Caleres Inc’s Revenue Growth Masks Mounting Profitability Pressure

The company’s flat revenue growth conceals a steep decline in earnings and liquidity challenges amid competitive footwear retail dynamics.

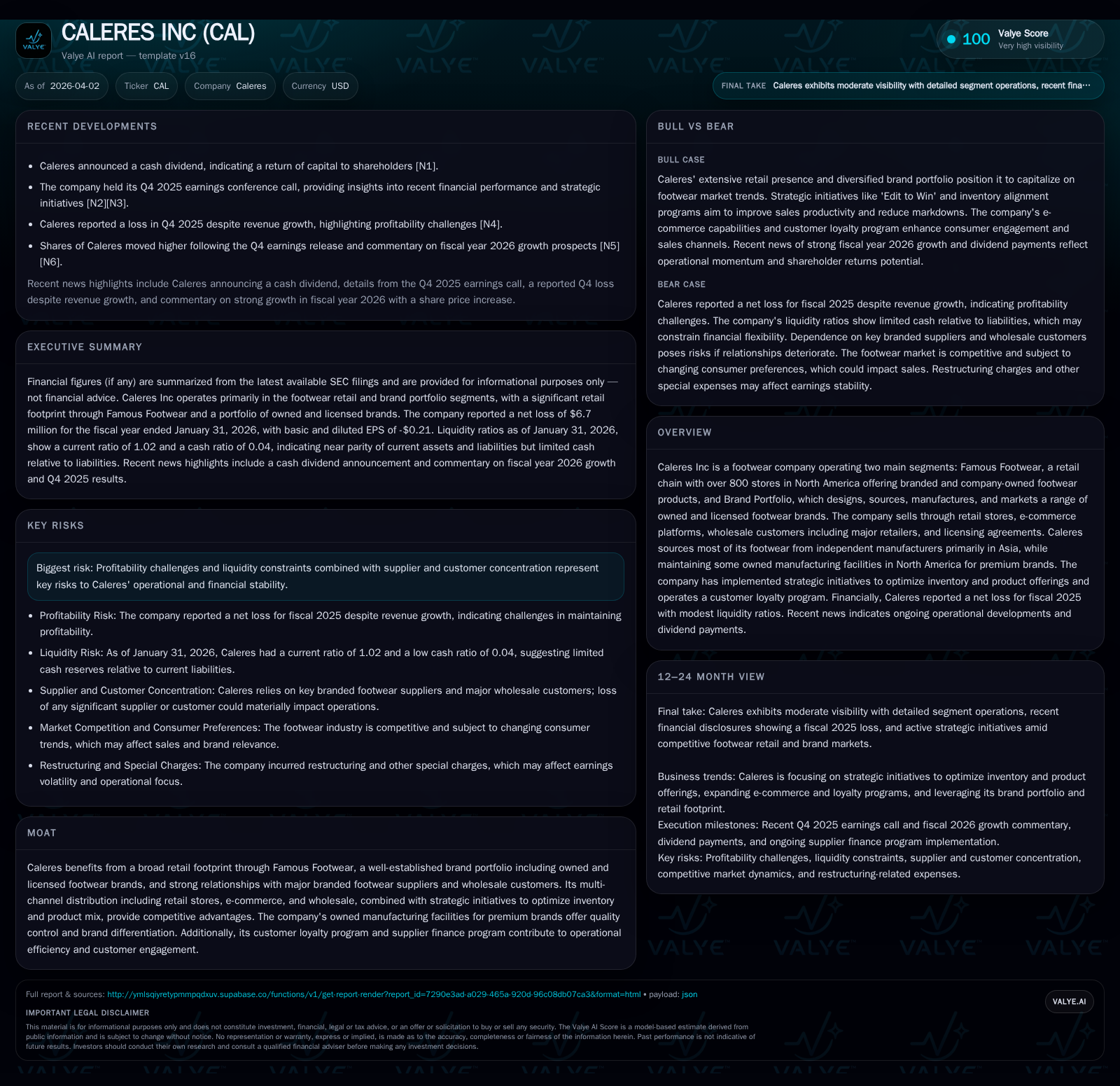

Caleres Inc reported nearly flat annual top-line growth of 0.5% in fiscal 2025, driven by its extensive Famous Footwear retail chain and diverse Brand Portfolio. However, operating income plunged roughly 95.7%, culminating in a net loss for the year amid margin compression and cost pressures. Liquidity remains tight with a current ratio near 1.02, while capital allocation reflects steady dividends but significantly scaled-back share repurchases. The company’s future growth hinges on strategic initiatives focused on premiumization and inventory efficiency, though profitability and working capital management remain key risk areas to monitor.

Revenue Momentum in 2025: Growth Drivers Behind a Flat Top Line

Caleres Inc showed resilience in sustaining revenue levels during fiscal 2025, reporting approximately $85.5 million in sales—a marginal increase of about 0.5% compared to the prior year [F1]. This flat performance belies a nuanced set of underlying dynamics within its dual-segment structure defined by Famous Footwear's expansive retail footprint across over 800 stores in North America and a Brand Portfolio comprising both owned and licensed footwear brands [S1][S23].

Famous Footwear continues to leverage its broad reach and brand recognition to maintain stable revenues despite pressure on store traffic trends common in brick-and-mortar retail. Concurrently, the Brand Portfolio segment complements with wholesale sales to major retailers such as Amazon.com, Nordstrom.com, TJX Corporation chains like Marshalls and TJ Maxx, Walmart, alongside direct-to-consumer e-commerce platforms [S15]. Licensing agreements contribute about 14% of Brand Portfolio sales [S23], enhancing product variety without significant capital expenditure.

Strategic initiatives including 'Edit to Win,' focusing on SKU rationalization to drive volume through fewer products, alongside a 'Speed' program aimed at synchronizing inventory closer with consumer demand cycles, helped mitigate markdowns and reduce inventory risks [S15]. These moves are vital given Caleres' reliance on independent Asian manufacturers for most footwear sourcing while maintaining some premium manufacturing facilities domestically [S1]. Nonetheless, overall revenue stagnation underscores market saturation pressures and intensifying competition.

Profitability Under Strain: What Sank Operating Income and Net Earnings

Despite the stable top line, Caleres endured severe profitability headwinds in FY2025 that culminated in operating income dropping nearly 95.7% to just $6.4 million—a collapse from $149.9 million seen the previous year [F1]. This translated into a net loss of $6.7 million marking a sharp reversal from net income of $107.3 million in FY2024 [F1].

The erosion stems from several intertwined factors: sustained SG&A inflation that outpaced gross margin gains; restructuring charges likely related to optimizing the retail footprint or brand portfolio consolidation; and adverse product mix effects where sales shifted toward lower-margin or promotional items dampening unit economics [S1][S14][N4]. Furthermore, pervasive margin compression reflects broader retail apparel sector dynamics where competitive pricing pressures constrain leverage.

The Brand Portfolio contends with wholesale channel margin dilution due to landed cost variability and longer supply chains emphasizing first-cost wholesale over higher-margin landed wholesale sales—a distinction crucial for pricing power [S14]. Additionally, operating losses highlight the challenge of balancing premiumization aspirations of owned brands against discount-driven volume elsewhere.

Retail Channels and Brand Portfolio: Multi-Channel Complexity Explored

Caleres operates through two principal segments which exhibit complementary strengths but also elevate execution complexity [S15]:

- Famous Footwear: Operating more than 800 stores primarily throughout North America offering well-known branded footwear alongside company-owned choices.

- Brand Portfolio: Encompasses design, sourcing (largely outsourced Asia), marketing of both owned/licensed branded footwear as well as direct-to-consumer online channels.

This multi-channel set-up allows diversified reach yet imposes intricate inventory management demands across physical stores, e-commerce sites, wholesale partners (e.g., Nordstrom Rack), plus licensing agreements generating royalties [S23]. Supply chain concentration risks arise due to reliance on Asian-based independent manufacturers coupled with smaller North American facilities reserved for premium brands like Allen Edmonds or Stuart Weitzman [S1][S15].

Another operational nuance is the recently implemented supplier finance program enabling select vendors to sell receivables facilitated by Caleres’ credit standing—this improves vendor relations but also defers cash outflows creating working capital intricacies [S5]. Meanwhile inventory turns vary markedly by channel; retail typically has slower turns compared with wholesale drop-ship models increasingly favored by large retailers.

Liquidity and Capital Structure: Navigating Tight Current Ratios and Debt

Liquidity metrics signal constraints within Caleres’ financial positioning. As of January 31, 2026, current assets marginally exceed current liabilities yielding an approximate current ratio of 1.02—reflective of a narrowly balanced working capital structure [F1][S6]. Cash & equivalents stood at about $29.8 million while revolving credit facility borrowings fluctuated substantially during FY25 reaching highs around $387 million during quarters before payments reduced outstanding balances [S4][S6].

Trade payables oscillated around higher levels characteristic of supplier concentration exposure compounded by the supplier finance arrangements where accounts payable represent confirmed obligations under financing terms [S10]. Lease obligations remain material given the large retail footprint with noncurrent lease commitments surpassing short-term amounts adding financial leverage risk [S4][S16].

These conditions constrict operational flexibility especially if market headwinds persist or unforeseen cash needs emerge.

Capital Allocation: Dividends Amid Declining Buyback Activity

Despite posting losses for FY2025, Caleres proceeded with dividend payments totaling approximately $9.4 million maintaining consistency albeit marginally below prior year distributions ($9.7 million) [F1][N1][S7]. This reflects management’s intent to preserve shareholder yield even while confronted with profitability pressures.

Conversely, share repurchases contracted drastically from $65 million in FY2024 down to just over $5 million in FY2025 highlighting prudence in discretionary cash deployment amid uncertain earnings [F1]. The resulting approximate return on equity stands negative near -1.1%, underscoring diminished capacity to generate shareholder wealth during tough operating periods.

This shift suggests prioritizing liquidity stabilization over aggressive capital returns—a signal aligning with constrained working capital conditions.

Historical Performance Summary

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -7 | 103 | 6 | 64 | -106.2% |

| 2024 | 107 | 105 | 150 | 49 | -37.4% |

| 2023 | 171 | 200 | 194 | 45 | -5.7% |

| 2022 | 182 | 126 | 214 | 56 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 9 | 5 | 39 |

| 2024 | 10 | 65 | 55 |

| 2023 | 10 | 17 | 156 |

| 2022 | 10 | 63 | 70 |

Source: SEC companyfacts cache [F1].

Future Growth Outlook: Strategic Initiatives and Market Positioning

Forward-looking commentary from recent earnings discussions anticipates continued top-line growth momentum into FY26 supported by ongoing premiumization trends prevalent across the footwear sector leveraging shifts towards higher quality brands commanding better margins [N2][N9][N12]. Caleres intends to capitalize on these dynamics through enhanced product mix optimization targeting elevated SKU productivity ('Edit to Win') alongside accelerated inventory responsiveness ('Speed' program) aimed at mitigating markdowns and obsolescence.

Management acknowledges external cost pressures remain a hurdle including labor inflation within SG&A functions plus supply chain disruptions potentially disrupting unit economics further if unchecked ([N2][N9]). The vast brand portfolio offers breadth but requires deft stewardship balancing scale efficiencies against brand dilution risk especially given licensing coverage comprising a notable revenue slice.

Execution of channel expansion efforts via e-commerce will be critical given shifting consumer behaviors favoring online shopping channels combined with digital loyalty engagement strategies boosting direct customer relationships ([N12]).

What to Watch: Key Metrics, Earnings Calls, and Dividend Developments

Professional investors should monitor several pivotal indicators during upcoming quarterly earnings releases:

- Revenue trajectory versus margin recovery signals distinguishing between mere volume gains versus profitable growth.

- Cash flow generation patterns especially free cash flow which remained positive (~$39 million) but impacted by elevated capex spending nearing $64 million for store refurbishments or technology investments [F1].

- Performance of the supplier finance program influencing accounts payable dynamics and downstream vendor reliability.

- Dividend announcements verifying sustainability amid ongoing net loss environment coupled with prudent share repurchase activity gauge market confidence levels.

Recent stock movements (+9.7% jump post-FY25 earnings) evidence market optimism contingent upon effective execution of premiumization strategy whilst keeping liquidity intact ([N8]). Close attention should be paid to any shifts in liquidity measures or unexpected expense items signaling operational stress escalation.

Disclaimer: This analysis is based solely on disclosed SEC filings and published news transcripts up to April 2nd, 2026. It reflects historical data without projecting investment outcomes or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments