CalciMedica’s Path to Commercialization: Evaluating Clinical Progress and Financial Resilience

An examination of CalciMedica’s innovative CRAC channel inhibitors against the backdrop of persistent clinical and financial challenges.

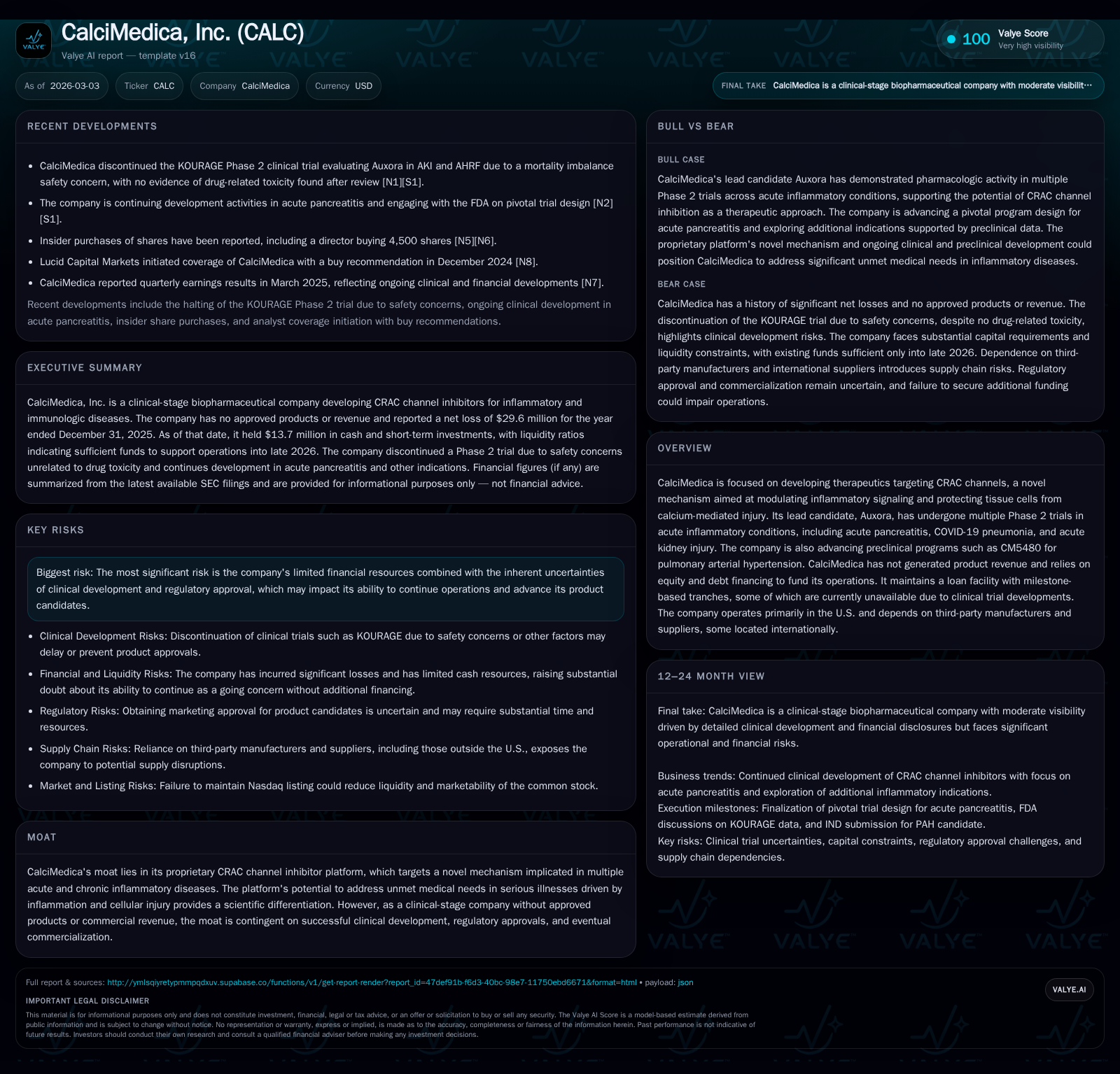

CalciMedica, a clinical-stage biopharma company pioneering therapeutics targeting calcium release-activated calcium (CRAC) channels, has demonstrated a scientifically differentiated platform with Auxora leading multiple Phase 2 trials for inflammatory diseases. Despite its technological promise, the company continues to grapple with significant net losses and cash burn fueled by ongoing clinical development costs. Its capital structure, reliant on milestone-based debt tranches and equity offerings, underscores funding constraints that interplay tightly with clinical progress. Upcoming Phase 3 milestones and financing events warrant close attention to gauge sustainability on its path toward potential commercialization.

Clinical Milestones Driving Past Performance

CalciMedica’s development trajectory is anchored by its lead asset Auxora, a selective CRAC channel inhibitor focused on modulating inflammatory signaling pathways detrimental in acute organ injuries. The company's clinical portfolio has matured around Phase 2 trials addressing critical unmet needs including acute pancreatitis (AP), COVID-19 pneumonia with acute respiratory distress syndrome (ARDS), and acute kidney injury (AKI) often complicated by acute hypoxic respiratory failure (AHRF).

The subsidiary nuances within these trials—such as patient enrollment curves, pharmacodynamic biomarker validations, and bridging data from inflammatory cascade modulation—have impacted timelines and trial outcomes [F1][S2]. For instance, the recent completion of the AP Phase 2b trial informs a planned pivotal Phase 3 program expected to test Auxora's efficacy in mitigating systemic inflammatory response syndrome (SIRS) alongside pancreatic inflammation [N2]. Concurrently, earlier Phase 2 COVID-19 pneumonia data demonstrated promising safety and efficacy signals albeit within limited cohorts [S2].

Separately, CalciMedica continues an ongoing Phase 2 AKI trial incorporating pediatric populations afflicted by asparaginase-induced pancreatitis, reflecting strategic breadth in patient targeting [S2]. These staged developments dictate R&D spend focus and inform subsequent clinical phase gating decisions.

Evolving Trial Outcomes: Impact on Financial and Operational Trajectory

Operationally, the company’s financial health remains tightly coupled with clinical trial progress. The decision to halt the KOURAGE study—a Phase 2 trial investigating Auxora’s efficacy in COVID-19-associated ARDS—was consequential enough to restrict access to milestone-triggered lending tranches under its existing loan agreements [N1][S13][S17]. The impact reveals how adaptive clinical decisions modulate financing runway dynamics.

Despite an approximate 4.5% improvement in operating income YoY from -$24.2 million in FY2024 to -$23.1 million in FY2025 [F1], net losses widened sharply by over 115% to -$29.6 million in FY2025 given other non-operational charges [F1][S1]. This deterioration illustrates exacerbated bottom-line pressures occasioned possibly by fair value adjustments or litigation reserves described in disclosures [S28]. Cash burn remains aggressive with operating cash flow stable but negative near -$21.18 million year-over-year [F1]. These trends signal persistent expense commitment towards advancing clinical programs even amid constrained resources.

Upcoming Catalysts: What Investors Should Monitor

The market should closely watch signals around initiation and enrollment into Phase 3 pivotal trials leveraging prior Auxora data sets from AP indications [N2][S3]. Regulatory feedback loops anticipated from FDA dialogue points present significant inflection potential. Additionally, execution of milestones triggering further debt tranche availability under the Avenue Venture loan agreement will be critical; delays or failures may compress liquidity further.

Parallel attention is warranted on external capital raising endeavors including secondary equity offerings or ATM sales given historical precedents tied to financing rounds witnessed through late 2024 and early 2025 [S17]. These will collectively dictate CalciMedica’s capital runway length allowing continued product candidate advancement.

Capital Structure Overview and Funding Dynamics

CalciMedica’s capital landscape at December 31, 2025 showed total debt of approximately $9.7 million complemented by $5.5 million raised through an ATM equity facility [F1][S17][S28]. The cornerstone financing instrument is a loan agreement with Avenue Venture Opportunities Fund entailing an initial $10 million drawdown followed by conditional access up to $22.5 million in milestone-based tranches contingent upon clinical progress metrics between September 2025 and March 2026 [S13][S18]. However, some future tranches remain unavailable owing to unmet milestones following recent trial developments [N1][S13].

Financial covenants impose restrictions around indebtedness incurrence, asset sales, dividend payments (prohibited), and other operational flexibilities reflective of typical venture debt facilities’ conservatism [S13][S28]. Month-to-month lease arrangements for reduced office space highlight cost rationalization adapting to financing limitations [S1][S6].

Evaluating Operating Losses, Cash Flows, and Capital Allocation

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -30 | -21 | -23 | 28000 | -115.8% |

| 2024 | -14 | -21 | -24 | 8000 | +60.1% |

| 2023 | -34 | -26 | -38 | 78000 | +3.5% |

| 2022 | -36 | -23 | -36 | 308000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -21 | 445.1 |

| 2024 | -21 | -95.1 |

| 2023 | -26 | -421.2 |

| 2022 | -23 | -99.0 |

Source: SEC companyfacts cache [F1].

CalciMedica shows a subtle amelioration in operating income losses from FY2024 to FY2025 but net income shrank due partly to non-cash accounting impacts per filings [F1][S28]. Capital expenditures remain negligible relative to cash outflows given focus on outsourcing manufacturing rather than fixed asset growth [F1]. No dividends or share repurchases have been reported—a standard stance for companies entrenched in phase gating research activities absent commercial product revenue.

ROE is profoundly negative given net losses outweigh shareholders' equity which turned negative at year-end 2025 due to accumulated deficits eroding book value calculated at approximately -445% based on latest figures [F1]. This reflects inherent risk profiles typical among early-stage biopharma players dependent exclusively on external capital injections.

Risk Management in a Resource-Constrained Environment

The company candidly outlines risks including dependency on successful clinical development outcomes required to unlock financing tranches under its loan facility combined with ongoing litigation risk from shareholder disputes initiated in April 2025 alleging misrepresentations related to investment inducement strategies [S6][S7]. Managing such legal scrutiny consumes management bandwidth while amplifying financial uncertainty.

Regulatory compliance—including adherence to evolving FDA frameworks—and cybersecurity oversight practices remain under active board-level supervision given potential disruption scenarios outlined by management involving contractors or CROs handling sensitive data sets [S1]. HIPAA-related compliance obligations across data security frontiers impose added complexity given CalciMedica’s networked research collaborations domestically and internationally [S20][S21].

The absence of approved products compounds reliance on external funding pipelines vulnerable to broader healthcare regulatory headwinds including pricing reforms highlighted through multiple legislative references [S14][S25], demand fluctuations within pandemic-driven therapy markets as seen previously for COVID-19 indications specialize risk factors uniquely borne by biopharma enterprises pursuing transformative anti-inflammatory modalities.

CRAC Channel Platform: Scientific Differentiation and Commercialization Barriers

CalciMedica's proprietary CRAC channel inhibitor platform targets store-operated calcium entry pathways—mechanisms integral to regulating inflammatory cytokine signaling cascades pivotal in many acute inflammatory diseases characterized by calcium-mediated cellular injury. This mechanistic novelty situates CalciMedica at forefront differentiation versus mainstream immunomodulators or anti-cytokine biologics currently deployed clinically .

Auxora's demonstrated ability to potentially attenuate excessive calcium influx hypothesized as a key driver of tissue injury expands therapeutic applicability beyond isolated organ systems into systemic inflammatory states such as pancreatitis-associated SIRS or ARDS triggered by viral pneumonitis . Nevertheless, clinical-stage status creates steep commercialization barriers encompassing long timelines necessary for pivotal validation trials; uncertainty on regulatory approvals remains elevated given evolving standards for demonstrating meaningful mortality or morbidity benefits .

Marketing approval may require high-powered randomized controlled trials specifically designed around validated endpoints accepted by regulators; this phase gating introduces further capital intensity alongside competitive pressure from emergent therapeutics focusing on overlapping inflammatory pathways.

Operational Dependencies: Contractual and Manufacturing Considerations

CalciMedica operates with lean internal infrastructure anchored primarily out of La Jolla headquarters while relying extensively on third-party contract manufacturing organizations (CMOs) for active pharmaceutical ingredient synthesis and formulation processes supporting preclinical through late-stage clinical supply needs [S6][S21]. Such dependence incurs supply chain risks amplified by geopolitical factors impacting international logistics reliability—potentially imperiling timeline adherence for critical clinical material deliveries.

Contracts with vendors typically necessitate advance commitments but generally permit termination upon notice terms between two to three months facilitating flexible responsiveness during funding uncertainties albeit at possible cost penalties [S6]. Recent premises downsizing reflected month-to-month lease adaptation reducing fixed costs commensurate with constrained capital availability signaling prudence amidst ongoing liquidity challenges [S1][S6].

This analysis integrates publicly disclosed SEC filings up through early March 2026 alongside select market news analyses but eschews speculative forecasts beyond explicit stated milestones or guidances absent in disclosures. The presented evaluation balances scientific innovation inherent in CalciMedica’s CRAC platform against material financial headwinds typical for clinical-stage biopharmaceutical firms reliant principally on external equity/debt markets for survival until product approval is achieved.

Readers should recognize that operational advances postulate successful clinical outcomes essential for unlocking prospective financial resources necessary for eventual commercialization—a transition phase laden with scientific as well as business execution risks.

Disclaimer: This report is prepared solely for informational purposes without any recommendation regarding securities purchase or sale. Readers should conduct independent due diligence before making financial decisions related to CalciMedica or similar entities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments