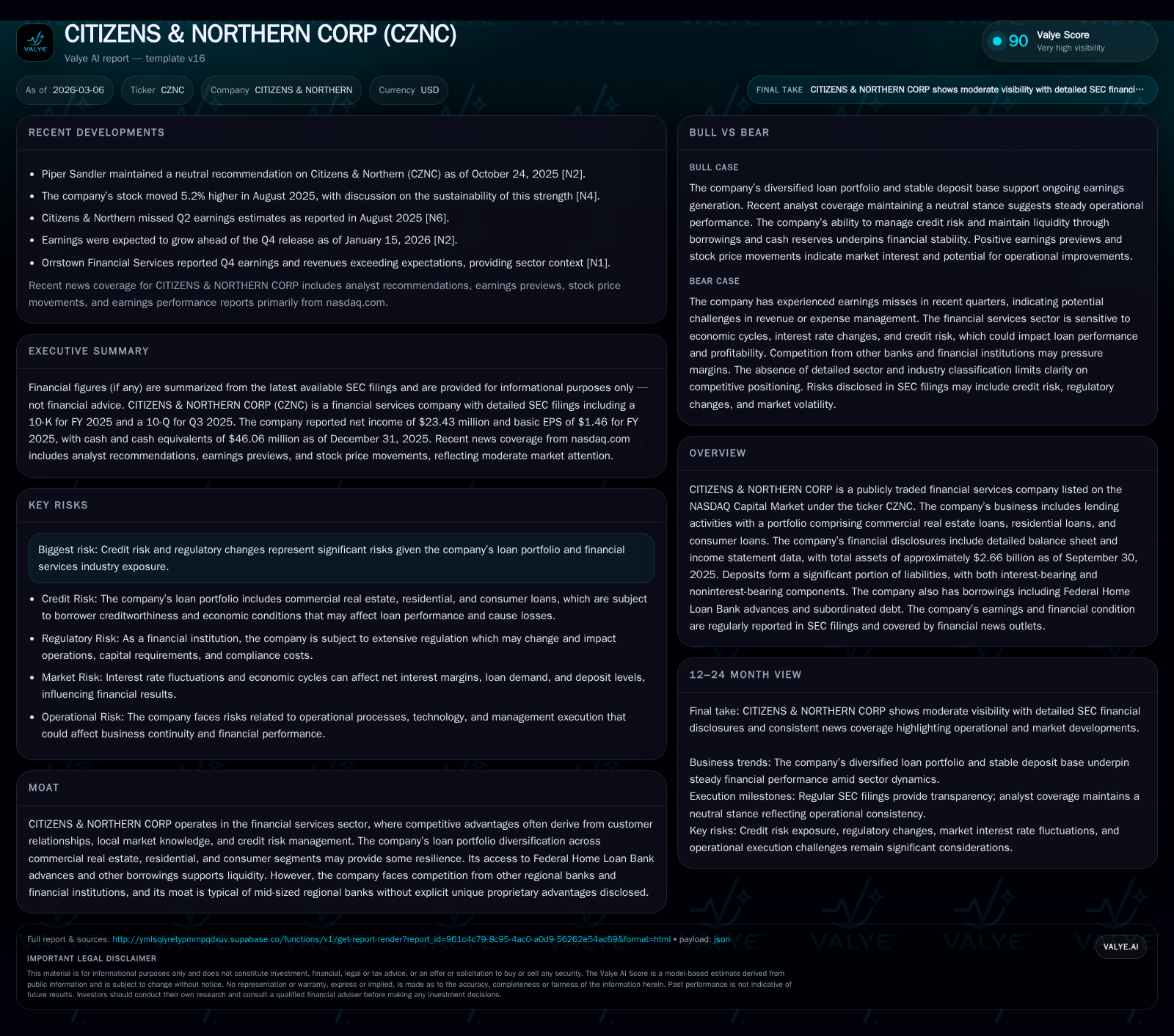

CITIZENS & NORTHERN CORP's Modest Earnings Decline Contrasts With Steady Equity Growth and Stable Loan Portfolio

The company showed resilience in loan portfolio diversification and capital management despite a slight net income dip in 2025.

CITIZENS & NORTHERN CORP (CZNC) reported a near 10% decline in net income in 2025 following several years of fluctuating earnings, largely driven by modest changes in operating performance and a stable but competitive regional banking environment. The firm maintains a diversified lending portfolio comprising commercial real estate, residential, and consumer loans, supporting revenue stability. Equity capital increased substantially, reflecting retained earnings growth and capital management strategies. Cash flow remains robust with consistent dividends paid, though buybacks have been minimal in recent years. Future growth will depend on managing credit and regulatory risks amid intensifying competition and potential macroeconomic headwinds.

Historical Performance and Financial Trends

CITIZENS & NORTHERN CORP has demonstrated financial resilience over the past four years despite varying earnings outcomes. Net income exhibited fluctuations: peaking at $26.6 million in 2022 before retreating to $23.4 million by 2025 [F1]. This decline equates to a -9.8% year-over-year drop from 2024's results. Operating cash flows followed a similar pattern, dipping by approximately 3.1% to $32.0 million in FY2025 from $33.0 million in the prior year [F1]. Capital expenditures show measured discipline with spending hovering near $1.9 million annually since 2024, down from $3.3 million in 2022.

Equity accumulation is a standout metric; shareholders' equity grew significantly by over 24% year-over-year to exceed $341 million at the end of 2025 [F1]. This reflects not only retained earnings but possibly conservative payout policies relative to earnings volatility.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 23 | 32 | 2 | -9.8% |

| 2024 | 26 | 33 | 2 | +7.5% |

| 2023 | 24 | 34 | 2 | -9.3% |

| 2022 | 27 | 35 | 3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 16 | 30 | 6.9 |

| 2024 | 16 | 31 | 9.4 |

| 2023 | 16 | 31 | 9.2 |

| 2022 | 16 | 31 | 10.7 |

Source: SEC companyfacts cache [F1].

Net income and cash flows declined modestly despite consistent dividend payments.

Business Model and Loan Portfolio

The company operates primarily as a regional financial services firm focusing on lending activities diversified across commercial real estate (both owner-occupied and non-owner-occupied), residential mortgages, and consumer loans [S1][S27]. This distribution provides some insulation against downturns concentrated in any single loan category.

As of September 30, 2025, total assets were approximately $2.66 billion [S15], funded mainly through deposits amounting to about $2.17 billion — split between roughly $508 million noninterest-bearing and $1.66 billion interest-bearing deposits [S15]. This deposit base underwrites lending operations while keeping funding costs manageable.

Borrowing facilities include Federal Home Loan Bank advances (around $133 million as of Q3 FY2025) with maturities staggered through late decade [S15][S5–S10], coupled with subordinated debt issued at a fixed rate of approximately 3.25%, redeemable at par by mid-2026 [S7]. These instruments enhance liquidity flexibility but introduce refinancing considerations around that redemption timeline.

Notably, the commercial real estate segment features both owner-occupied and non-owner-occupied loans with risk grading data highlighting largely well-performing credit exposures — minimal impaired or doubtful loans reported as of late [S12][S13]. Residential and consumer portfolios similarly show low delinquencies and special mention classifications.

Capital Allocation and Returns

CITIZENS & NORTHERN maintains stable dividend distributions exceeding $16 million per annum recently [F1] — roughly translating to returns supported by steady earnings despite recent declines.

Share repurchase programs have been virtually dormant post-2016 aside from minor activity many years ago [F1], reflecting either management’s cautious approach or prioritization of balance sheet strength over market-driven capital return strategies.

The approximate return on equity (ROE) for FY2025 can be derived as about 6.9% based on the reported net income versus shareholders’ equity figures [F1], indicating moderate profitability relative to invested capital.

Cash flow generation remains solid with free cash flow in the range of around $30 million after accounting for capex needs [F1]. This positions the company favorably for ongoing dividend support or opportunistic reinvestment.

Risks and Industry Environment

Risk factors articulated include typical pressures on credit quality inherent to regional banking amid shifting economic cycles [S4][S25]. Regulatory changes continue to be monitored closely by management given their complexity and potential compliance cost impacts.

Competitive dynamics stem from nearby regional banks jockeying for market share while adapting digital capabilities that influence customer acquisition costs and retention rates—a challenge common within the sector but without explicit moat-enhancing proprietary propositions disclosed for CITIZENS & NORTHERN .

Outlook Considerations

Explicit guidance was not observed within filings or news disclosures; however, observers should monitor quarterly results for developments concerning interest margin compressions or expansions tied to Federal Reserve rate actions affecting loan yields and funding costs.

Upcoming maturity events related to subordinated debt redemption present refinancing risks but also opportunities for cost optimization if market conditions are favorable.[S7]

Loan portfolio performance remains critical as macroeconomic uncertainties could trigger asset quality pressure especially if commercial real estate markets soften regionally.

Dividend sustainability should continue aligning with cash flow trends barring material shifts in credit losses or unexpected regulatory expenses.

Conclusion

CITIZENS & NORTHERN CORP embodies characteristics of a prudent regional lender managing a diverse loan book within a competitive environment marked by slow-growth net income trends yet expanding equity base. Operating cash flow resilience coupled with measured capital expenditure and steady shareholder payouts paint a picture of conservative stewardship amid evolving sector challenges.

Prospective watchers will want to focus on subtle loan performance metrics alongside capital structure refinements during coming periods to gauge whether the company can reverse recent profit moderation or maintain its current stability profile.

Disclaimer: This analysis is informational only and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments