Lifecore Biomedical Reaffirms Growth on Contract Manufacturing Backbone

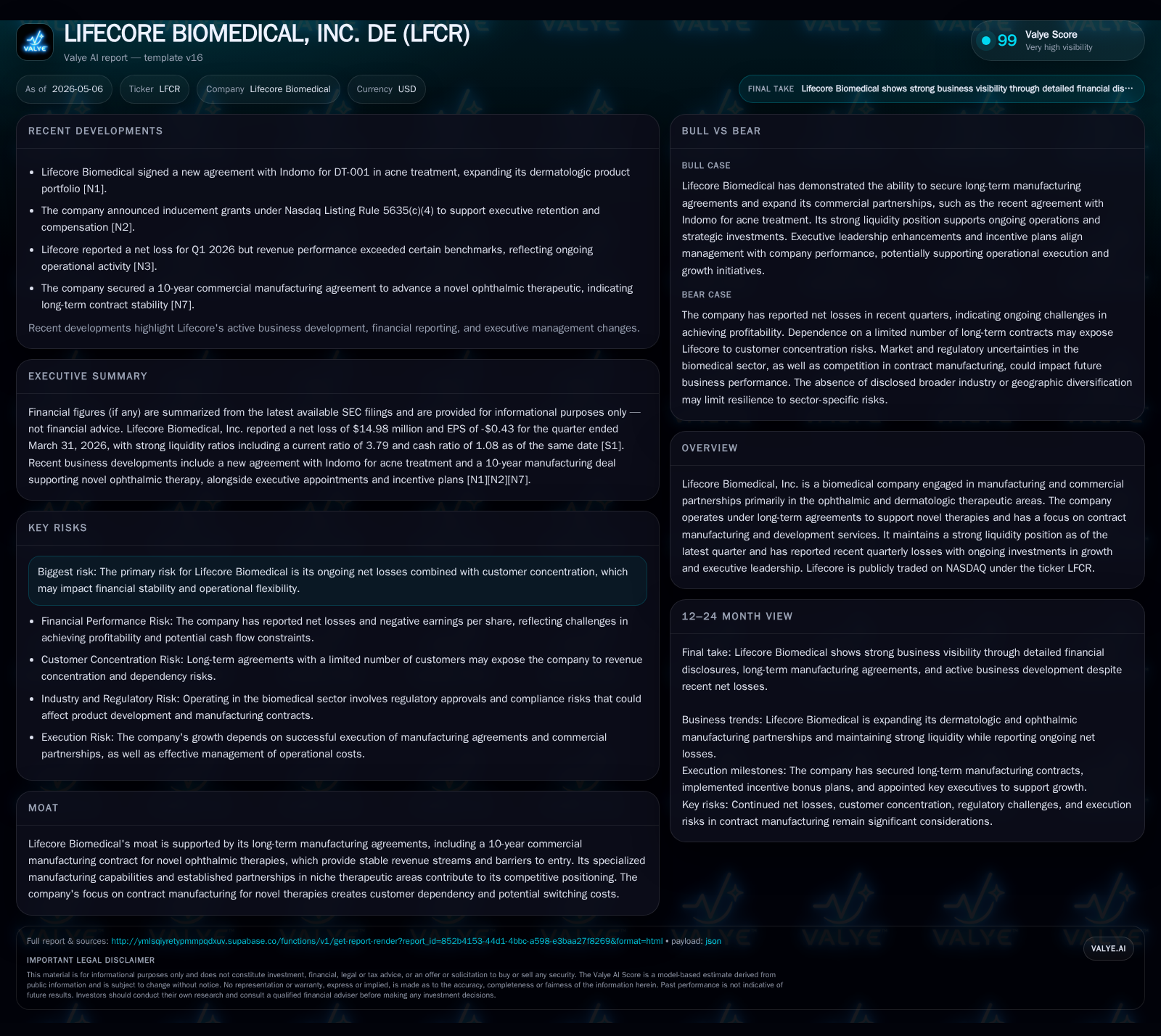

Lifecore’s Q1 2026 results underscore revenue stability from long-term manufacturing agreements despite ongoing net losses driven by strategic investments.

In its latest quarterly filing, Lifecore Biomedical demonstrates operational resilience anchored by long-term contract manufacturing agreements in ophthalmic and dermatologic therapeutics. The company reported continued net losses reflecting deliberate investments in growth and executive leadership without material changes in risk profile. Its specialized manufacturing capabilities and decade-long commercial contracts underpin a stable revenue base, positioning Lifecore for expansion while balancing customer concentration and leverage risks.

Latest Quarterly Operating Update: Stability Meets Investment

Lifecore Biomedical’s first quarter ending March 31, 2026, reflects its established role as a specialized contract manufacturer with stable revenues anchored in long-term commercial agreements. According to the May 6, 2026 Form 10-Q [S2], the company continues to operate primarily under multi-year contracts—most prominently a 10-year commercial manufacturing agreement focused on novel ophthalmic therapies. This foundational stability offsets the pressures of ongoing investment-driven operating losses reported in the quarter. There were no material changes to previously disclosed risk factors [S2], underscoring continuity in the company’s risk profile.

Liquidity remains solid with cash and equivalents totaling roughly $20.8 million alongside a strong current ratio of 3.79 supported by $77.6 million in current assets against $20.5 million current liabilities [F1]. This provides Lifecore with near-term financial flexibility amid its investment phase. However, total debt stands elevated at about $200 million with net debt approximating $179 million after accounting for cash [F1], which frames capital structure considerations.

Business Model Foundations: Specialized Contract Manufacturing

Lifecore Biomedical operates as a contract development and manufacturing organization (CDMO) specializing in producing therapeutic products for ophthalmic and dermatologic applications under strict quality regimes compliant with cGMP requirements. Revenues derive primarily from long-term service contracts where pharmaceutical clients outsource manufacturing complexities that demand technical precision.

The company's value proposition lies in its capacity to deliver consistent quality amid stringent regulatory environments combined with flexible development-to-commercial scale-up capabilities. These qualities generate substantial switching costs for customers due to regulatory re-validation processes that create dependency on Lifecore's facilities and processes. Such differentiation limits commoditization risk prevalent among broader CDMOs.

Revenues are driven by contracted volumes and pricing structures that reward duration and technical complexity rather than simple unit turnover. Lifecore’s niche focus leverages accumulated expertise making it an indispensable partner for customers launching novel therapies in sensitive therapeutic segments.

Competitive Landscape and Industry Positioning

Within the biomanufacturing ecosystem serving ophthalmology and dermatology sectors, Lifecore commands competitive advantages rooted in exclusivity and technological barriers to entry. The company’s moat is reinforced by its long-term contractual relationships (including the critical decade-spanning ophthalmic manufacturing agreement) which secure predictable revenue streams and erect barriers against competitor incursions.

On competition, Lifecore faces pressure from other CMOs offering broader or lower-cost services but often lacking comparable specialized capabilities or regulatory certifications critical for these end markets. Execution quality—including consistency of batch release, compliance track record, and responsiveness—serves as critical differentiation fostering customer retention.

Pricing power appears moderate; given the niche nature of their services paired with regulatory hurdles for customers switching providers, Lifecore can maintain favorable pricing though mindful of pressure points from alternative manufacturers looking to encroach on their share.

Growth Drivers: Long-Term Agreements and Expanding Capabilities

Key growth levers emerge visibly from Lifecore’s ability to leverage existing contracts through volume escalations as client therapies scale post-approval [S7]. Capacity utilization improvements within existing facilities can materially enhance margins without proportional capital expenditure increases.

Moreover, pipeline expansion may derive from onboarding new customers or extending geographic reach of services—efforts supported by recent executive leadership investments signaling strategic emphasis on broadening operational scope. Although explicit new contract wins have not been detailed recently, the company’s commitment to innovation around manufacturing processes positions it well to pursue such growth avenues.

Performance incentives tied both to company-wide revenue attainment and adjusted EBITDA underpin management’s execution focus [S22], aligning internal priorities to measurable financial outcomes that support sustainability.

Risks and Constraints: Losses, Customer Concentration, and Debt

Despite steady revenue baselines, Lifecore continues to report net losses largely reflecting upfront costs linked to scaling operations and enhancing organizational depth [S2]. Sustained negative earnings limit internal cash flow generation necessitating reliance on existing liquidity buffers or external financing options.

Customer concentration remains a salient operational risk—revenue dependency on a limited number of contracts exposes Lifecore to potential volatility if contract renewals falter or if client demand slows unexpectedly. This concentration also constrains negotiating leverage.

Furthermore, balance-sheet leverage poses constraints; with net debt exceeding $179 million against relatively modest cash reserves [F1], refinancing risk or restrictive covenants could complicate growth funding or operational flexibility during downturns.

What to Watch Next: Milestones, Revenue Expansion, and Margin Progression

Upcoming quarters will be pivotal as Lifecore seeks evidence of volume ramps under existing agreements converting into improved top-line results alongside stable or improving gross margin profiles. Investors should track contract renewal announcements or extensions—as indicators of backlogged revenue—and management commentary on capacity utilization enhancements during earnings calls or filings [S3].

Additionally, developments related to customer diversification would mitigate concentration risks while any disclosed progress on new market entries would validate the firm’s strategic expansion ambitions.

Financial metrics tied closely to adjusted EBITDA performance targets will serve as barometers for operational scaling success given their weighting in executive compensation schemes [S22]. Monitoring these will provide insight into efficiency gains relative to costs associated with ongoing investment phases.

Financial Snapshot: Liquidity, Leverage, and Operating Results

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $21mm | |

| 2026-03-31 | ||

| Total debt | $200mm | |

| 2026-03-31 | ||

| Net debt | $179mm | |

| 2026-03-31 | ||

| Current assets | $78mm | |

| 2026-03-31 | ||

| Current liabilities | $20mm | |

| 2026-03-31 | ||

| Current ratio | 3.79x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

This financial data encapsulates Lifecore’s position at the quarter-end mark: robust short-term liquidity supports operations while indebtedness levels underscore fiscal discipline requirements over the longer term [F1]. Operating income remains pressured given strategic investments reflected in recently reported quarterly losses [S2], reinforcing that patience may be necessary before profitability inflection.

This analysis synthesizes recently reported operating dynamics within Lifecore Biomedical without offering investment advice. It reflects information as filed through May 6, 2026 [S2], [S3], supplemented by current balance-sheet evidence [F1] and contextualized industry insights specific to contract biopharmaceutical manufacturing segments.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments