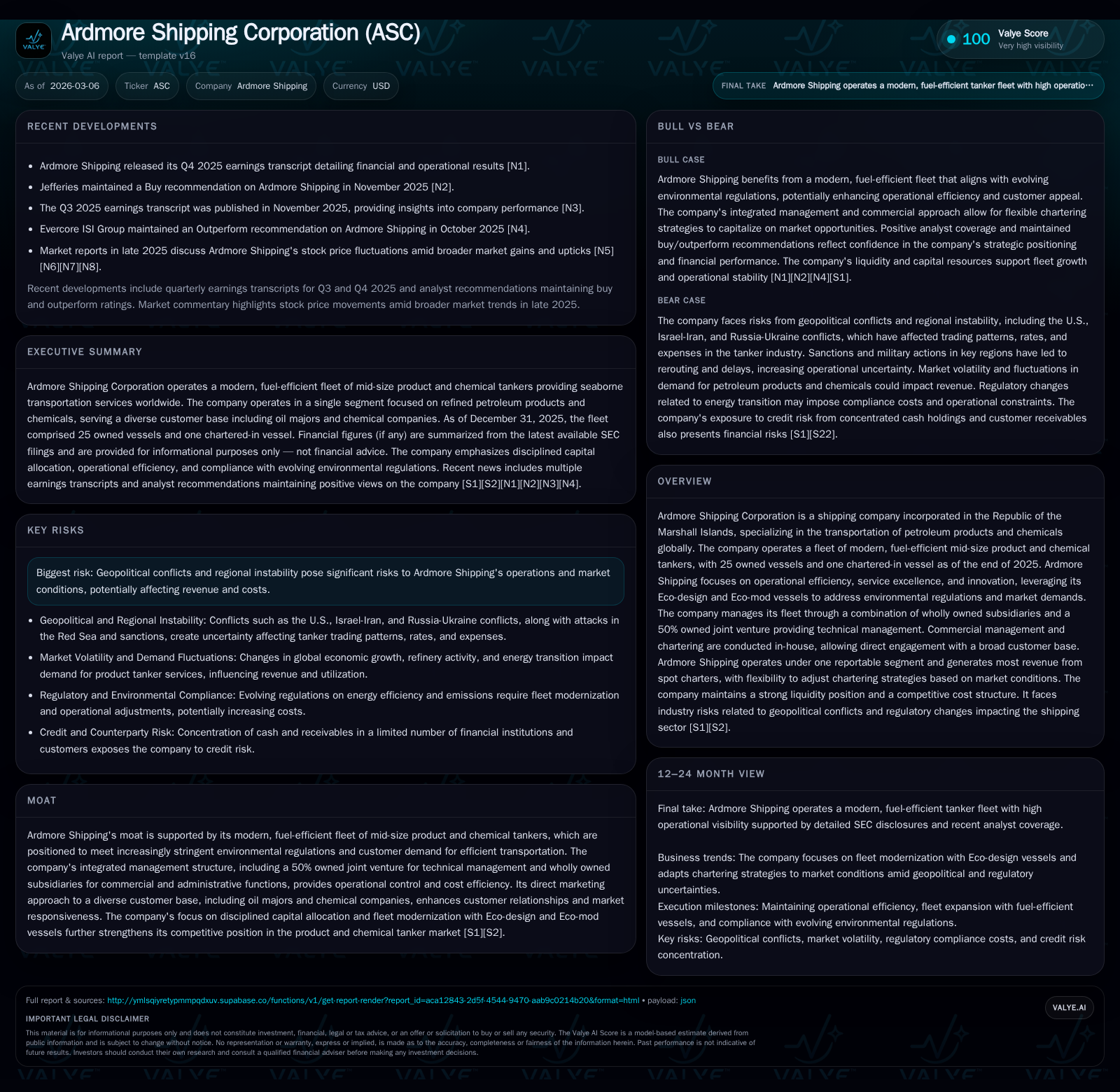

Ardmore Shipping Corp’s Strategic Execution in Mid-Size Chemical Tankers Elevates Competitive Edge

Ardmore Shipping balances recent revenue pressure with fleet innovation and tight operational control to reinforce its market foothold.

Ardmore Shipping Corporation, specializing in mid-size product and chemical tankers, experienced a notable revenue decline of 23.6% in 2025 yet maintained profitability supported by disciplined capital allocation and operational efficiencies. The company's modern, fuel-efficient fleet and integrated management structure underpin its competitive advantage amid geopolitical risks and tightening environmental regulations. Future growth hinges on navigating demand recovery, regulatory alignment, and leveraging sustainability-linked financing while maintaining strong liquidity and shareholder returns.

Company Background and Fleet Overview: Foundation for Operational Excellence

Ardmore Shipping Corporation operates as a specialized player in the seaborne transportation of petroleum products and chemicals globally through a fleet consisting primarily of mid-size product and chemical tankers. As of December 31, 2025, the company owned 25 vessels plus one chartered-in ship — all designed for fuel efficiency — boasting an average fleet age of roughly 10.9 years [S1][S16]. These modern vessels include configurations such as Eco-designs and Eco-mods specifically engineered to meet stringent environmental norms like IMO emission standards.

Structurally, Ardmore leverages a highly integrated management model comprising wholly owned subsidiaries responsible for commercial management (e.g., Ardmore Shipping (Asia) Pte. Limited, Ardmore Shipping (Americas) LLC) alongside a strategic joint venture partnership — owning 50% of Anglo Ardmore Ship Management Limited Pte. Ltd. (AASML) — dedicated to technical vessel management. This joint venture relationship enhances operational control over day-to-day technical upkeep without relinquishing governance while commercial chartering is handled entirely in-house, which facilitates direct engagement with a broad customer base including oil majors and chemical companies [S1][S2][S16][S20].

Operationally, mid-size tankers provide flexibility across diverse trade routes not bound to fixed schedules or ports, optimizing routing and cargo loading capabilities particularly to complex multi-grade or multi-port CPP trades where chemical handling expertise is vital [S1].

Historical Financial Trajectory: Revenue Decline Against Consistent Profitability

Between 2022 and 2025, Ardmore exhibited fluctuating top-line results characterized by cyclical industry influences. After peaking above $445 million in revenue during FY2022, top-line contracted sharply by approximately 23.6% to $310.2 million in FY2025 according to company filings [F1]. Despite this sizable contraction amid volatile tanker freight markets exacerbated by geopolitical tensions impacting global trade flows, Ardmore managed to preserve profitability with net income reported at $41.0 million for FY2025 — down from $133.0 million the prior year but still positive.

Operating cash flow also reflected this trend with CFO declining roughly 49.1% between FY2024 ($160.4 million) and FY2025 ($81.6 million) yet remaining robust relative to net income levels indicating maintained operational leverage [F1]. This pattern underscores effective cost management coupled with fleet utilization efficiency that partially cushions sharply reduced spot charter revenues common under tanker market downturns.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|

| 2025 | 310 | 41 | 82 | -23.6% | -69.2% |

| 2024 | 406 | 133 | 160 | +2.5% | +13.9% |

| 2023 | 396 | 117 | 160 | -11.2% | -15.6% |

| 2022 | 446 | 138 | 124 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 18 | 6.5 |

| 2024 | 18 | 21.9 |

| 2023 | 21.7 | |

| 2022 | 0 | 29.5 |

Source: SEC companyfacts cache [F1].

Note: Operating Income data unavailable beyond earlier periods.

Key Drivers of Past Growth: Spot Market Focus and Fleet Efficiency

Ardmore's earnings profile reflects significant exposure to spot charters which accounted for about $285 million of its total revenue in FY2025, well exceeding time charter revenues which contributed approximately $25 million [S12]. This reliance on the spot market instills earnings volatility aligned with freight rate cycles but also allows flexible deployment across shifting trade lanes particularly between clean petroleum products (CPP) and chemical cargos.

The company's strategy actively exploits synergies between CPP trades requiring multi-grade chemical expertise — such as simultaneous carriage of several petroleum/chemical grades — thus differentiating its service offering through specialization uncommon among some competitors restricted to single cargo types [S1][S4].

Fleet modernity underpins operational efficiency; fuel-efficient hull designs enable lower voyage costs versus aging competitors’ fleets which face higher bunker consumption especially relevant under new maritime emissions mandates like IMO’s carbon intensity regulations.

Market Environment and Geopolitical Risks: Navigating Volatility in Global Trade Flows

Ardmore faces persistent risk from geopolitical conflicts impacting key oil supply regions affecting tanker trade lanes directly or indirectly through increased tariffs, port fees, or navigational detours around hot spots such as the Red Sea due to Houthi rebel attacks or the volatile Strait of Hormuz area amid Iran-related tensions [S1][S20]. The ongoing Russia-Ukraine conflict has further entrenched uncertainty within global energy logistics.

These dynamics translate into cargo flow intermittency, re-routing costs, higher insurance premiums, and sporadic freight rates impacting tanker utilization patterns unpredictably particularly for medium-range operators reliant on global commodity flows rather than niche localized trades.

Fleet Modernization & Environmental Positioning: Eco-designs and Regulatory Alignment

Recognizing regulatory tightening globally on emissions from shipping vessels, Ardmore has prioritized fleet renewal emphasizing eco-efficient vessels encompassing advanced hull form designs (Eco-designs) alongside engine modifications (Eco-mods), enabling compliance with IMO emission targets ahead of many peers [S1][S2].

This investment not only reduces fuel consumption thereby lowering voyage costs but positions Ardmore favorably against expected future regulations such as EEXI (Energy Efficiency Existing Ship Index) norms set forth to enforce legacy vessel upgrades or phase-outs.

The company's capital expenditure on modernization aligns tightly with sustainability criteria required under its banking arrangements — including the recently refinanced $350 million sustainability-linked revolving credit facility — facilitating continued access to favorable financing terms contingent on maintaining environmental performance thresholds [S3][S13].

Commercial Strategy and Client Diversification: Leveraging Integrated Management

Ardmore maintains full control over its commercial operations through in-house chartering teams based primarily in Singapore and Delaware subsidiaries; no third-party blanket commercial managers are engaged for the core business segment ensuring nimble decision-making directly linked to customer relationships [S20].

Its clientele spans oil majors, national oil companies, chemical traders, chemical firms, and pooling providers—a diversified base mitigating counterparty concentration risk although some single charterers contribute over 10% annually illustrating importance of strong individual relationships [S4][S8].

The tightly integrated structure combining wholly owned subsidiaries for corporate functions alongside AASML JV for technical operations enhances cost efficiency while facilitating rapid adjustments in vessel deployment responding to volatile freight markets.

Capital Allocation and Shareholder Returns: Dividends, Buybacks, and Credit Facilities

Ardmore has exhibited prudent capital discipline balancing fleet expansion investments with shareholders’ expectations for returns via dividends and buybacks [F1][S13][S22]. During calendar year 2024, the company repurchased approximately $17.9 million worth of common stock at an average price near $11.49 per share demonstrating opportunistic capital return when share prices allowed value accretion.

Dividend distributions continue steadily; the Board declared quarterly cash dividends most recently at $0.09 per share payable in March 2026 reinforcing commitment despite recent revenue softness [N1][S22].

On the funding side, Ardmore refinanced prior facilities consolidating into a sizable $350 million sustainability-linked revolving credit facility due July 2031 bearing interest at SOFR plus approximately 1.8%, well below historic rates reflecting improved credit profile stabilized by its environmental initiatives [S3][S6].

As of year-end 2025 Ardmore’s drawn debt stood at about $127 million against undrawn capacity over $210 million providing ample liquidity headroom while complying fully with all loan covenants specifying minimum solvency (>30%), adjusted net worth (> $200 million), positive working capital requirements among others crucial for uninterrupted access to capital markets during cyclic downturns [F1][S10].

Estimated return on equity approximates a moderate ~6.5% signaling room for uplift contingent on market recovery given conservative leverage levels anchored by heavy equity base [$634 million equity at FY-end] [F1].

Future Growth Outlook: Capacity, Demand Signals, and Regulatory Constraints

Company guidance remains cautious amid uncertain macro backdrops; explicit forward visibility limited reflecting typical tanker market opacity from dynamic geopolitical pressures coupled with economic cycles affecting refined product demand globally [N1][S28].

Nonetheless growth avenues include selective fleet acquisitions maintaining eco-efficiency standards aligned with increasing regulatory scrutiny restricting older tonnage entry into many global ports.

Demand signals hinge upon global oil product consumption trends including substitution effects from energy transitions potentially impacting chemical tanker segments differently than crude or LNG shipping niches stimulating strategic positioning within overlapping multi-grade CPP/chemical markets.

Capital discipline likely persists given past emphasis; potential accretive vessel purchases will intertwine closely with sustainability conditionality embedded within credit facilities restricting uncalibrated expansion risking covenant breaches.

Financial Health and Liquidity Analysis: Strong Balance Sheet Amid Industry Cyclicality

At December 31, 2025 Ardenore Shipping reported strong liquidity evidenced by a current ratio of roughly 4.33 derived from current assets totaling about $112 million against current liabilities near $25 million reflecting substantial working capital buffers supportive during freight rate troughs or temporary cash flow mismatches [F1][S24].

Cash equivalents remain ample even accounting for operating cycle needs facilitating uninterrupted capex programs focused on drydockings plus technical upgrades essential for compliance under IMO frameworks.

Debt maturities are weighted toward long-term revolving facilities minimizing near-term refinancing risks; combined with low gross leverage relative to fleet value sizes this positioning affords resilience against sudden downturn shocks prevalent in tanker sectors vulnerable to geopolitical shocks or regional disruptions on critical trade lanes discussed previously.

DISCLAIMER: This report is for informational purposes only reflecting data available up to March 6, 2026; it does not constitute investment advice or recommendations regarding purchase or sale of securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments