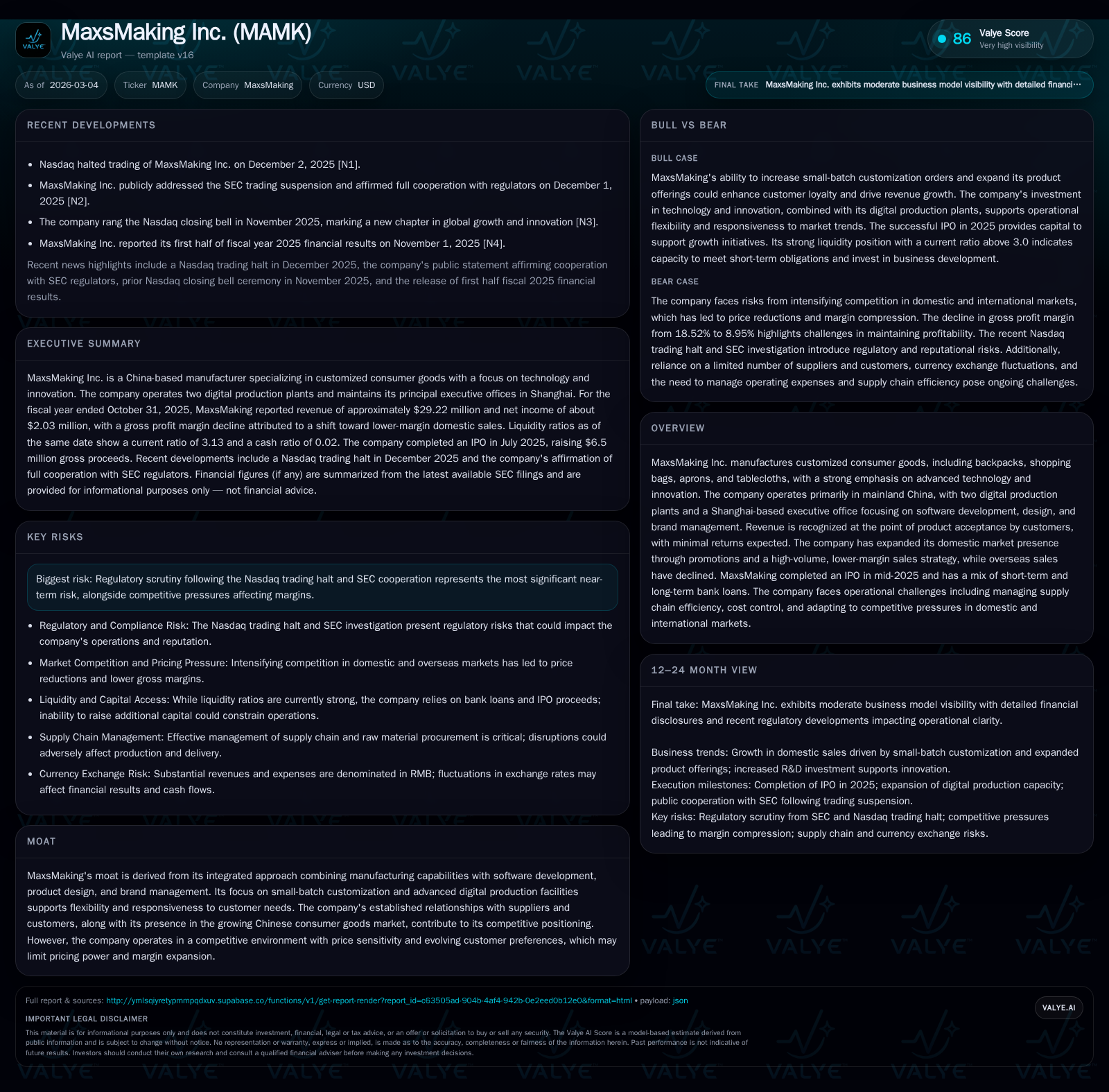

Evaluating MaxsMaking’s Custom Manufacturing Business Model and Financial Health

An assessment of MaxsMaking’s integrated manufacturing-software model reveals growth trajectories tempered by margin pressures and regulatory risks.

MaxsMaking Inc. has pursued a growth strategy reliant on its unique combination of digital manufacturing and software-driven customization, which has driven notable revenue increases following its mid-2025 IPO. However, the company faces margin compression amid an aggressive low-price domestic push and declining overseas sales. Its capital structure incorporates a mix of short- and long-term bank loans complemented by IPO proceeds, yet cash flows remain negative due to working capital demands and operating expenses. Regulatory scrutiny following a Nasdaq suspension presents material near-term uncertainty. Investors should focus on operational execution in small-batch customization, supply chain management improvements, and the evolving regulatory landscape.

MaxsMaking’s Growth Journey: From Inception to IPO

MaxsMaking Inc., founded in 2007 under the leadership of Xiaozhong Lin and Xuefen Zhang, has developed into an integrated manufacturer of customized consumer goods. Operating primarily through two digital production plants located in Yiwu, Zhejiang Province, and Zhumadian, Henan Province, the company maintains an aggregate floor space of approximately 4,192 square meters dedicated to manufacturing operations [S1]. Its Shanghai headquarters concentrates on software development, product design, and brand management—highlighting an uncommon vertical integration blending technology with physical production.

Historically, MaxsMaking recognized revenue at product acceptance by customers with minimal returns due to quality assurances embedded in their processes [S15]. Prior to the July 2025 IPO which raised approximately $6.5 million gross proceeds [S20], the company experienced fluctuating financial results closely tied to order volumes in small-batch customized goods versus larger batch orders [F1], [S1]. The IPO was a pivotal event intended to bolster liquidity for expansion investments particularly in strengthening market reach within mainland China.

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

Note: Capex figure limited to disclosed amounts; operating income figures derived from financial statements [F1].

Wholesale vs. Small-Batch Customization: Revenue Drivers and Margin Impact

MaxsMaking's competitive moat centers on its capacity for small-batch customization powered by advanced digital plants paired with software tools allowing nimble customer-specific product configurations [S1]. This capability supports flexibility responding swiftly to changing market demands—a critical factor given the volatility in order volumes from varied customers.

However, this small-batch focus entails tradeoffs in unit economics versus bulk wholesale orders which historically yielded better margins. As detailed by management discussion [S4], the shift towards a high-volume but lower-margin domestic sales strategy compressed overall gross profitability despite higher top-line growth outcomes.

The company's revenue recognition practices align with ASC 606 standards recognizing sales upon delivery acceptance [S19], supporting transparency but also highlighting limited margin leverage when pushing volumes under price-sensitive conditions.

Geographic Sales Trends: Domestic Expansion Meets Overseas Decline

Fiscal year 2025 marked a clear inflection where MaxsMaking's domestic sales surged by over $9 million or approximately +54%, constituting more than 90% of total revenues at $26.64 million [S8], [S10]. This expansion was driven by intensified promotions during Chinese shopping festivals and strategic client referrals extending the customer base.

Conversely, international sales shrunk markedly with Asia ex-China down nearly 60%, Europe declining almost 30%, reflecting weak demand dynamics abroad compounded by South Asian competitors aggressively pricing into North American markets [S4],[S8]. These geographic shifts negatively impacted gross margins given that overseas sales traditionally generated higher profits.

Supply Chain Management Amid Cost Inflation and Competitive Pricing

The company’s operating model depends critically on reliable sourcing of raw materials and timely fulfillment aligning with dynamic small-batch scheduling [S1],[S9]. Recent periods saw raw material costs inflation coupled with supply chain disruptions causing inventory buildup as reflected in working capital increases of nearly $5 million year-over-year [S12].

To maintain competitiveness against price-sensitive customers domestically and cost-efficient rivals internationally, MaxsMaking reduced pricing leading to further gross margin contraction—from an already thin ~18% margin in 2024 down below 9% in fiscal year 2025 [S4],[F1].

Capital Structure and Liquidity: Debt Mix, Bank Loans, and IPO Proceeds

As of October 31, 2025 MaxsMaking's balance sheet reveals short-term bank loans totaling approximately $1.95 million split between Ningbo Bank (3.4-4%) and Zhejiang Yiwu Rural Commercial Bank (5%) plus long-term loans aggregating ~$2.3 million sourced from Zhejiang Yiwu Rural Commercial Bank (3.5%), Bank of China (2.9%), and China Construction Bank (3.9%) [S3],[S11]. Additional non-interest-bearing third-party loans amount to roughly $0.21 million.

Cash reserves stood at a minimal $122 thousand post-IPO indicating constrained liquidity despite equity infusion [F1],[S12]. Total working capital improved from $9.1 million to ~$14.65 million benefiting short-term operational funding but pressure remains due to high inventory levels and receivables nearing $10 million [F1],[S21].

The IPO provided $6.5 million gross proceeds after deducting underwriting fees signaling intent to strengthen capital for sustained growth initiatives [S20]. Nonetheless elevated debt servicing requirements coupled with operational cash outflows (-$5+ million CFO) limit financial flexibility currently.

Profitability Snapshot: Gross Margins, Operating Income, and Free Cash Flow

MaxsMaking’s financial profile demonstrates revenue growth juxtaposed against considerable margin erosion culminating in near breakeven net income ($2K USD) despite revenues jumping over $29 million FY25 vs FY24 levels over $21 million [F1],[S4]. Key profitability metrics are summarized below:

| Fiscal Year | Revenue (USD million) | Operating Income (USD thousand) | Net Income (USD thousand) | Cash Flow from Operations (USD million) | Capex (USD million) |

|---|---|---|---|---|---|

| 2023 | 21.43 | N/A | N/A | (0.60) | N/A |

| 2024 | 21.43 | N/A | N/A | (3.04) | N/A |

| 2025 | 29.22 | 0.10 | 0.002 | (5.29) | 0.06 |

Operating expenses rose sharply (+42%) driven largely by a doubling of G&A costs including IPO-related professional fees plus allowance for doubtful accounts increasing provisions as receivables grew [S6],[S13]. Selling expenses decreased as headcount reductions partially offset freight cost reductions.[S6]

Free cash flow is persistently negative due to working capital consumption amid expanding inventory purchases necessary for customization demand surges despite modest capex investments focused on plant technology upkeep rather than expansion [F1],[S14].

Future Outlook: Growth Opportunities Versus Regulatory and Market Risks

While MaxsMaking seeks future gains through deepening domestic penetration leveraging its proprietary digital fabrication strengths and software-enabled design innovation pipeline [S1], significant challenges loom.

Regulatory concerns dominate risk considerations: recent SEC enforcement actions precipitated a ten-day Nasdaq trading suspension threatening delisting risks pending investigation outcomes coordinated with company cooperation efforts [S27]. Such uncertainties constrain access to U.S.-based capital markets affecting funding options going forward.

Competitive market headwinds persist both domestically in price-sensitive categories and abroad where South Asian firms continue undercutting prices undermining margin recovery potentials.[S4],[S8]

Operationally, the need for supply chain optimization remains crucial given current inefficiencies observed in working capital strains that depress free cash generation capabilities.

Capital Allocation Philosophy: Dividends, Buybacks, and Operating Leverage

MaxsMaking maintains no dividend or share repurchase programs as per latest filings reflecting prudent reinvestment prioritization amid capital constraints post-IPO [S17],[S20].

The company emphasizes operating leverage gains through scaling production efficiencies as business volume grows but achieved so far at cost increases associated with staff expansions especially within R&D functions aimed at process digitization improvements [S6],[S9].

ROE remains effectively zero consistent with minimal net income relative to equity base underscoring nascent profitability status as reported for FY25 while management focuses on expense control initiatives balancing growth investments [F1],[S25].

What to Watch: Key Milestones and Metrics for Investors

Absent formal forward guidance or public milestone commitments in filings or news releases, investors should monitor:

- Quarterly order volume trends particularly within small-batch customized segments which define core differentiation value proposition;

- Progress reports on supply chain initiatives aimed at inventory reduction and improving working capital turns;

- Domestic market share evolution amid ongoing promotional campaigns versus encroaching competitor pricing pressures;

- Developments related to SEC investigations including updates on Nasdaq listing status given implications for capital access;

- Operating expense trajectories focusing on R&D efficiency vs G&A cost absorption post-IPO professional fee normalization.

Understanding these dynamics will be critical as MaxsMaking attempts balancing innovation-led service differentiation against intense market competition combined with regulatory complexities constraining financial maneuverability.

This analysis reflects information derived from publicly filed SEC documents dated through March 4, 2026 ([S1]-[S27]), along with numerical data consolidated from the company's annual report snapshot ([F1]). It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments