First Community Bankshares Reports Mixed Earnings as Acquisition Broadens Reach

FCBC expands its regional footprint through acquisition while contending with slight earnings pressure and competitive challenges.

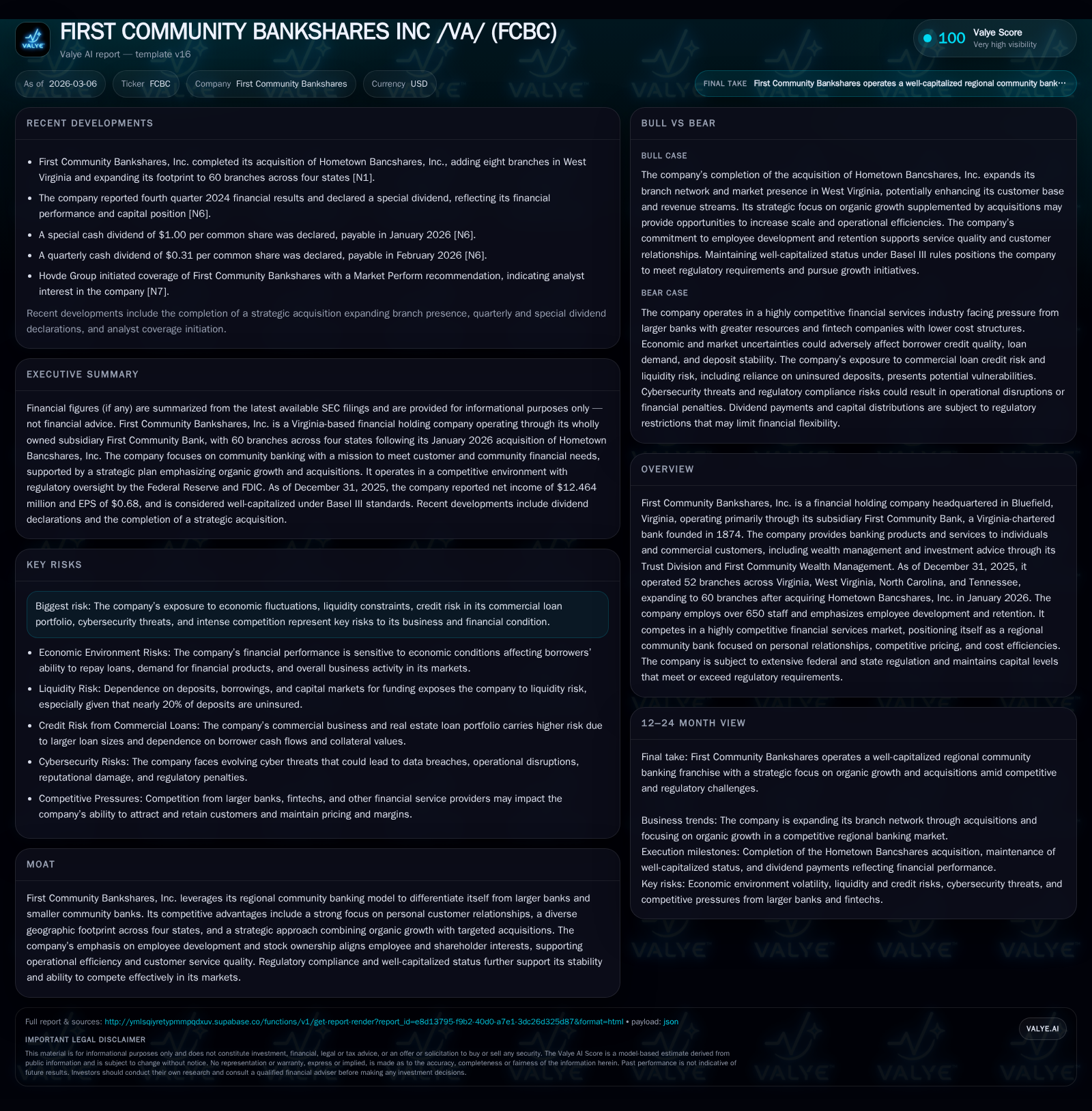

First Community Bankshares, Inc. (FCBC) completed the acquisition of Hometown Bancshares in January 2026, increasing its branch network from 52 to 60 across four states. Despite this strategic expansion, FY2025 net income declined by 4.4% year-over-year to $12.46 million, even as operating cash flow rose by nearly 9%. The company maintains a well-capitalized position under Basel III standards, balancing dividend payouts with modest share repurchases amid economic and regulatory uncertainties. FCBC’s future growth hinges on effectively integrating acquisitions, navigating competitive pressures in community banking markets across Virginia, West Virginia, North Carolina, and Tennessee, and managing credit and liquidity risks.

Solid Historical Earnings with Recent Profit Softening

First Community Bankshares reported FY2025 net income of $12.46 million, marking a decline of approximately 4.4% compared to $13.04 million in FY2024 [F1]. Notably, this contraction occurred despite an improvement in operating cash flow (CFO), which increased by roughly 8.7% year-over-year to $62.75 million in FY2025 from $57.74 million in FY2024 [F1]. This divergence suggests stable core cash-generating operations but challenges translating growth into bottom-line profitability.

The firm's equity base expanded significantly from $421.99 million in FY2022 to $500.55 million by end-2025 [F1], supporting continued operations amid economic fluctuations but exerting pressure on return metrics; the implied return on equity (ROE) stood near a modest 2.5% for FY2025 [F1]. Capital expenditures historically remain conservatively scaled relative to operating cash flows (latest available capex circa early-to-mid single-digit millions), underscoring cost discipline.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Net YoY |

|---|---|---|---|

| 2025 | 12 | 63 | -4.4% |

| 2024 | 13 | 58 | +10.7% |

| 2023 | 12 | 62 | -6.3% |

| 2022 | 13 | 59 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 61 | 2 | 2.5 |

| 2024 | 22 | 9 | 2.5 |

| 2023 | 21 | 23 | 2.3 |

| 2022 | 19 | 21 | 3.0 |

Source: SEC companyfacts cache [F1].

*Capex annual figures not consistently available for the recent years.

This data confirms a trajectory of relatively stable earnings generation punctuated by episodic declines and reflects a mature regional banking franchise balancing profitability pressures.

The Strategic Acquisition of Hometown Bancshares and Market Footprint Expansion

In January 2026 FCBC completed the acquisition of Hometown Bancshares Inc., the parent entity of Union Bank Inc., acquiring eight additional branches predominantly located in West Virginia [N1][S1][S7]. This deal lifted FCBC's branch network from 52 to a total of 60 locations spread across Virginia, West Virginia, North Carolina and Tennessee [S1][S7].

The acquisition aligns squarely with First Community's strategic playbook blending organic growth with targeted acquisitions to enhance market penetration and diversify geographic exposure — particularly strengthening its footprint in West Virginia where it previously held fewer branches [N1]. This move is strategic not only for physical expansion but also for scaling community banking assets amid intensifying competition.

An important nuance is Hometown Bancshares’ cultural fit: selection criteria emphasized target institutions closely resembling First Community’s operational ethos including similar employee experience levels and local community ties to ease integration risks [S1][S14]. However integration complexities may still challenge short-term earnings due to costs involved as flagged historically around acquisitions and potential asset quality uncertainties [S14].

Regional Banking in Four States — Competitive Pressures and Differentiation

Operating primarily as a regional community bank covering four southeastern states [S7], FCBC encounters stiff competition from a spectrum of financial players: large national banks wielding scale advantages; community banks vying aggressively for local loyalty; credit unions often underpriced due to tax-exempt status; and emerging fintech/wealthtech firms leveraging digital-first models [S5][S7].

Pricing pressures manifest through increasing adoption of low-fee or no-fee deposit accounts driven partly by fintech competition challenging traditional interest margins [S5]. In response FCBC leans heavily on relationship banking — cultivating personal customer contacts via branch networks and customized wealth management through its Trust Division [S1][N1]. Cost efficiencies gained via employee stock ownership initiatives further support competitive positioning by aligning staff incentives with shareholder value creation and service quality enhancement [S7].

However sustained deposit retention amidst rising digital disruption requires ongoing investment in technology platforms without diluting the personalized service that distinguishes regional community banks—a notable tension implicit but observable industry-wide.

Managing Credit, Liquidity, and Regulatory Risks Amid Economic Uncertainties

A prominent risk factor pertains to FCBC’s loan portfolio composition: commercial business and real estate loans constitute about two-thirds of outstanding assets ($1.53 billion), including commercial construction exposures that carry heightened credit risk due to project uncertainties [S15]. Concentrations expose the bank to localized economic downturns impacting borrower repayment capacity particularly given economic unevenness across regions like West Virginia with legacy coal/gas industry volatility [S25].

Liquidity management is complicated by almost one-fifth (19.54%) of deposits being uninsured as of December 31st 2025 — inherently more sensitive to withdrawal behavior during periods of systemic stress or depositor confidence erosion noted broadly within regional banking sectors post-2023 crisis events [S4][S26]. Maintaining sufficient high-quality liquid assets alongside access to borrowing facilities mitigates these vulnerabilities.

FCBC adheres stringently to regulatory capital requirements under Basel III frameworks ensuring well-capitalized status at quarter-end December 2025 with CET1 ratios comfortably above mandated minima [S6][S10][S11]. Nevertheless evolving regulatory landscapes impose ongoing compliance costs while constraining certain business activities such as dividend payouts contingent on capital adequacy thresholds enforced by federal regulators [S13][S16]. Cybersecurity threats also comprise material risk considering operational digital dependencies; breaches could inflict reputational harm as well as financial losses despite substantive preventive investments undertaken [S19][S24].

Capital Allocation: Dividends, Buybacks, and Maintaining Well-Capitalized Status

FCBC’s capital returns strategy is strongly skewed towards dividend distributions relative to share repurchases as evidenced by dividends paid hitting about $60.6 million in FY2025 versus buybacks at approximately $1.85 million—a ratio highlighting management preference for delivering income stability to shareholders over active capital return through market transactions [F1][S13][S16].

Equity has grown steadily from just under $422 million at FY2022 through $500+ million at FY2025 end supporting resilience against credit shocks or liquidity stresses while enabling measured headroom for organic growth or acquisition financing without jeopardizing regulatory capital ratios [F1][S6]. This conservative capitalization approach ensures compliance with prompt corrective action guidelines underscoring safety-and-soundness priorities central to effective bank governance.

Employee stock ownership plans play an integral complementary role by improving employee retention and aligning frontline performance with broader shareholder interests—an uncommon but potent feature sustaining operational rigor especially crucial during integration phases post acquisitions [S7].

What to Watch: Growth Catalysts and Risks Looking Ahead

Forward-looking growth will hinge on several critical vectors anchored in both documented company priorities and sector dynamics:

- The integration success of the Hometown Bancshares acquisition remains pivotal; seamless operational consolidation without significant disruption will be observable via expense trends and loan performance metrics over subsequent quarters [N1][S1][S14].

- Expansion within FCBC’s wealth management division presents upside potential leveraging cross-selling opportunities amid shifting demographics favoring advisory services [N1].

- Employee development initiatives signal management’s commitment to talent retention—key given intensified competition for skilled personnel compounded by ever-evolving compliance demands [S8][S7].

- Macroeconomic factors such as inflation persistence or energy price swings inherent within FCBC’s regional geographies could pressure loan demand or elevate nonperforming asset ratios particularly within commercial segments vulnerable to cost shocks or cyclical downturns [S25][S29].

- Regulatory changes remain an area of uncertainty—any tightening could restrict fee structures or lending parameters affecting revenue streams; vigilance on policy developments will be required alongside monitoring evolving marketplace competition from digitization accelerating fintech entrants aiming at deposit or lending market share capture [S5][S20].

Absent explicit forward guidance from management as per available filings [N#]/[S#], these considerations form analytical bellwethers rather than precise forecasts.

This analysis is based strictly on public financial disclosures and regulatory filings up to March 6th 2026 combined with recent news announcements relevant to First Community Bankshares Inc., without speculative extrapolation beyond verified data sources.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments