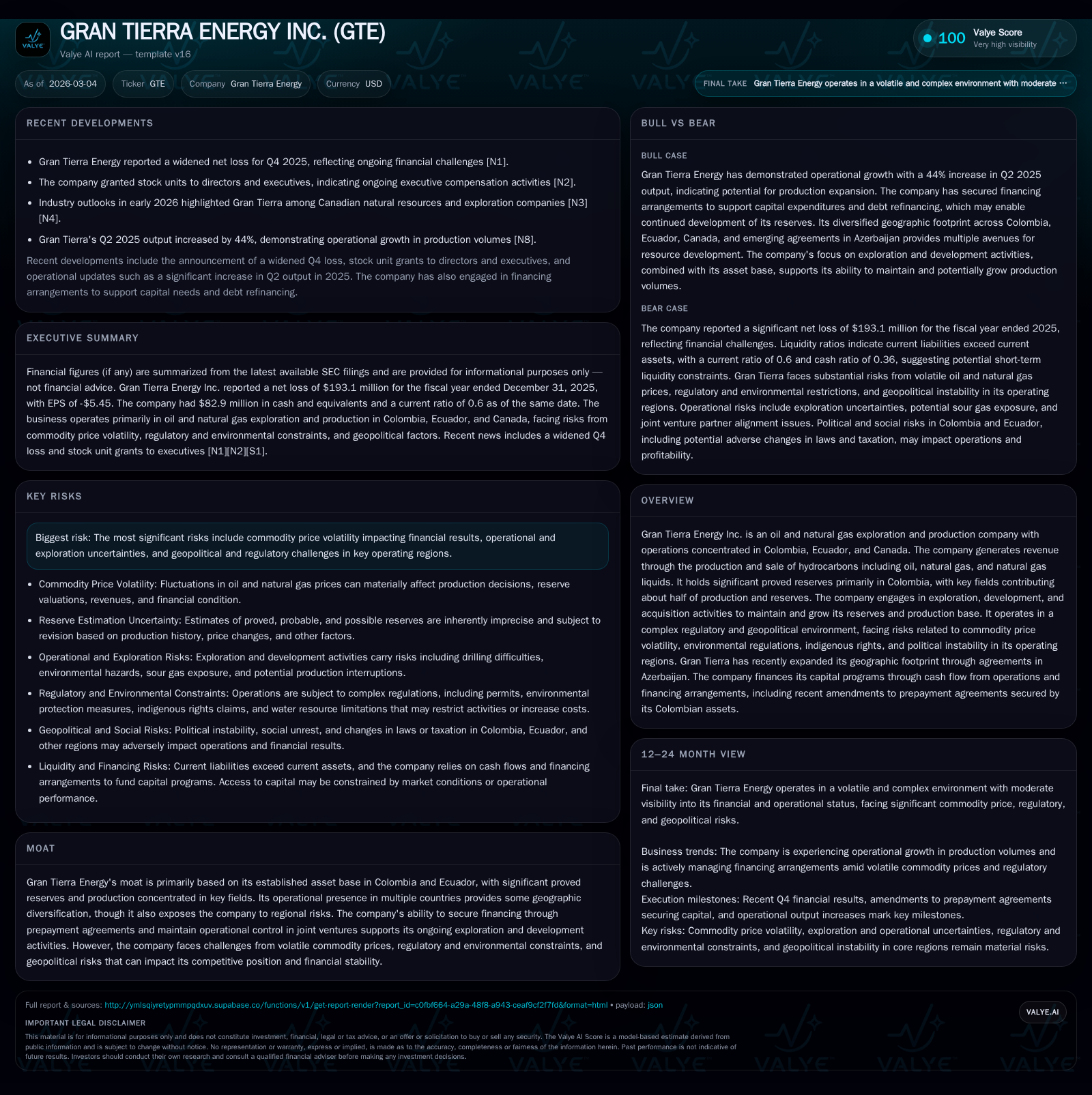

Gran Tierra Energy's 2025 Performance: Reserves concentration and financial turnaround challenges

Gran Tierra’s 2025 financial and operational results underscore challenges from concentrated reserves, widened losses, and complex capital deployment amid geopolitical and price risks.

In 2025, Gran Tierra Energy experienced a dramatic reversal in net income from a modest profit in 2024 to a significant loss, despite strong operating cash flow growth. The company’s production and reserves remain heavily concentrated in four Colombian fields, exposing it to infrastructure and geopolitical vulnerabilities. Strategic exploration in Ecuador and a new foothold in Azerbaijan signify an effort at geographic diversification. However, elevated debt costs and tightened liquidity pose challenges for capital allocation. Regulatory complexities and risks related to pipeline reliability compound the operational uncertainty going forward.

Financial Trajectory: From Positive Margins to Notable Losses

Gran Tierra Energy’s financial performance in 2025 marked a stark reversal compared to prior years. Revenue continuity persisted through the period though exact figures are not detailed in the filings. The headline figure is a net loss of approximately $193 million for fiscal year 2025, compared with a modest net income of $3.2 million recorded in 2024 [F1][N1][S1]. This steep decline translates into a -6104.9% year-over-year change in net income. Yet concurrently, operating cash flow (CFO) increased by approximately 30.9% reaching over $313 million in 2025 from $239 million the previous year [F1]. The disparity between non-cash losses or impairments impacting earnings versus the positive cash flow signals complex factors such as asset write-downs or higher financing costs.

Equity contracted significantly to roughly $229 million by end-2025 down from $414 million last year [F1], yielding an approximate negative return on equity (ROE) of -84.4%, reflective of the large net loss absorbing shareholders’ capital. Capital expenditures declined relative to 2022 but remain substantial to sustain operations [F1][S9]. Share repurchases dampened notably to about $3.5 million in 2025 versus $15.3 million prior year [F1], while dividend payments remain absent, aligning with capital preservation needs amid financial volatility [S12]. Gran Tierra’s liquidity profile remains constrained with a current ratio of roughly 0.6 owing to higher current liabilities exceeding current assets at year-end [F1].

Table: Historical Financial Summary FY2022-2025

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Net YoY |

|---|---|---|---|

| 2025 | -193 | 313 | -6104.9% |

| 2024 | 3 | 239 | +151.2% |

| 2023 | -6 | 228 | -104.5% |

| 2022 | 139 | 428 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 3 | -84.4 |

| 2024 | 15 | 0.8 |

| 2023 | 17 | -1.6 |

| 2022 | 27 | 33.3 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures disclosed only for FY2025; capex guidance/spending figures referenced qualitatively but not quantified annually.

Operational Footprint: The Colombian Core and Pipeline Vulnerabilities

Gran Tierra’s operations are notably focused on four Colombian fields—Acordionero, Costayaco, Moqueta, and Cohembi—that together accounted for about half of total production and proved reserves as of end-2025 [S8][F1]. This geographic concentration creates exposure to region-specific supply chain factors including limited access to buyers and logistical bottlenecks.

Among infrastructure challenges are outages reported on Ecuador’s major crude oil transit routes—the Oleoducto de Crudos Pesados (OCP) pipeline and the Sistema de Oleoductos Trans Ecuadoriano (SOTE). These events were driven by significant soil erosion near the Coca river area leading to temporary service disruptions [S8]. Though rerouted sections have restored flow capacity recently, the pipeline throughput constraints accentuate reserve life management concerns given that uninterrupted transport is crucial for commercial realization of upstream production.

Upstream production faces inherent decline rates typical in mature fields; Gran Tierra must continuously manage reservoir performance through development drilling aided by technical analysis based on reservoir modeling [S9]. The company’s reliance on localized output amplifies operational leverage risk since any single disruption could materially impact total volumes.

Exploration and Expansion: Geographic Diversification and Azerbaijan Entry

Strategically seeking growth beyond its core South American operations, Gran Tierra has expanded its portfolio through newly awarded exploration blocks within Ecuador plus entry into Azerbaijan via arrangements with the State Oil Company of Azerbaijan Republic (SOCAR) [N3][S8][S9].

These frontier hydrocarbon basins represent both opportunity and complexity. Operating under multi-jurisdictional frameworks introduces regulatory hurdles including sovereign risk considerations distinct from Colombia or Ecuador norms. Geopolitical risk mitigation thus factors heavily into exploration planning given historic armed conflicts and interstate tensions within the Caucasus region [S15].

Exploration block activity includes both appraisal drilling targeting increased recovery factors as well as seismic surveys to map subsurface structures [S9]. Success hinges on technological capabilities including seismic interpretation software combined with logistical synchronization across global teams.

Capital Deployment: Balancing Cash Flow, Debt Costs, and Shareholder Returns

In February 2026 Gran Tierra issued about $488 million aggregate principal amount of senior secured amortizing notes maturing in 2031 carrying a coupon rate of approximately 9.75% per annum—signaling elevated debt costs reflecting credit risk perceptions prevalent across the oilfield services sector amid commodity price uncertainty [S5][S6][S20][N1]. These notes replaced earlier ones due in 2029 via an exchange offer settled partially with cash consideration.

The indenture imposes covenants limiting incremental indebtedness while restricting payments such as dividends or share repurchases outside prescribed thresholds [S5][S12][S28]. Liquidity management therefore prioritizes operational funding alongside necessary capex spending within an announced range of $120 million to $160 million for ongoing exploration and development programs for fiscal year 2026 [S6][S9]. These expenditures aim at sustaining reserve replenishment despite volatile pricing.

Share buyback activity has retreated sharply to a few million dollars last year from nearly $15 million previously [F1], concurrent with no dividend distributions noted recently—a prudent preservation stance under tighter credit conditions.

Geopolitical and Regulatory Landscape Impacting Growth

Gran Tierra navigates an inherently complex environment featuring intertwined political instability risks predominantly within Colombia and Ecuador where social unrest related to indigenous rights protests may interrupt production or field operations unexpectedly [S4][S11].

Environmental regulation enforcement continues tightening globally aligned with commitments under international frameworks such as the Paris Agreement—with heightened scrutiny applied locally towards greenhouse gas emissions limits potentially affecting cost structures via carbon taxes or mandatory disclosures [S17][S18]. In addition to scheduled operational permits requiring renewal under stringent conditions potentially leading to suspension if violated [S25], pipeline rehabilitation amid natural hazard vulnerability remains critical courtesy of tropical soil erosion events impacting Ecuadorian transit routes [S8].

Corruption risk inherent to emerging markets also presents exposure under anti-bribery statutes applicable across jurisdictions such as U.S., Canada, Colombia and Ecuador—with extension anticipated for newly entered geographies like Azerbaijan—all mandating strict internal controls though inadvertent breaches carry reputational penalties or legal sanctions [S21].

Forward-Looking Considerations: Price Sensitivities and Financing Needs

Looking ahead analysts will focus keenly on Brent-WTI oil price differentials given their direct bearing on Gran Tierra’s realized pricing after adjustments for quality differentials transportation fees which heavily influence margins [N1][N3][S6][F1]. The company stresses funding its capital program primarily through operating cash flows conditioned on average Brent prices near $65/barrel and WTI near $61/barrel assumptions embedded within planning documents yet recent natural gas price weakness introduces some funding uncertainty given C$3/mcf targets versus actuals closer to C$2/mcf so far this year [S6].

Without adequate cash flows or external financing availability—subject to credit climates—Gran Tierra may need to delay discretionary projects or explore alternative joint venture arrangements [S6][N3]. Absence of additional capital would constrain reserve replacement potentially compressing future production volumes.

The upcoming periods will also test effectiveness of hedging protocols if implemented given ongoing commodity price volatility plus potential tax regime adjustments connected with evolving environmental policies escalating compliance costs unpredictably thereby impacting breakeven levels.

This analysis synthesizes publicly filed financial data along with regulatory disclosures and recent news updates without constituting investment advice or forecasts beyond documented evidence sources.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments