Cable One Bolsters Broadband Reach by Acquiring Full Stake in Mega Broadband Investments

Following strong Q1 results, Cable One aims to expand Vyve Broadband’s footprint through a pending $475–495 million acquisition, while managing regulatory and integration risks.

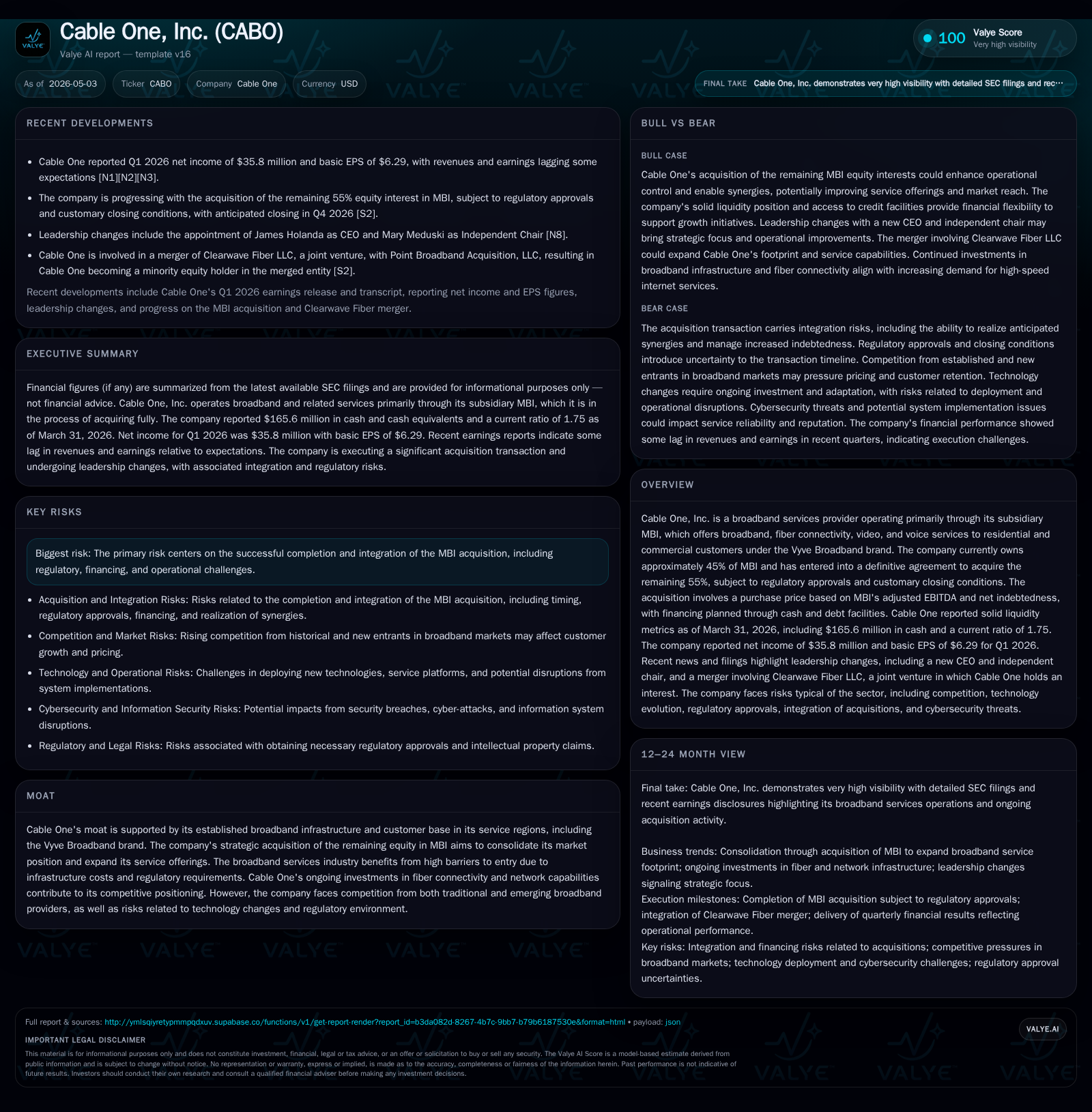

Cable One reported solid first-quarter 2026 results highlighted by $35.8 million net income and stable liquidity, reflecting ongoing strength in its broadband business. The company is on track to complete the acquisition of the remaining 55% stake in Mega Broadband Investments (MBI), consolidating its broadband footprint under the Vyve brand. This strategic move aims to enhance Cable One’s scale and service offerings amid persistent industry infrastructure barriers and competitive pressures. Execution risks related to acquisition integration, regulatory approvals, and financing remain key watchpoints.

Recent Operating Update: Q1 2026 Highlights

Cable One’s latest quarterly report for the period ending March 31, 2026 reveals a continuing trajectory of operational stability anchored in its broadband services segment. The company posted net income of $35.8 million with basic earnings per share of $6.29 [S2]. These metrics demonstrate underlying profitability amid ongoing investments in scaling its fiber infrastructure through its Vyve Broadband subsidiary.

Liquidity remains robust with cash and equivalents totaling approximately $165.6 million as of quarter-end alongside a current ratio of 1.75, signaling sound short-term financial health [F1]. This positions Cable One well to execute its planned strategic transactions without immediate liquidity constraints.

The most material near-term development is Cable One's progress towards fully acquiring Mega Broadband Investments (MBI), where it currently holds a 45% stake. The company entered into a definitive agreement on January 2, 2026 to acquire the remaining 55%, at an anticipated price range of $475 million to $495 million subject to standard regulatory approvals and customary closing conditions [S3, S19]. Regulatory consents from federal and state authorities are expected to be satisfied by mid-May 2026, paving the way for closing no earlier than October 1, 2026 [S3].

Business Model: Revenue Mechanics and Strategic Position

Cable One generates revenue primarily through broadband internet services offered to residential and commercial customers. Its subsidiary MBI operates under the Vyve Broadband brand providing a mix of broadband data, video entertainment packages, voice telephony services, and increasingly fiber-based connectivity solutions [S1].

Customers pay monthly subscription fees which vary based on speed tiers (e.g., gigabit-level fiber access commands premium pricing), bundled service products (data + video + voice), as well as installation or upgrade charges. Revenue growth derives from increasing subscriber counts (volume), periodic rate escalations (pricing), product upgrades migrating customers up bandwidth tiers (mix), and expansion into new geographic territories via acquisitions or network buildout.

Operationally, margins benefit from economies of scale inherent in network infrastructure usage; fixed costs are leveraged over growing subscriber bases while incremental bandwidth provisioning costs remain moderate when transitioning customers onto fiber networks.

The pending full ownership of MBI is a strategic lever intended to capture greater margin upside from unified operations while expanding Cable One’s addressable market footprint across regional broadband markets previously only partly served through JV ownership.

Industry Structure and Competitive Positioning

The U.S. broadband services industry features significant barriers to entry due to capital-intensive infrastructure requirements—network deployment involves substantial rights-of-way negotiations, regulatory franchising commitments, and upfront fiber optic cable installations often running millions per mile.

These hurdles insulate incumbents like Cable One but also necessitate continuous capital investment to upgrade legacy coaxial systems toward all-fiber networks demanded by growing consumer data traffic needs [S1]. The industry remains regulated at multiple levels with oversight on service quality standards, franchise renewals, pole attachment fees, and consumer protection rules affecting pricing power.

Competition spans traditional cable operators such as Comcast and Charter Communications who have nationwide scale vs. regional players like Cable One that often serve suburban or less densely populated areas with limited alternatives for consumers.

New entrants deploying fixed wireless access technologies or low-earth orbit satellite internet services pose emerging competitive threats in rural or underserved markets but face challenges matching fiber speeds sustainably.

Cable One's Vyve Broadband brand provides differentiation through localized customer service combined with investments in next-generation fiber capabilities supporting symmetrical upload/download speeds meeting enterprise clients’ increasing demands as well [S1].

Growth Drivers

The primary growth vector is subscriber base expansion fueled by tailoring multi-product bundles attracting both residential customers upgrading their internet plans for streaming/remote work use cases—and commercial clients needing robust connectivity for cloud applications.

Fiber network builds enable higher-tier offerings with stronger margins given customer willingness to pay for consistent gigabit-capable connections supporting evolving digital lifestyles and smart home technologies.

Cross-selling within acquired regions post-MBI acquisition offers synergies through unifying billing platforms and marketing channels improving customer retention rates.

Additionally, network modernization facilitates offering differentiated managed services or business-grade internet packages which command premium pricing relative to commoditized consumer plans.

Risks / Watchpoints / Growth Constraints

The foremost risk revolves around successfully completing the MBI acquisition without delays or escalated costs attributable to financing complications or regulatory pushback beyond expectations [S13]. Integration risks also bear watching—aligning operational systems across two corporate cultures carries execution uncertainty which could impair cost efficiencies or divert management attention [S26].

Technology shifts impose constant pressure; failure to keep pace updating networks to meet next-generation data demands could result in market share loss.

Industry competition intensity could intensify pricing stresses especially if emergent wireless or satellite alternatives gain footholds reducing incumbent pricing power.

Leverage levels post-transaction will spike materially given incremental debt incurred; maintaining prudent balance sheet discipline while funding organic/fiber expansion is imperative [F1].

Supply chain volatility for hardware components might delay critical network upgrades impacting customer experience metrics detrimental for retention.

What To Watch Next

Key near-term milestones include anticipated FCC and state regulatory approvals expiring May 12, 2026 enabling Cable One to proceed toward closing MBI acquisition by Q4 calendar year-end [S3]. Market reaction surrounding this timeframe will reveal investor confidence in deal execution.

Post-close integration effectiveness should become evident through operational metrics such as subscriber churn rates within former MBI territories alongside cost synergy realizations detailed gradually via quarterly disclosures.

Further announcements around fiber rollout acceleration plans or new product launches leveraging combined scale could signal continued strategic momentum.

On the financial front, tracking leverage ratios relative to cash flow generation during subsequent quarters will help assess balance sheet flexibility amidst capital allocation choices between debt servicing versus reinvestment.

Financial Snapshot (As of Q1 Ending March 31, 2026)

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $166mm | |

| 2026-03-31 | ||

| Total debt | $3.1bn | |

| 2026-03-31 | ||

| Net debt | $2.9bn | |

| 2026-03-31 | ||

| Current assets | $300mm | |

| 2026-03-31 | ||

| Current liabilities | $171mm | |

| 2026-03-31 | ||

| Current ratio | 1.75x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

The company exhibits strong liquid asset reserves but carries significant net debt mainly due to financing activities related to its acquisition strategy. Maintaining current ratio above unity reflects prudent working capital management despite capital intensity in infrastructure projects [F1].

This analysis leverages publicly available SEC filings as of April 30, 2026 ([S2], [S3], [S1]) combined with factual financial metrics drawn from current balance sheets ([F1]). It reflects the company's positioning within a structurally constrained yet evolving broadband industry shaped by scale economics and technology upgrades requiring disciplined execution against defined risks without extending into speculative valuation commentary.

Disclaimer: This report is provided for informational purposes only without any investment recommendation or endorsement regarding Cable One Inc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments