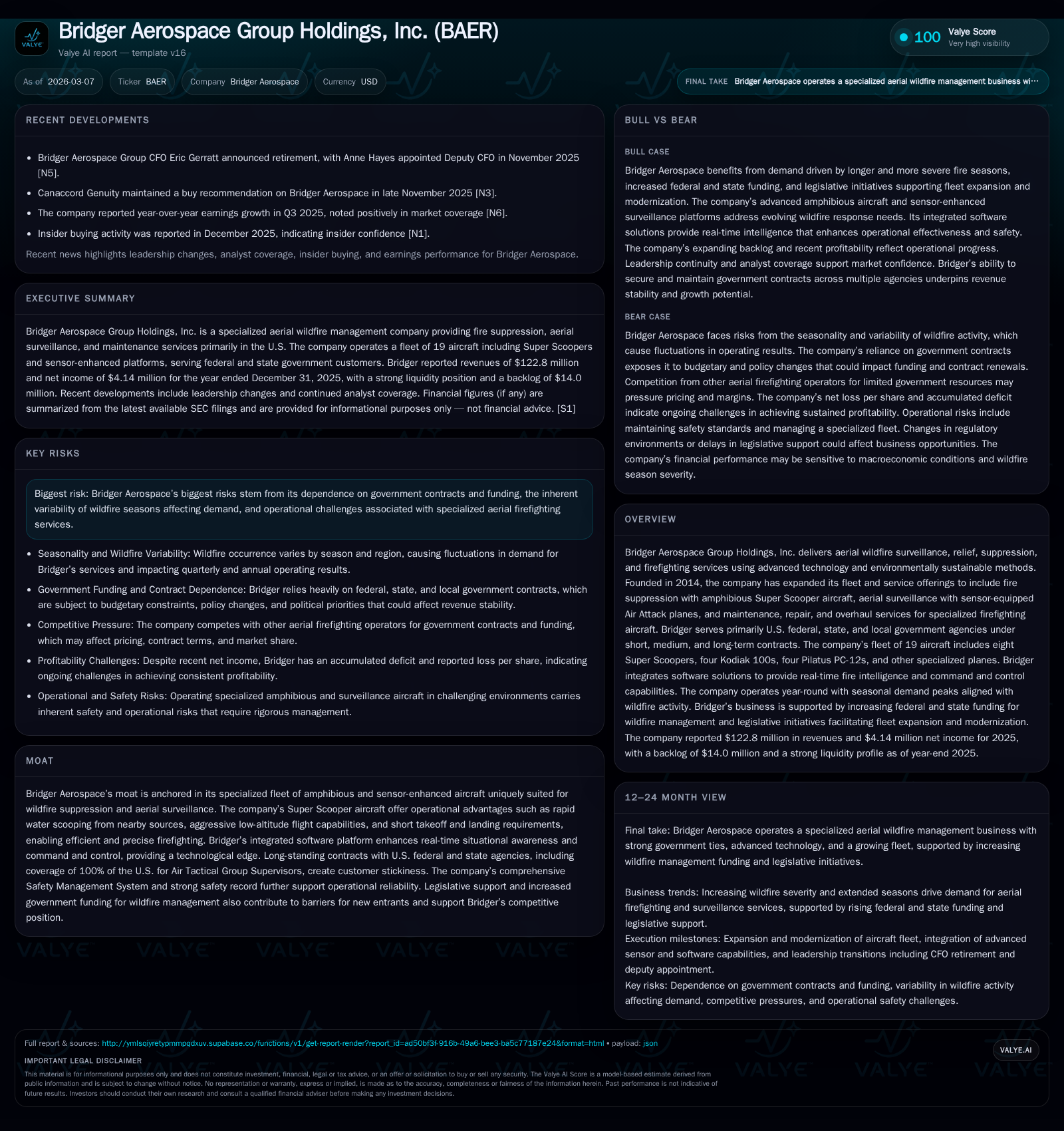

Bridger Aerospace Group Holdings, Inc. experienced a financial turnaround between 2023 and 2025, shifting from a net loss of $77.4 million in 2023 to a net income of $4.1 million in 2025. This recovery was driven by expanding its specialized amphibious firefighting fleet, increasing revenue by over 24%, and managing costs prudently despite rising maintenance expenses related to fleet scale-up. The company secured a comprehensive refinancing in late 2025 that enhanced liquidity and extended debt maturities, supporting aggressive capital expenditures that grew nearly nineteenfold in one year. Bridger operates under long-term government contracts but remains exposed to wildfire seasonality and funding variability. Key future metrics include leverage ratios under declining covenants and contract renewals amid fluctuating wildfire demands.

Transformation Behind the Turnaround: Historical Financial Milestones and Drivers

Bridger Aerospace’s recent financial arc illustrates a striking pivot from substantial losses to modest profitability within two years. The company reported a net loss of approximately -$77.4 million for fiscal year 2023 [F1], burdened by significant operating inefficiencies amid fleet expansion phases. By contrast, fiscal year 2025 closed with a positive net income of $4.14 million, representing a year-over-year (YoY) increase of roughly 127% compared with the prior year’s -$15.57 million loss [F1]. Operating income mirrored this trend, improving from $5.32 million in 2024 following losses in earlier periods [F1].

This performance recovery aligns with revenue growth from $98.6 million in 2024 to $122.8 million in 2025—a robust 24.5% increase—driven primarily by expanded fire suppression and aerial surveillance services [S4]. The company's operational costs rose as well; notably, maintenance expenses jumped significantly from approximately $26.46 million to $39.21 million, reflecting the scaling of the fleet and associated upkeep demands [S4]. Meanwhile, selling, general & administrative (SG&A) expenses remained relatively stable (+1.3%), highlighting controlled spending amidst growth initiatives [S4]. These dynamics underscore an improving revenue base partially offsetting rising variable costs.

Operating cash flow also turned positive after consecutive years of losses, reaching $16.7 million in 2025 versus $9.35 million in 2024, marking an improvement of nearly 79% YoY [F1]. This supports ongoing operations despite a sharp capex rise (discussed later). The clear shift into positive earnings territory marks managerial execution on strategic priorities post-CEO transition following Tim Sheehy’s Senate election.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 4 | 17 | 81 | +126.6% | |

| 2024 | -16 | 9 | 5 | 4 | +79.9% |

| 2023 | -77 | -27 | -57 | 21 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -64 | -1.2 |

| 2024 | 5 | 4.8 |

| 2023 | -48 | 23.6 |

Source: SEC companyfacts cache [F1].

Note: Operating income figure for FY2025 was not explicitly reported; comparison uses available prior years’ data [F1], [S4].

Deploying Technology and Specialized Aircraft: Core Operational Assets Fuel Growth

Bridger Aerospace’s strength lies in its niche yet scalable aerial firefighting capabilities incorporating technologically advanced amphibious aircraft alongside sensor-equipped surveillance platforms [S4]. Central to its competitive edge is the Super Scooper CL-415EAF fleet—eight amphibious aircraft capable of rapid water scooping directly from lakes or reservoirs near wildfires without lengthy turnaround times for refilling [S4]. This permits aggressive initial attack maneuvers at low altitudes with short takeoff/landing parameters critical during fast-evolving fire events.

Complementing suppression planes are four Kodiak 100s and four Pilatus PC-12s outfitted with sophisticated sensor suites facilitating real-time aerial reconnaissance—the so-called Air Attack role—which vastly improves situational awareness for firefighting command units [S4]. Bridger integrates these platforms with proprietary command-and-control software enabling live data feeds that inform resource allocation dynamically.

Fleet expansion since inception has been rapid; by end-2025 Bridger operated a total of nineteen aircraft including multiple international assets stationed temporarily abroad for operational assessment [S4]. Software integration enhances coordination among air tactical group supervisors throughout U.S. territories—an exclusive coverage lock that reinforces client stickiness particularly for federal agencies seeking seamless interagency collaboration.

The combination of specialized amphibious water scooping capabilities married with advanced electronics differentiates Bridger within the niche aerial firefighting sector where asset exclusivity acts as an entry barrier.

Navigating Wildfire Seasonality and Government Funding: Growth Prospects and Industry Constraints

Demand for Bridger’s firefighting assets fluctuates sharply with wildfire incidence—a factor tied closely to weather patterns such as drought periods altering both timing and intensity of fire seasons nationwide [S11]. Though the company operates year-round owing to regionally staggered wildfire cycles across North America, peak utilization occurs largely during summer months encompassing Q2 and Q3 [S11]. This seasonality injects inherent volatility into quarterly financial outcomes.

Furthermore, the company relies predominantly on U.S federal and state government contracts issued mainly via agencies like the U.S. Forest Service (USFS) and Department of Interior (DOI), covering all states most prone to wildfires [S4], [S11]. Contract lengths vary but often include auto-renewal clauses providing some revenue visibility; however industry risk arises from potential shifts in governmental funding priorities or regulatory changes impacting aerial firefighting budgets as noted under risk disclosures [S1].

Management continues targeting contract renewals while exploring service scope expansions that mitigate dependency concentration risk even though three customers accounted for over 85% total revenues in FY2025 [S5]. Overall legislative support around climate resilience potentially bodes well for gradual spending increases but demand remains exposed to unpredictable wildfire frequency fluctuations.

Liquidity Boost and Debt Refinancing: Unlocking Financial Flexibility for Expansion

A pivotal event solidifying Bridger’s financial footing was the October 28, 2025 refinancing exercise replacing its previous $160 million Series 2022 bonds with an enhanced Credit Agreement package [S1],[S6],[S7],[S10]. This new structure comprises:

- $210 million Initial Term Loans maturing October 2030

- A $21.5 million revolving credit facility (unused as of Dec '25)

- A $100 million Delayed Draw Term Loan (with $10.3 million drawn initially)

The transaction extended maturities meaningfully while consolidating multiple legacy obligations including Live Oak Bank credit facilities and UMB loan repayments totaling nearly $43 million principal retired simultaneously—the associated costs caused a recognized extinguishment loss near $7.8 million inclusive of write-offs on issuance fees [S1],[S6],[S7],[S9].

Interest rates are set at Term SOFR +6%, reflecting market risk pricing; first-priority liens secure most tangible/intangible assets notably aircraft collateral underpinning lender comfort [S6],[S7],[S10]. Covenant structures incorporate leverage limitations reducing from maximum ratios up to seven times initially down to targets near five and a half over subsequent years while setting minimum operating cash flow thresholds ($30M minimum) [S7],[S13],[S14].

This liquidity strengthening affords Bridger capacity to pursue aggressive capital investments coupled with manageable near-term debt service obligations—key given planned fleet modernization efforts discussed next.

Capital Investment Surge: Evaluating Asset Purchases and Impact on Cash Flow

Fiscal year 2025 witnessed an extraordinary jump in capital expenditures totaling approximately $80.9 million—nearly nineteen times greater than the previous year's $4.08 million outlay—signaling accelerated asset acquisition activities aligned with strategic growth objectives [F1], [S19],[S13].

A material portion funded by available credit lines post-refinancing includes acquisition of new aircraft such as two Pilatus planes purchased outright from previously leased assets ($10.3M draw on DDTL) plus large investments in Spanish CL-415EAF Scooper variants for European operations examination (~$50M purchase completed end-of-year), along with contracted King Air aircraft planned for early delivery in calendar year following reporting period valued at roughly $11.4 million as per recent agreements [S4].

While this investment surge has adversely impacted free cash flow which stood negative near -$64.2 million (operating cash flow minus capex) reflecting heavy reinvestment cycles typical within aerospace fleets’ renewal windows, strong operating cash flow improvements cushion funding needs temporarily during this growth phase (operating cash flow rose >78%) [F1].

Capital deployment emphasizes fleet modernization balanced against burning-season readiness; successful integration points toward upcoming periods where operational leveraging might provide margin expansion if revenue growth sustains pace.

Market Concentration and Contractual Relationships: Sustaining Customer Stickiness

Clients remain heavily concentrated among government entities with three largest customers combining for almost two-thirds of total revenues (66%, ~11%, ~10% respectively for FY2025) consistent with prior periods albeit slight additional dispersion compared against two dominant accounts holding nearly three quarters prior year share (61%, ~12%) [S4],[S5].

Such client concentration inherently raises counterparty risk exposure but is tempered by longstanding contractual engagements typically inclusive of auto-renewal options across federal/state wilderness agencies tasked with wildfire management oversight—a backbone underpinning backlog stability estimated at approximately $14 million as of December 31, 2025—although such backlog is subject to usual contract termination-for-convenience provisions limiting long-horizon revenue visibility somewhat [S16],[S25].

This tight customer base underscores necessity for continued excellence in service reliability including superior safety management systems recognized within industry standards supporting repeated renewals across multiple fire seasons.

Forecast Signals and Key Metrics to Monitor Going Forward

Absent explicit formal guidance or detailed multi-year forecasting within filings through early March ’26 ([N#] none found), investors should track several performance indicators likely indicative of Bridger’s trajectory:

- Compliance trends with evolving total leverage ratio covenants which relax gradually from current maximum levels near seven times consolidated debt/EBITDA toward approximately five and a half starting early-to-mid calendar years post-refinancing through maturity dates (2030 horizon) [S7],[S13]

- Quarterly operating cash flow relative to minimum thresholds ($30M per covenant) signaling ability to cover interest/principal alongside reinvestment needs

- Renewal status outcomes of major governmental contracts constituting >85% total revenues especially amid shifting federal budget priorities or wildfire policy adjustments

- Fire season intensity forecasts which correlate strongly with utilization rates affecting flying hours logged on Super Scoopers/Kodiaks/Pilatus platforms

- Margins improvement or contraction associated with scale effects invoked by larger fleet deployments sustaining cost control

- Announcements around fleet acquisitions like King Air deliveries or regional expansion signaling strategic diversification moves

Taken together these metrics will serve as forward-looking barometers letting stakeholders assess whether Bridger consolidates recent gains into sustainable growth or if external volatility reintroduces financial stress.

This analysis draws exclusively on publicly available SEC filings ([F1], [S#]) up through March ’26 filings paired with internal domain knowledge without speculative forecasts beyond noted evidence constraints. It represents neither investment recommendations nor price commentary but aims to elucidate Bridger Aerospace's operational evolution amid challenging industry fundamentals.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments