How Muncy Columbia Financial Leverages Localized Banking Amid Regional Economic Pressure

Post-merger integration amplifies community banking strengths while capital management underpins resilience in a competitive Pennsylvania market.

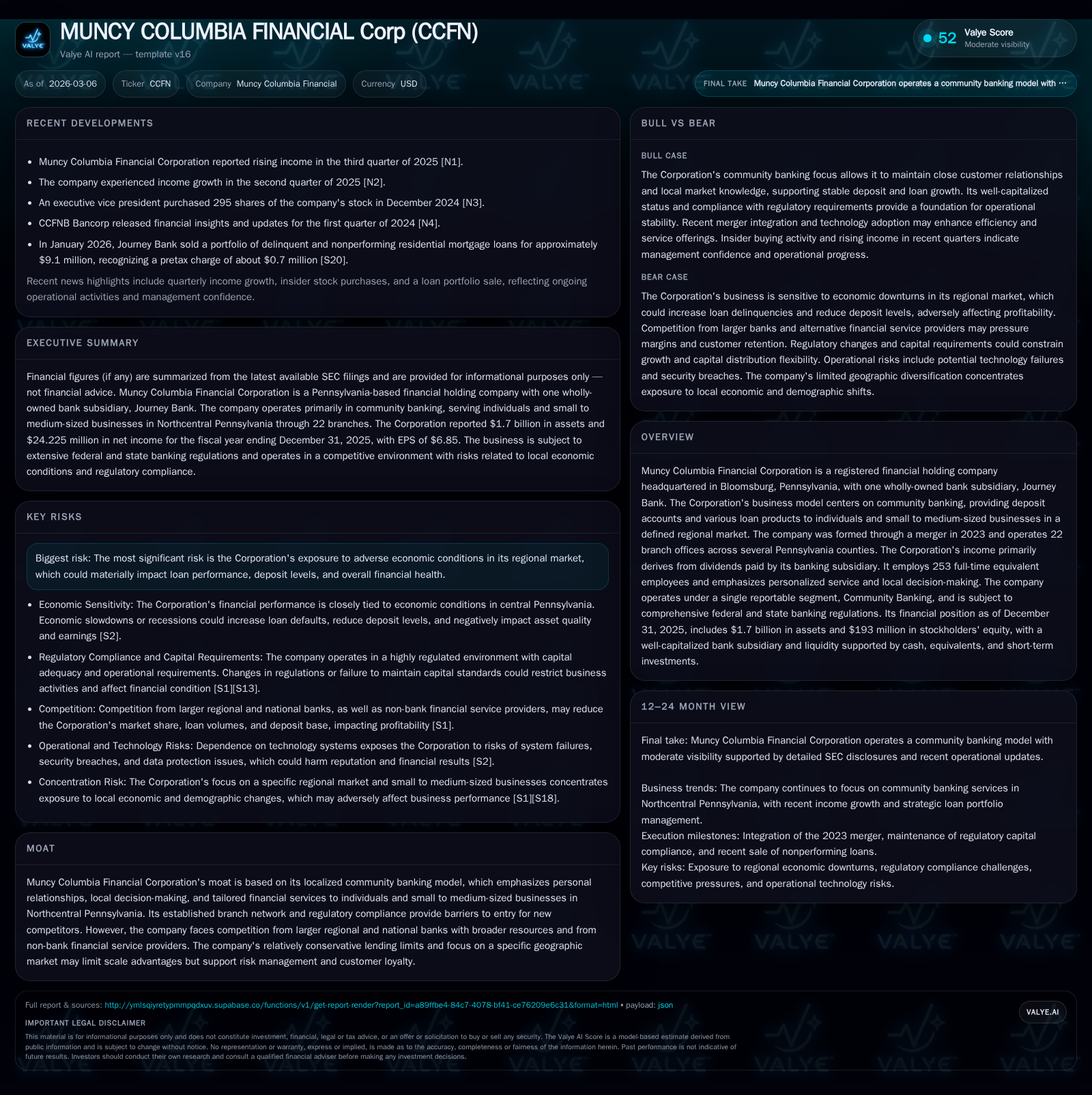

Muncy Columbia Financial Corporation’s formation through a 2023 merger expanded its asset base to $1.7 billion and reinforced its community banking model centered on local relationships and personalized service. The company has demonstrated rapid net income growth, supported by disciplined capital allocation and strong operating cash flows. Its conservative credit policies and regional focus foster customer loyalty but present challenges in competing against larger institutions. Navigating localized economic risks and evolving regulatory frameworks remains critical as the company balances growth ambitions with prudent risk management.

Merger Genesis and Historical Growth Drivers

Muncy Columbia Financial Corporation emerged from the November 2023 merger between CCFNB Bancorp, Inc., and Muncy Bank Financial, Inc.—a strategic combination described as a merger of equals [S1]. This union consolidated two regional players into a single entity with a substantially enlarged footprint across Pennsylvania counties including Clinton, Columbia, Lycoming, Montour, and Northumberland.

Post-merger, the newly named Muncy Columbia Financial Corporation controls Journey Bank (the surviving bank entity), boasting a total asset base of approximately $1.7 billion as of December 31, 2025 [F1][S1]. The merger facilitated not only scale gains but intensified operational synergies—reflected unmistakably in net income progression: from $3.39 million reported in FY2023 immediately after the merger, rising to $19.0 million in FY2024, climbing further to $24.2 million by FY2025 [F1].

This growth trajectory underscores the effectiveness of consolidating local community banking franchises to strengthen competitive positioning within their shared regional market. It also accentuates how combining overlapping branch networks—22 locations currently—and harmonizing operations can deliver enhanced profitability without diluting the personalized service traditionally offered.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 24 | 23 | 1395000 | +27.3% |

| 2024 | 19 | 17 | 407000 | +461.6% |

| 2023 | 3 | 7 | 968000 | |

| 2013 | 7 | 293000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($) | FCF ($mm) |

|---|---|---|---|

| 2025 | 8 | 22 | |

| 2024 | 6 | 1517000 | 16 |

| 2023 | 4 | 25000 | 6 |

| 2013 | 3 | 625000 |

Source: SEC companyfacts cache [F1].

Small number of buybacks reported for FY2023 but exact comparable data lacking for FY2025.

Financial Performance: Trends in Profitability and Cash Flow

The corporation’s post-merger growth is mirrored in rising profitability metrics alongside substantial improvements in operational cash flow efficiency [F1]. FY2025 showed a healthy net income increase of 27.3% year-over-year building on an already sharp jump from the previous year. Operating cash flow similarly expanded by nearly 38%, signaling robust earnings quality and solid internal liquidity generation.

Capital expenditures surged over 240% year-over-year in FY2025 relative to FY2024—a clear signal of strategic reinvestment possibly toward technology upgrades or branch enhancements that underpin community banking competitiveness [F1]. With equity increasing steadily due to retained earnings accumulation plus possibly accretive effects from post-merger integration benefits reaching maturity phases [F1], return on equity calculates near an industry-respectable circa 12.6% for FY2025 ([net income/equity] approximation from [F1]).

Such ROE indicates competent capital stewardship compared with regional banking peers who often target double-digit returns balanced against regulatory capital cushions.

Community Banking Model: Local Relationships as Competitive Moat

Operating exclusively under a "Community Banking" reportable segment reflects Muncy Columbia Financial’s dedication to relationship-intensive banking [S1][S5]. Their business philosophy emphasizes direct access between customers and senior team members—with local credit underwriting allowing timely decisions reflecting nuanced understanding of borrowers’ circumstances.

By focusing primarily on individuals plus small- to medium-sized enterprises (SMEs) within defined counties of Northcentral Pennsylvania—and servicing them through twenty-two brick-and-mortar branches—the bank cultivates loyalty grounded on personal service rather than scale economies or technology-driven efficiency common at national banks [S1][S5].

The moat tightens as expansive regulations coupled with entrenched customer relationships deter new entrants; however geographic narrowness limits scalability advantages compared to multi-state competitors leveraging more diverse economies.

Competitors include large regional banks enjoying broader resources and fintech entrants offering digital convenience absent physical footprint limitations—challenging Muncy Columbia’s ability to retain younger demographic segments accustomed to app-based financial solutions [S5]. Nonetheless its distinct local credit culture remains a durable edge for risk control.

Loan Portfolio Strategy and Balance Sheet Composition

At year-end 2025 Journey Bank had approximately $1.2 billion gross loans alongside $1.4 billion in deposits supporting loan growth ambitions within conservative risk boundaries [S1][F1]. The company applies internal lending limits significantly more restrictive than the legal maximum cap (regulations limit single borrower exposure to roughly 15% of bank capital plus an additional allowance for highly collateralized loans), rendering it less flexible than competitors for large corporate credits [S4].

To remain compliant yet serve occasional larger clients requests amid internal ceilings on single borrower exposure, the institution routinely utilizes loan participations—syndicating portions of sizable credit commitments to other financial entities thus managing concentration risk effectively [S4].

Collateral generally encompasses real estate alongside business assets like equipment or inventory; however reliance principally lies on borrower cash flows given inherent depreciation and valuation uncertainty associated with these collateral types [S4]. Deposit stability remains paramount with low-cost core deposits forming primary funding source—challenged periodically by competition-induced deposit rate pressures but mitigated through long-standing regional client bases [S5][S14].

Navigating Regional Economic Risks and Market Competition

A central vulnerability arises from economic dependency on central Pennsylvania markets where downturns disproportionately affect borrower repayment capacity and deposit inflows [S1][S2][S26]. Unlike diversified larger institutions nationwide able to offset localized stress via multiple markets exposure, Muncy Columbia faces concentration risks where SME clients possess limited financial buffers against recessions or sectoral downturns.

Competition intensifies not only among traditional banks increasing acquisition-driven consolidation but also from digitally agile non-bank lenders targeting mortgage lending and small businesses with non-traditional underwriting models [S5][S8]. This dynamic exerts pressure on both loan pricing power and deposit gathering strategies forcing tactical responses balancing local service values against emerging technological demands.

Additionally, macroeconomic uncertainties tied to federal fiscal policy gridlocks or tariffs amplify risks indirectly impacting local credit quality through employment trends or real estate valuations [S2][S16].

Capital Allocation, Dividend Policy, and Shareholder Returns

The corporation has maintained disciplined capital deployment policies post-merger evidenced by consistent dividend growth—from $3.56 million dividends paid in FY2023 up toward $8.13 million by FY2025—and modest but accelerating share repurchases notably reported during FY2024 at $1.52 million after negligible buybacks earlier years [F1][S3]. By preserving approximately $21.9 million free cash flow (operating cash flow minus capex) annually in the last fiscal period examined ([F1]), the firm demonstrates ample internal liquidity supporting stable shareholder distributions alongside reinvestment initiatives.

Regulatory capital ratios comply comfortably with Basel III-inspired requirements including leverage ratio minimums leaving no immediate pressure on risking capital constraints during growth phases [S7][S12][S17]. The "source-of-strength" doctrine further compels holding company readiness to support subsidiary liquidity if required underscoring an emphasis on prudent capital coverage reflective of banking regulatory imperatives [S4][S15].

Outlook and Key Milestones: Strategic Initiatives to Watch

Explicit forward-looking guidance is not provided within available filings; therefore stakeholder attention should focus analytically on emerging trends such as continuation or scale changes within loan participations sales strategies affecting credit risk distribution. Monitoring deposit base composition shifts—especially gauging competitiveness in interest rates offered—will also indicate adaptability amidst evolving market consolidation forces.

Additionally keeping track of expenditures classified under capex will reveal strategic priorities on technology implementation or branch modernization critical for sustaining community banking relevance in digitally evolving contexts.

Regulatory Framework Impacting Ongoing Operations

As a regulated entity operating under intricate federal and state supervision regimes governing lending practices—including stringent caps on borrower exposures—and extensive consumer protection statutes relating to privacy/data security standards,[...] along with environmental assessment obligations for certain loan types—the company must continuously calibrate compliance structures with evolving normative expectations [S4][S8][S26]. Certificate classifications by regulators deem Journey Bank well-capitalized under all current standards ensuring authorized operational scope without imminent regulatory restrictions [S11][S12].

Moreover adherence to Community Reinvestment Act requirements—which recently underwent proposed amendments—is crucial given their potential impact on franchise expansion approvals such as new branch establishment or relocations demonstrating societal responsibility alongside financial prudence [S19]. Notably federal directives impose liability principles requiring the holding company’s financial strength underpinning subsidiary banks reinforcing accountability throughout corporate structure layers [S15][S24].

This analysis is based solely on publicly filed documents as of March 6th, 2026 and does not constitute investment advice nor an investment recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments