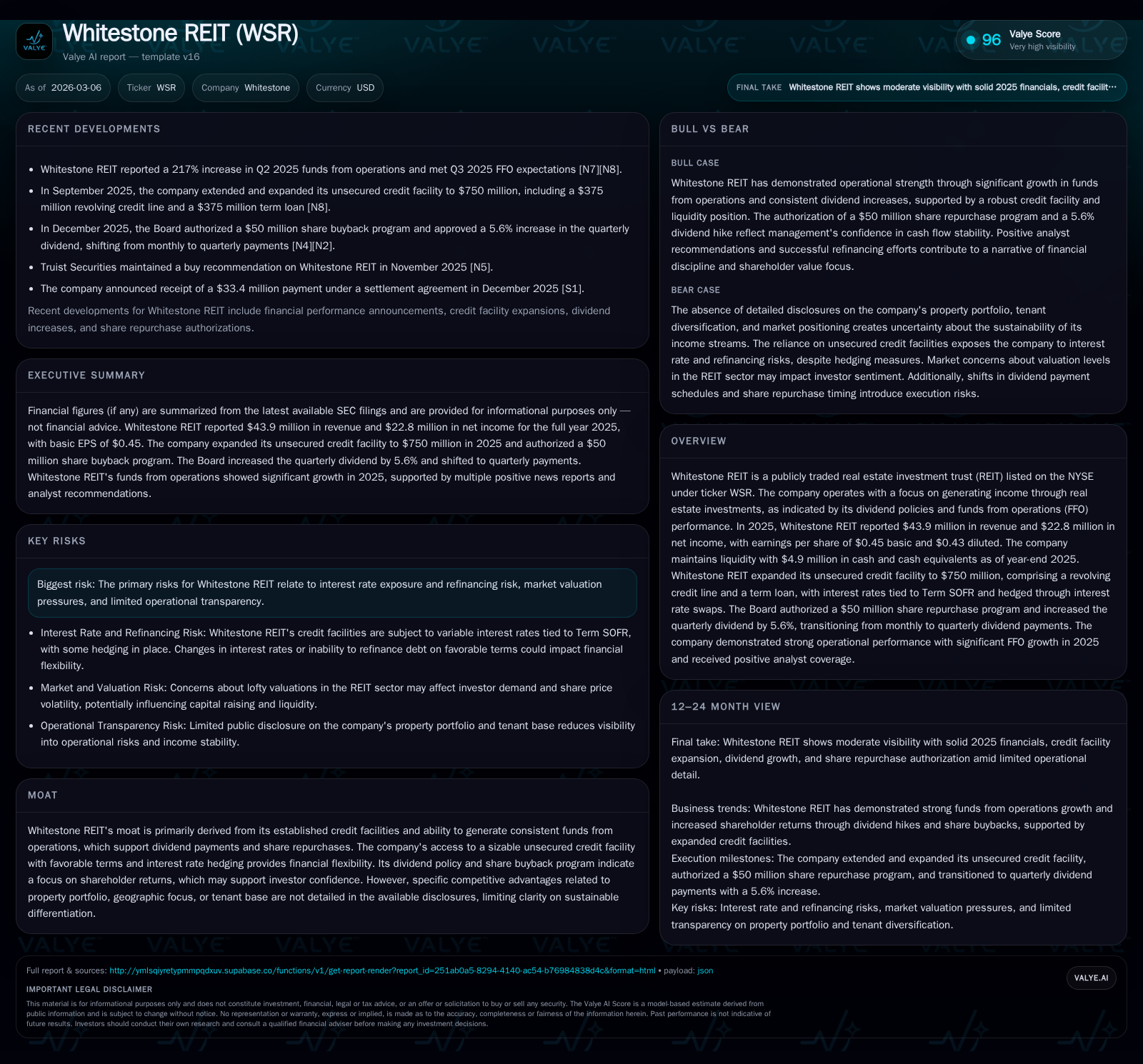

Whitestone REIT Strengthens Financial Foundation With Credit Expansion and Shareholder Returns

Whitestone REIT’s 2025 year-end results reflect solid revenue and profitability growth, supported by an expanded unsecured credit facility and enhanced capital return programs signaling disciplined financial management.

In 2025, Whitestone REIT posted a 7.5% increase in revenue to $43.9 million alongside a 31.7% jump in net income to $22.8 million, driving stronger earnings per share. The company further bolstered liquidity with a $750 million unsecured credit facility comprising a revolving line and term loan with interest hedging, enhancing refinancing flexibility amidst rate volatility. Strategic shareholder returns were amplified via a newly authorized $50 million share repurchase program and a 5.6% dividend increase paired with a transition from monthly to quarterly dividend payments. Whitestone’s prudent capital allocation and risk management position it for measured growth while navigating typical REIT sector cyclical risks.

Revenue and Earnings Momentum in 2025: Drivers Behind the Growth Trajectory

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 44 | 23 | 51 | 300000 | +7.5% | +31.7% |

| 2024 | 41 | 17 | 58 | 200000 | +8.8% | +1025.0% |

| 2023 | 38 | 2 | 48 | 100000 | +7.5% | -92.3% |

| 2022 | 35 | 20 | 44 | 100000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 27 | 2 | 50 |

| 2024 | 25 | 3 | 58 |

| 2023 | 24 | 1 | 48 |

| 2022 | 23 | 1 | 44 |

Source: SEC companyfacts cache [F1].

Whitestone REIT demonstrated solid top-line expansion in fiscal year 2025, with revenue rising by approximately 7.5% year-over-year to reach $43.9 million compared to $40.8 million in the prior year [F1]. This growth appears linked to operational efficiencies or possibly improved portfolio yields, though specific property-level details remain undisclosed in the filings [S3]. Notably, net income showed significant acceleration, climbing over 31%, from $17.3 million in 2024 to $22.8 million in 2025 [F1]. This considerable margin expansion translated into basic earnings per share of $0.45 and diluted EPS of $0.43 for the period [S1], signaling effective cost management alongside revenue gains.

Within the REIT sector framework, such income growth often correlates with stronger funds from operations (FFO) metrics supporting distributable cash flows; Whitestone's improving bottom line thus aligns with its moat centered on consistent FFO generation . This earnings momentum is critical amid competitive pressures where portfolio yields directly influence investor return profiles.

Liquidity Boost Through Credit Facility Expansion: Flexibility Amid Rate Volatility

September 2025 marked a pivotal liquidity milestone as Whitestone REIT secured a substantially expanded unsecured credit facility totaling $750 million [S5]. This facility is bifurcated into a $375 million revolving credit line due September 19, 2029 (extendable semi-annually up to September 2030) and a $375 million term loan maturing January 31, 2031 [S5].[S9]. Borrowings under this facility carry interest rates linked to Term SOFR plus leverage-based spreads, approximately at SOFR +1.35%-1.40% current margins for the revolver and term loan segments respectively [S9].

Importantly, Whitestone has implemented interest rate swap agreements that effectively fix the Term SOFR portion of the term loan's interest expense through maturity stages extending out to January 2031 [S9]. This hedging approach mitigates exposure amid volatile short-term rates—a notable risk factor for real estate firms reliant on floating rate debt [S4][S8]. Additionally, no collateralization is required on this unsecured financing, enhancing balance sheet flexibility.

The expanded facility laid groundwork for refinancing about $368 million of prior debt obligations at more favorable terms while preserving key financial covenants consistent with previous arrangements [S10][S13]. This strategic capital structure optimization supports Whitestone’s ability to weather market valuation fluctuations commonly seen in REIT markets.

Shareholder Returns Enhanced: From Dividend Policy Shifts to Buyback Authorizations

In late December 2025, Whitestone’s Board authorized an ambitious shareholder return initiative featuring a new share repurchase program permitting up to $50 million of common stock buybacks through May 20, 2028 [S7][S11]. Repurchases may be executed through various mechanisms, including open market transactions or accelerated programs depending on prevailing market conditions and corporate discretion.

Simultaneously, the Dividend policy shifted from monthly disbursements to quarterly payments—with the initial quarterly dividend raised by approximately +5.6% to $0.1425 per share/unit effective Q1 2026 [S7][S11]. Such timing adjustments aim at dividend yield optimization allowing consolidated distributions that reduce administrative costs while sustaining shareholder income streams.

This balanced capital allocation approach underscores a focus on maintaining robust dividend coverage supported by consistent funds from operations while utilizing buybacks opportunistically when shares trade attractively.

Operating Cash Flow Dynamics and Capital Expenditure Trends

While revenue showed continued growth, operating cash flow (CFO) contracted moderately by about -12.8% year-over-year—from roughly $58.2 million in 2024 down to just over $50.7 million in fiscal year 2025 [F1]. The decline could suggest timing differences in receipts or increased operating expenses but remains within reasonable fluctuation typical for property management cycles.

Capital expenditures remain minimal yet increased somewhat tripling from prior years’ levels—rising from roughly $100k annually up to $300k in FY25—indicating modest reinvestment focused likely on maintenance rather than aggressive expansion [F1].

The combination results in strong free cash flow generation (~$50.47 million), supporting sustainable dividends as confirmed by steady payout levels near $27.4 million annually [F1]. This only reinforces Whitestone’s capability of funding distributions internally without heavy reliance on external equity or debt issuance.

Balance Sheet Strength and Return on Equity Assessment

Whitestone’s balance sheet reflects solidity with total equity rising approximately as well—from about $438 million at end-2024 to around $458 million at end-2025 alongside net income growth momentum [F1][S6]. Calculated return on equity for fiscal year reporting stands near an estimated 5%, indicating efficient utilization of shareholders' capital despite sector pressures associated with real estate asset cycles.

Maintaining conservative leverage levels facilitated by strong equity accumulation supports ongoing dividend coverage prudently while enabling room for financial maneuvering regarding future acquisitions or strategic initiatives [S6][S13]. Equity growth trajectory combined with positive net income trends represents crucial elements underpinning investor confidence.

Navigating Interest Rate and Refinancing Risks: Hedging and Covenant Considerations

Interest rate risk featured prominently among the key risk factors disclosed by Whitestone given its sizable floating rate borrowings indexed primarily to Term SOFR plus margins that fluctuate based on leverage ratios [S4][S8][S13]. However, the employment of interest rate swaps fixed portions of outstanding debt costs specifically on the term loan tranche until January 2031 mitigates exposure significantly.

Furthermore, the amended credit agreement preserves principal covenant tests ensuring compliance within defined leverage limits enhancing borrowing stability over medium term horizons even amid potential rate hikes or economic downturns [S9][S13]. These covenant structures generally provide lenders comfort while giving Whitestone operational leeway.

Refinancing risk remains managed via maturity extensions afforded through multi-year revolver options and long-dated term loans replacing previous shorter tenor facilities [S10][S17]. Such staggered maturities ease concentrated risk spikes common among REITs facing compressed financing windows.

The combined effects of these financial instruments demonstrate institutional-grade balance sheet governance customary among proactive real estate operators responding adeptly to market volatility drivers inherent within fixed asset portfolios.

Looking Ahead: Milestones, Market Conditions, and Strategic Watchpoints

Absent explicit forward guidance beyond current disclosures [N1][S7][S11], investors should monitor execution pace against the newly authorized share repurchase program as an indicator of management confidence aligned with valuation levels.

Dividend sustainability under inflationary or interest rate shift scenarios will be pivotal given continued emphasis on yield attraction via quarterly payout scheduling coupled with incremental increases.$ Likewise, approaching maturity dates demand vigilance toward refinancing terms especially after leveraging substantial unsecured credit capacity optimized recently.

Additional factors such as tenant retention dynamics or localized real estate market conditions—though not fully elucidated—may subtly influence operational cash flows moving forward.

Continued oversight of cash flow trends relative to capex outlays will provide clarity on reinvestment intensity versus distribution prioritization reflecting strategic capital allocation discipline observed historically.

Beyond headline numbers, Whitestone’s evolving interaction between financial engineering safeguards like swap agreements and shareholder-oriented policies will prove influential amid sector cyclicality expectations.

Disclaimer: This report is for informational purposes only reflecting facts as disclosed by Whitestone REIT's SEC filings and company releases through March 2026 without intention of investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments