Interparfums Strengthens Brand Portfolio with License Extensions and Innovation Pipeline

Interparfums’ latest quarter underscores strategic license renewals and a robust innovation pipeline as pillars for sustainable growth despite market headwinds.

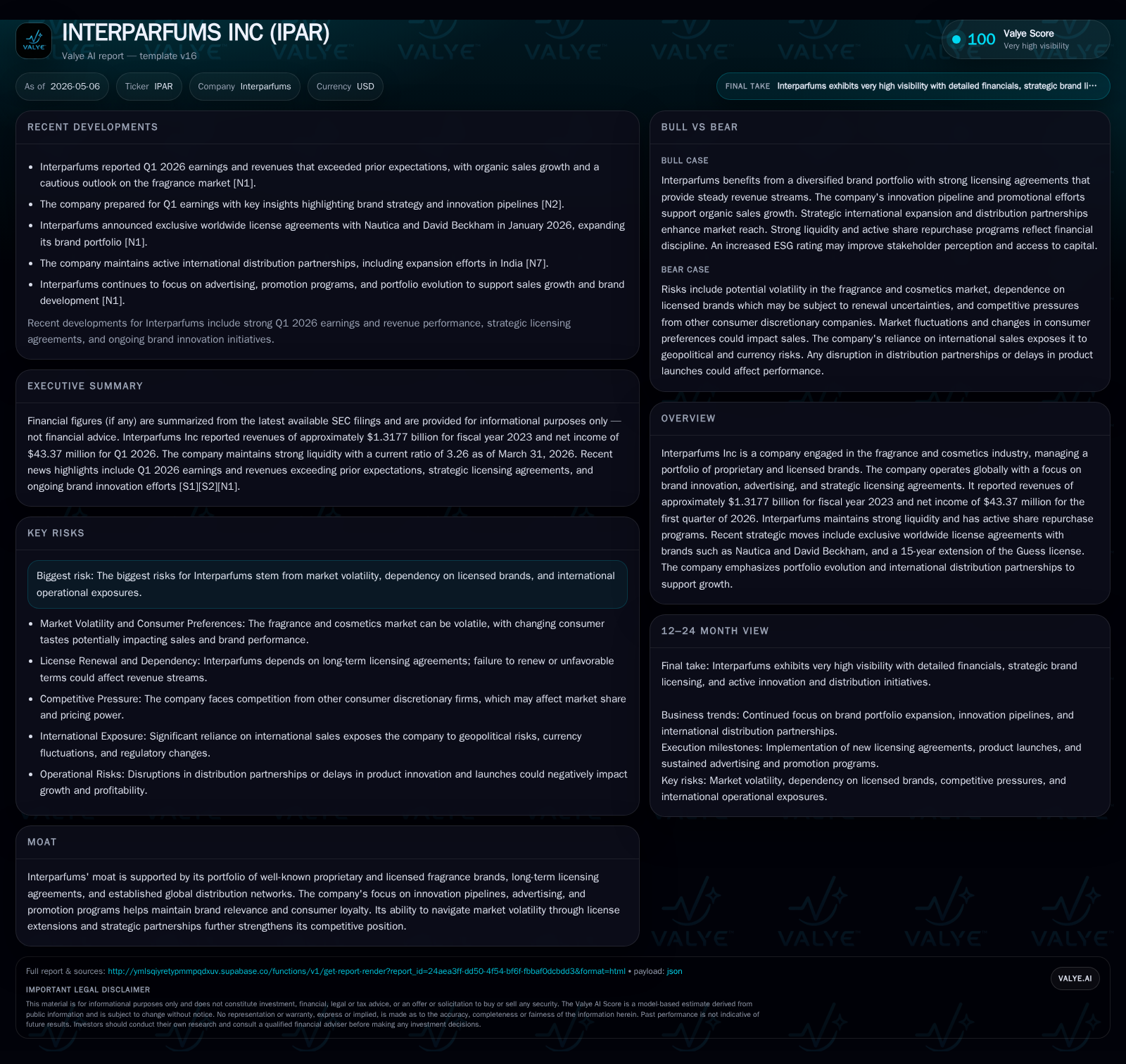

Interparfums reported modest revenue growth and net income improvement in Q1 2026, bolstered by continued licensing agreement extensions including a significant 15-year extension with Guess and new brand licenses such as Nautica. The company’s business model leverages proprietary and licensed brands with strong advertising support, maintaining competitive advantage through stable long-term contracts and global distribution reach. Growth is primarily driven by planned new product launches across key brands like Montblanc, Lacoste, and Donna Karan/DKNY, alongside international expansion efforts. Risks revolve around exposure to licensed brand renewal cycles and geopolitical uncertainties impacting operational costs. Financially, Interparfums maintains a solid liquidity position with disciplined share repurchases supporting shareholder value.

Q1 2026 Operating Update: Reassessing Momentum

Interparfums released its first-quarter results for fiscal year 2026 on May 5th (10-Q [S2], complemented by an 8-K update [S3]), reporting a modest but positive revenue increase of approximately 2% versus the prior year. Net income for the period was announced at $43.37 million—a sign that operational efficiencies and focused brand management are beginning to bear fruit even amid macroeconomic challenges [N6]. Advertising and promotional expenditures remained robust in Q1, signaling continued investment in brand equity maintenance and customer engagement critical in the fragrance sector where consumer preferences evolve rapidly [S3].

Notably, management authorized ongoing share repurchases early in the year with approximately 46,000 shares bought back at an average price of $85.56 during January alone, underlining confidence in the company's financial strength and future prospects despite cautious industry dynamics [S2]. These actions came alongside strategic licensing developments disclosed in the same filings: a pivotal 15-year extension of the Guess fragrance license underpinning long-term revenue visibility plus newly inked worldwide licenses for Nautica and David Beckham brands effective in coming years [S3][S29]. This combination of steady organic growth plus reinforcement of the licensing portfolio sets a tone of cautious optimism.

Refining the Business Model: Licensing, Branding, and Product Excellence

Interparfums operates primarily as a fragrance house that profits through a hybrid business model involving both proprietary brands under its control and an array of licensed luxury fragrance lines. Revenue generation is largely tied to royalties and licensing fees paid by retail partners who distribute these fragrances globally; these contracts frequently span multiple years or decades—as exemplified by the extended Guess license—ensuring recurring income streams while reducing volatility associated with short product life cycles [S1][S3].

The company differentiates itself by investing heavily in a pipeline of innovative scent profiles and complementary product extensions to keep its brands relevant in saturated markets. Effective brand management requires consistently refreshed offerings combined with targeted marketing campaigns to sustain consumer loyalty—a key switching cost embedded deep within fragrance purchases where emotional attachment often drives repeat buying behavior [N8]. Interparfums’ approach also involves leveraging its distribution network to scale launches internationally and exploit emerging demand pockets in Asia-Pacific and other developing regions.

Competitive Positioning Within the Fragrance Industry

The competitive moat Anchoring Interparfums’ stable performance lies within its portfolio's breadth—including high-recognition brands like Montblanc, Lacoste, and David Beckham—secured via often exclusive long-term licensing agreements that few peers can readily replicate. This scale affords economies in production planning, advertising leverage, and favorable terms with retail distributors globally [S1][N8]. The diversity across price points from luxury to more accessible segments also helps cushion against localized demand disruptions.

Industry structure is fragmented but dominated by players controlling flagship licenses due to barriers posed by brand equity management expertise and access to celebrity or designer partnerships. Pricing power varies widely but typically follows brand recognition curves; Interparfums sustains margins partly through disciplined promotional spend ensuring brand premium is preserved while combating intensified competition from niche or indie fragrance startups.

Growth Drivers: Innovation Pipelines and Global Partnerships

Looking forward into late 2026–2028 horizon detailed in recent disclosures ([S7], [S8]), Interparfums signals multiple catalysts underpinning growth expectations. Foremost among them are scheduled launches for Montblanc’s next-generation fragrances set for H2 2026 alongside new product introductions for Lacoste expanding geographic footprint plus Donna Karan / DKNY lines freshening their appeal through formulation upgrades.

Complementing these rollouts are international expansion strategies targeting emerging markets that remain underpenetrated relative to developed countries—especially within Asia-Pacific where premiumization trends continue driving discretionary spending on personal care goods. Advertising expenditure remains an integral lever here; consistent investment supports building awareness critical in newer territories while defending core markets against competitor incursions [N8][N6].

Key measurable indicators discussed by management include timing adherence for launches, incremental sales contributions expected per brand roll-out phases materially confirmed during earnings calls ([N2]), as well as retention rates for renewing licenses securing stable percentage fees over time.

Risks and Constraints: Market Volatility and Licensed Brand Dependence

Despite strengths, significant risks warrant attention. The annual report’s risk disclosure ([S1], [S28]) highlights market volatility driven by fluctuating consumer sentiment on luxury discretionary spends exacerbated by geopolitical events—the ongoing war-related tensions in the Middle East also introduce logistical challenges affecting supply chains or distribution costs ([S8]).

A structural vulnerability resides in reliance on licensed brand agreements; although recent extensions (Guess) reinforce stability, contractual renewals inherently introduce uncertainty about future cash flows should licensors opt not to extend or alter terms unfavorably.

Additional headwinds stem from currency fluctuations impacting international margins as well as tariffs that may be imposed intermittently affecting cost structures — both factors that may compress operating profitability if not managed prudently ([S8]). The company’s emphasis on prudent capital management attempts to mitigate those risks but demands continued vigilance.

Key Upcoming Milestones and Forward-Looking Indicators

Industry watchers should track several near-term markers: succeeding quarterly earnings releases to gauge consistency versus guidance reaffirmed through May filings ([S7]); progress on new product launches especially scheduled for Montblanc (H2 2026) which serve as volumetric KPIs; any fresh announcements regarding licensing arrangements which could alter revenue outlooks; plus updates from investor conference calls providing tone on mid-year strategy recalibrations ([N2]).

External market metrics such as premium fragrance consumption growth rates globally will also provide relevant demand context influencing underlying sales trajectories.

Financial Overview: Balance Sheet Health and Capital Allocation

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Total debt | $176mm | |

| 2025-12-31 | ||

| Net debt | $96mm | |

| 2025-12-31 | ||

| Current assets | $998mm | |

| 2026-03-31 | ||

| Current liabilities | $306mm | |

| 2026-03-31 | ||

| Current ratio | 3.26x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

A snapshot of Interparfums’ balance sheet as of March 31, 2026 shows a current ratio of 3.26, indicating strong short-term liquidity. Total debt stood at approximately $176 million with net debt near $96 million as of December 31, 2025, reflecting a manageable leverage profile relative to the company’s revenue base ([F1]).

Active share repurchase programs signal corporate confidence whilst balancing capital deployment toward innovation investments critical for sustaining franchise value.

This analysis integrates recent quarterly disclosures with annual strategic context illustrating how Interparfums leverages its deep-rooted business model revolving around long-duration licenses and continuous innovation amid nuanced global macroeconomic conditions. While opportunities arising from product pipeline expansions and geographic penetration appear promising drivers for future performance gains, vigilant management of external risks remains paramount for preserving margin integrity going forward.

Disclaimer: This report is an informational analysis based solely on public SEC filings and reputable news sources as indicated; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments