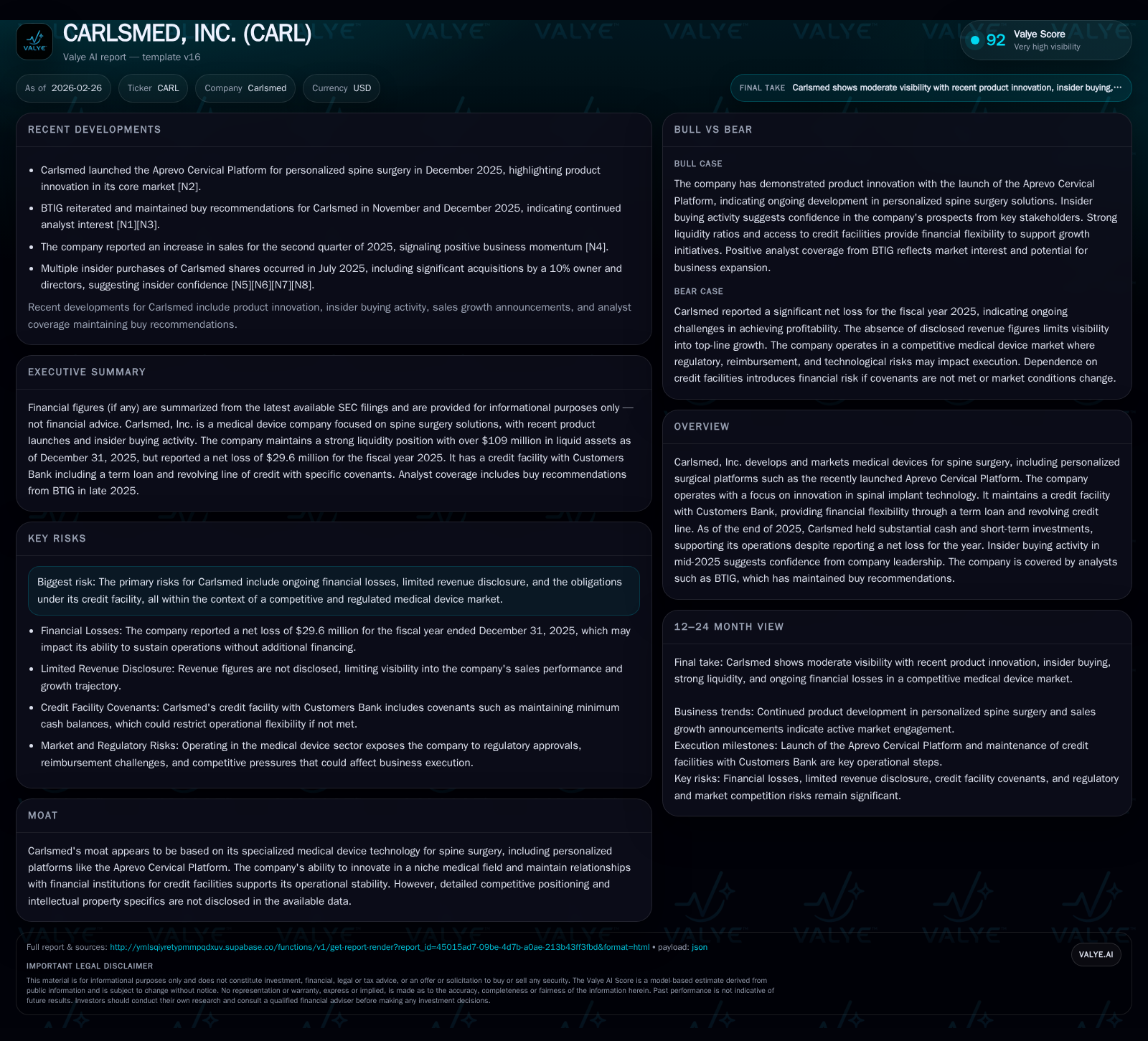

Carlsmed’s Financial Strain Overshadows Innovation in Personalized Spine Surgery Platforms

Despite launching a novel cervical platform and solid cash reserves, Carlsmed, Inc. faces continued losses and tight credit conditions.

Carlsmed, Inc. specializes in medical devices for spine surgery, highlighted by its recent Aprevo Cervical Platform. While innovation in spinal implant technology forms the company's core advantage, Carlsmed’s financial returns remain negative with significant operating losses reported through 2025. The firm maintains a credit facility capped at $50 million with Customers Bank, inclusive of term loans and revolving credit, supporting its liquidity alongside $85.8 million in year-end cash and equivalents. Moving forward, revenue milestones tied to loan terms will be critical to watch as the company navigates the competitive and regulatory regimes of the medical device space.

Company Overview

Carlsmed, Inc., incorporated in Delaware with principal offices in Carlsbad, California, is a medical device company focused exclusively on spine surgery solutions. Its core competency lies in developing innovative spinal implants, notably the newly introduced Aprevo Cervical Platform—an evolution toward personalized surgical platforms aiming to improve procedural outcomes for cervical spine patients.

The company's strategic emphasis on personalization within spinal implant technologies situates it within a highly specialized segment of the orthopedic device industry that demands continuous R&D investment alongside rigorous regulatory compliance.

Historical Financial Performance

Carlsmed's financial trajectory reflects typical challenges faced by companies investing heavily in advanced medical technologies with yet-to-mature commercial traction. For the fiscal year ending December 31, 2025:

- Operating income showed a significant deficit of approximately -$30.6 million.

- Net income loss was about -$29.6 million.

- Cash and cash equivalents remained robust at $85.8 million.

- Current assets totaled roughly $126.7 million against current liabilities near $14.3 million yielding a current ratio close to 8.9.

- Free cash flow was negative by an estimated $29.6 million due to cash outflows exceeding operating cash inflows minus capex.

- Approximate return on equity was -30%, highlighting unprofitable operations despite equity funding support [F1].

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

Operating losses continue despite adequate liquidity due to sizable investment into product development and market penetration efforts—common traits within emerging growth companies focused on disruptive surgical technologies.

Future Growth Prospects

Moving forward, Carlsmed’s growth hinges largely on:

- Commercial adoption of the Aprevo Cervical Platform and associated spine implant products addressing cervical disorders.

- Achievement of revenue milestones tied to incremental borrowing capacity under its credit facility agreements with Customers Bank.

- Expansion into additional spinal segments leveraging proprietary technologies enhancing surgeon personalization capabilities.

- Navigating reimbursement environments affected by evolving healthcare policies influencing hospital purchasing decisions.

Growth may be constrained by ongoing substantial operating losses limiting reinvestment capacity without external financing; competitive pressures from larger established orthopedic/spine device manufacturers; regulatory scrutiny inherent in medical device approvals; and obligations under capital lease and debt agreements requiring minimum revenue thresholds or cash balances [S4][S6][S9].

Credit Facility and Capital Structure

In October 2025, Carlsmed amended its loan agreement with Customers Bank establishing:

- Up to $50 million aggregate credit split between a term loan (up to $50M with $17.5M contingent on revenue milestones) and a $10M revolving line immediately available within total limits.

- Interest rate set at the higher of WSJ Prime +0.25% or a floor of 5.25%, equating recently to approximately 7.5% per annum.

- Term loan maturity scheduled for October 2030 featuring an interest-only period through October 2027 potentially extendable one year upon milestone achievement.

- Covenants mandate maintaining minimum cash deposit levels ($20M) at Customers Bank along with specific revenue tests to maintain borrowing capacity [S4][S10][S11].

Customers Bank holds warrants exercisable for common stock shares derived from preferred series warrants initially issued on prior amendments; these were partially modified reducing outstanding exercisable shares indicating negotiated adjustments tied to financing terms [S11].

Capital Allocation

To date, Carlsmed has not declared dividends or engaged in material share repurchases given its prioritization on sustaining R&D activities and covering operational deficits amidst growth-phase investments [S12][S13][S16]. The company’s capital deployment reflects focus on liquidity preservation while funding product development.

Risk Factors

The company outlines extensive risk disclosures emphasizing:

- Persistent net losses increasing the need for additional capital infusion or alternative financing sources.

- Dependence on successful commercialization of novel spine surgery platforms which may face acceptance barriers among surgeons or hospitals.

- Regulatory risks typical for medical device manufacturers including FDA clearance processes and potential litigation exposures noted without significant active legal proceedings disclosed presently [S1][S5][S6][S8][S14][S15][S17][S18][S19][S20].

Outlook and Monitoring Points (Analysis)

Absent explicit guidance on revenues or detailed commercial milestones beyond those linked to credit facility covenants, critical metrics for monitoring going forward include:

- Quarterly revenue progression relative to thresholds impacting borrowing capacity under bank agreements.

- Cash burn rate trends signaling runway sustainability given operational losses versus liquidity positions.

- Adoption rates of the Aprevo Cervical Platform within targeted spine surgery subsegments.

- Any changes in debt structure or equity financing aimed at extending capital resources.

These data points will reveal if Carlsmed can successfully transition from its early-stage investment phase toward operational break-even anchored by differentiated technology offerings.

Conclusion

Carlsmed presents an illustrative case of an emerging medtech innovator specializing in spine surgery implants struggling with the classic trade-off between heavy upfront investment and delayed profitability. Its substantial cash reserves paired with credit facility flexibility afford operational breathing room through mid-decade timelines but underscore an urgent imperative: scaling commercial traction sufficiently to meet both lender-imposed milestones and internal growth ambitions against stiff market competition and regulation complexity.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments