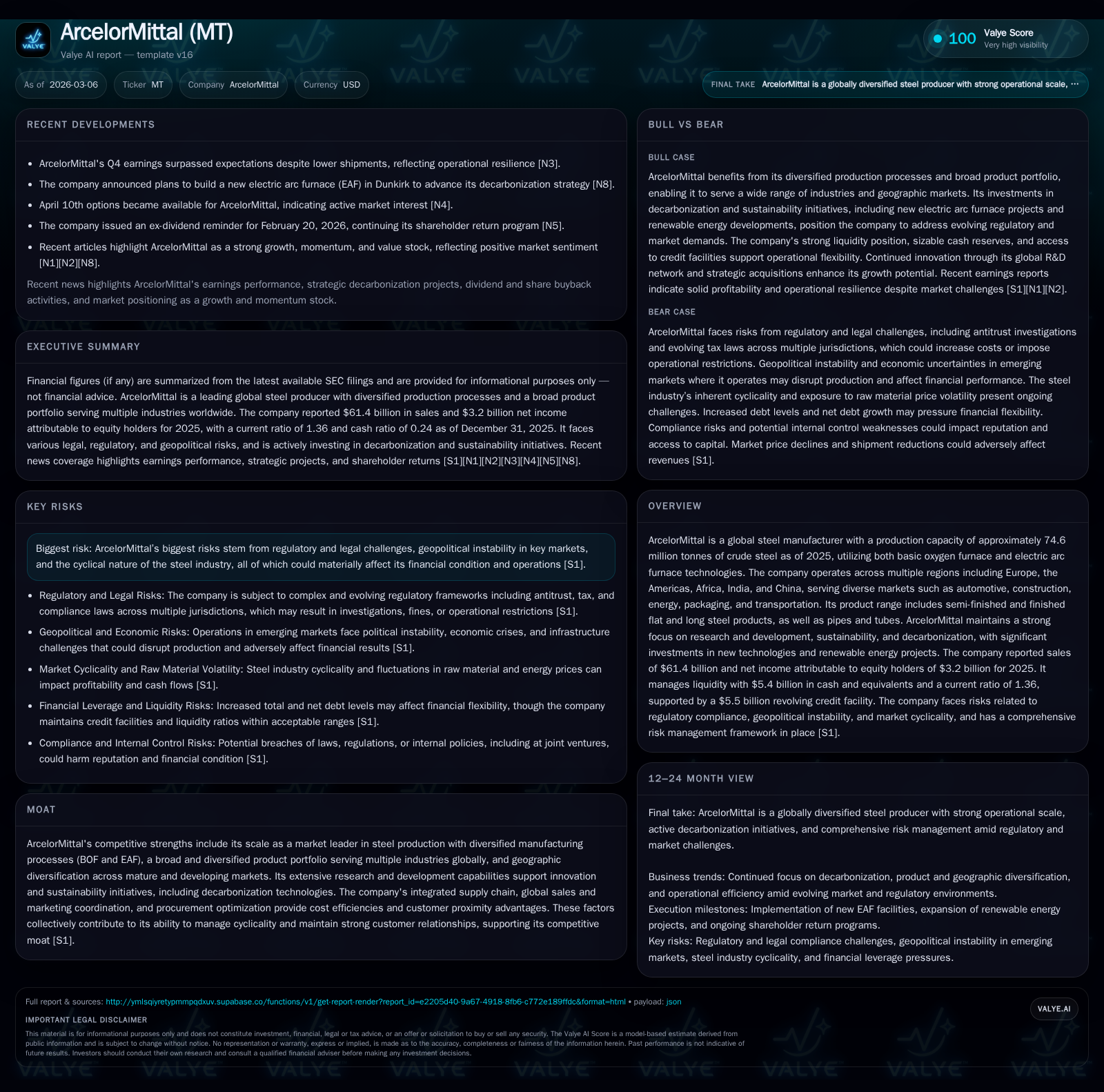

ArcelorMittal’s Strategic Expansion and Decarbonization Amid Rising Leverage and Cyclical Risks

A global steel leader capitalizing on diversified markets, technological innovation, and sustainability, balancing growth with elevated net debt and regulatory challenges.

ArcelorMittal commands a significant position in the global steel industry with over 74 million tonnes crude steel capacity as of 2025, serving various end markets through both BOF and EAF technologies. The company has demonstrated robust net income growth recently, more than doubling profits in 2025 versus 2024, driven by operational efficiencies and market recovery. Strategic investments focusing on decarbonization, including a major new electric arc furnace in Dunkirk, underline its commitment to sustainable steelmaking. However, rising total debt to $13.4 billion and geopolitical exposure present balancing risks. Share repurchases and steadily rising dividends indicate disciplined capital returns alongside ambitious growth plans.

Company Overview and Historical Performance

ArcelorMittal remains the world's largest steel producer with an achievable annual crude steel capacity near 74.6 million tonnes as of the end of 2025 [S1]. Its dual-technology approach combines traditional basic oxygen furnace (BOF) capacity with electric arc furnace (EAF) facilities, allowing flexibility to optimize costs and emissions intensity depending on market conditions.

Sales reached approximately $61.4 billion in 2025 (latest available figures), supporting net income attributable to equity holders of $3.24 billion — a substantial improvement over prior years which saw earnings around $1.38 billion in 2024 and $1.02 billion in 2023 [F1]. This reflects a concerted focus on operational efficiencies during recovering steel demand globally.

Historical performance (annual)

| FY | Net ($bn) | Net YoY |

|---|---|---|

| 2025 | 3.2 | +135.0% |

| 2024 | 1.4 | +35.0% |

| 2023 | 1.0 | -89.3% |

| 2022 | 9.5 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | ROE% |

|---|---|---|

| 2025 | 548 | 5.7 |

| 2024 | 585 | 2.7 |

| 2023 | 520 | 1.8 |

| 2022 | 636 | 17.2 |

Source: SEC companyfacts cache [F1].

Note: Revenues reported up to FY2017 at $68.68B are historical data points; recent years do not have disclosed revenues but focus here is on profitability metrics.

Industry Positioning and Competitive Strengths

ArcelorMittal's competitive moat derives from its sheer scale coupled with an integrated business model encompassing mining, steelmaking, downstream processing, distribution centers, and global sales networks [S1]. This integration supports cost advantages while maintaining close customer relationships across automotive, construction, packaging, energy sectors among others.

The company’s geographic diversification spans mature markets such as Europe and the Americas as well as fast-growing regions including India, Africa, China, Southeast Asia, and South America—a strategic hedge against localized cyclical volatility [S25][S26].

Procurement practices embrace a Total Cost of Ownership methodology that prioritizes cost efficiency through optimized supplier contracts, logistics improvements, material recycling efforts, and technological upgrades—critical in an industry where raw material costs may account for over half of total production cost [S21].

Growth Drivers and Future Outlook

Decarbonization Initiatives

A major catalyst for ArcelorMittal’s future growth is its aggressive pivot toward sustainability and climate change mitigation through technology adoption such as increased EAF usage which significantly reduces CO2 emissions compared to BOF processes [N12][S3]. The confirmed €1.3 billion investment into a new electric arc furnace facility in Dunkirk represents a cornerstone project aimed at expanding low-emission capacity consistent with the EU Green Deal directives.

Market Demand Recovery & Product Innovation

Emerging market infrastructure development alongside recovering automotive production are expected to sustain steel demand growth where ArcelorMittal holds strong client ties reinforced via early vendor involvement models especially in technical flat products tailored for light-weight automobiles [S28]. Concurrently, innovation leveraging AI-driven process modeling expedites new product development cycles vital for high-margin specialty steels.

Acquisitions & Capacity Expansion

Recent acquisition activity—including the Calvert plant purchase (~$1.2B)—and strategic investments bolster incremental production capability principally focused on long-term value rather than short-term margin capture [S13][S26]. Managing these expansions within cyclical headwinds will be critical.

Financial Health & Capital Allocation

Total debt rose by nearly $1.8 billion during 2025 to $13.4 billion driven by acquisitions ($1.9B estimated consolidated addition primarily from Calvert), share buybacks ($0.3B), dividend payouts ($0.4B), partly offset by robust operating cash flows ($4.8B) after capital expenditures ($4.3B) [S13][F1].

Cash holdings stood at approximately $5.4 billion maintaining adequate liquidity while net gearing increased from ~9.9% to ~14% reflecting these activities but credit rating upgrades signal improved financial stability [F1][S4]. The average debt maturity extended to nearly eight years providing refinancing flexibility with no covenant breaches reported.

Dividend policy remains progressive: base annual dividends were raised to $0.55 per share for fiscal year-end 2025 from $0.50 prior year with a board proposal for further increase to $0.60 per share approved subject to shareholder consent in May 2026 [S10]. Share repurchase programs continue under a framework allowing up to ten million shares per tranche until mid-2030 contingent on free-cash-flow generation post dividend—the latest tranche having repurchased two million shares at average prices near €25 [$29] per share by end-2025 [S6–S11].

Risks & Regulatory Environment

Despite strengths, ArcelorMittal faces material risks including:

- Regulatory complexities covering environment (carbon emission compliance under evolving EU regulations), anti-trust scrutiny given market size dominance concerns—any adverse rulings could impact operations or require divestitures [S17][S20][S23].

- Geopolitical instability especially within emerging markets like Brazil or India affects supply chains and demand prospects; economic disruptions in countries such as Argentina or Turkey hold precedent impact cases [S1][N2].

- Commodity price volatility influencing input costs despite procurement hedging countermeasures.

- Potential legal actions related to antitrust or compliance issues remain an ongoing corporate governance concern requiring vigilant internal controls.

Summary & Monitoring Points

ArcelorMittal leverages unparalleled scale paired with diversified technologies positioning it well to capture long-term growth leveraging decarbonization ambition and emerging market exposure amidst recovering global demand post-pandemic disruptions. Key metrics to watch include:

- Execution progress on new EAF facilities including Dunkirk commissioning timelines.

- Free cash flow generation after capital spending influencing future share buybacks or dividend hikes.

- Developments in geopolitical risks impacting operational continuity.

- Regulatory environment changes notably carbon pricing regimes or antitrust investigations.

- Steel shipment volume trends versus historical comparative baselines given sector cyclicality.

The company’s financial discipline evidenced by sustained liquidity management alongside strategic capital returns reflects an engaged balancing act addressing growth ambitions while managing gearing levels across volatile industry cycles.

This analysis presents factual company information aggregated from verified filings and reports without any investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments