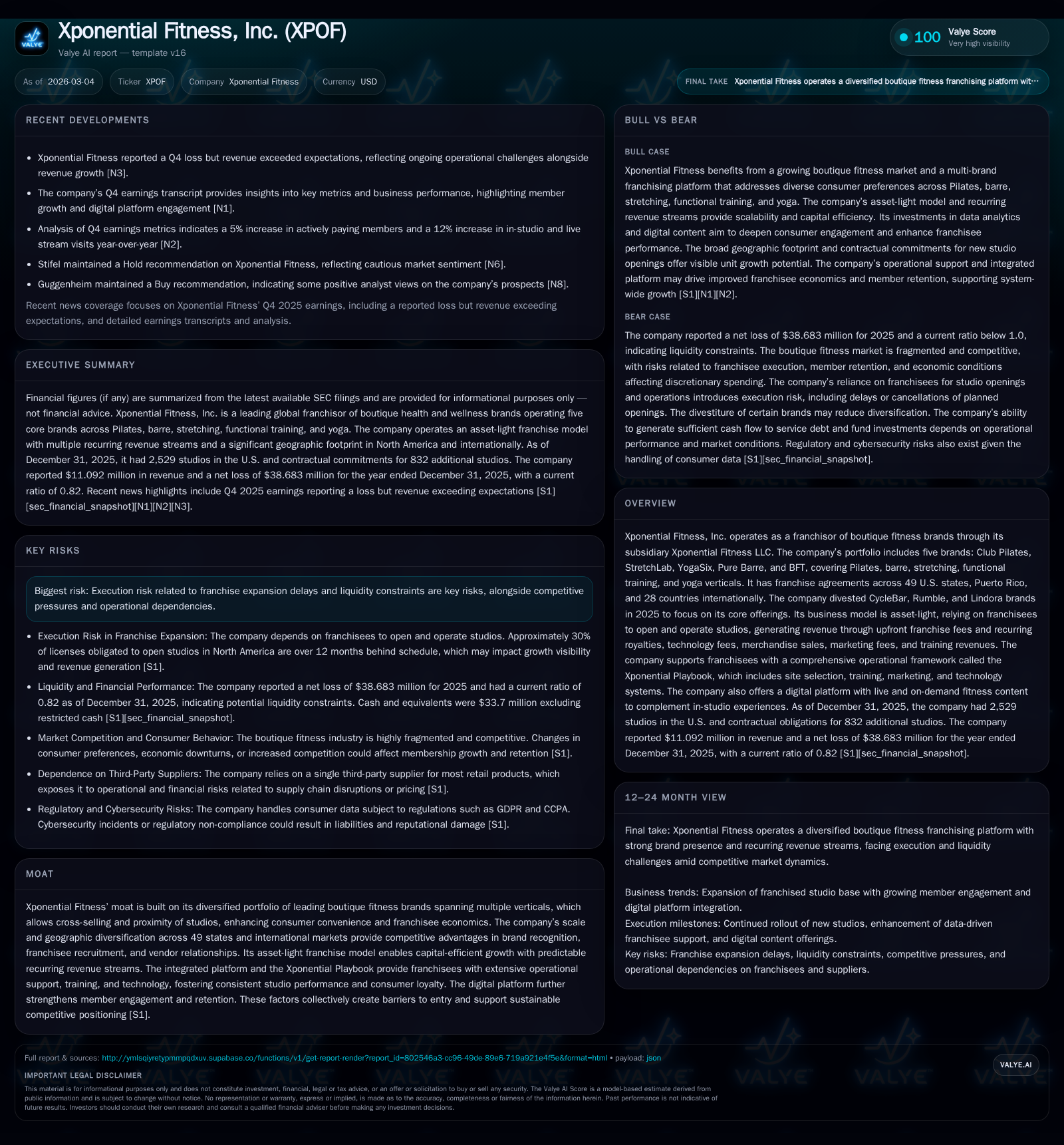

Xponential Fitness’s Strategic Refocus and Financial Resurgence in 2025

Xponential Fitness narrowed its brand portfolio in 2025, sparking an operating income turnaround despite lingering revenue headwinds.

In 2025, Xponential Fitness undertook a significant strategic realignment by divesting non-core boutique fitness brands CycleBar, Rumble, and Lindora to sharpen focus on five flagship brands across Pilates, barre, stretching, functional training, and yoga. This portfolio pruning supported operational efficiencies through its integrated franchise playbook and an asset-light model reliant on franchisees. While revenue declined 20.7% year over year due to these divestitures and delayed studio openings, operating income swung from a loss to a $19.8 million profit. However, net losses persisted at $38.7 million amid elevated costs and legal provisions. The company generated robust operating cash flow exceeding capex by $24.7 million, underpinning liquidity despite significant debt obligations capped by a $525 million term loan. Going forward, cautious expansion amid franchisee delays and regulatory scrutiny present key risks to watch.

Evolution of a Boutique Fitness Portfolio: From Expansion to Refocus

Xponential Fitness entered 2025 with an expansive boutique fitness portfolio that included seven brands spanning diverse verticals such as Pilates (Club Pilates), barre (Pure Barre), stretching (StretchLab), functional training (BFT), yoga (YogaSix), indoor cycling (CycleBar), boxing (Rumble), and medically guided metabolic clinics (Lindora). However, the company strategically restructured during 2025 by divesting CycleBar and Rumble in July and Lindora in September [S1][N3]. This move intentionally sharpened Xponential's concentration on five core brands representing its strongest verticals: Club Pilates, StretchLab, YogaSix, Pure Barre, and BFT.

This pruning aligned with the asset-light franchisor business model where growth depends on franchise agreements rather than capital-intensive owned studios. Xponential's operational framework—the Xponential Playbook—provides franchisees comprehensive support including site selection expertise, training programs, marketing assistance, and technology infrastructure [S1]. Such scale combined with cross-brand proximity enhances franchisee unit economics by facilitating cross-selling opportunities and optimizing shared resources across verticals within local markets. Furthermore, the geographic footprint covering all 49 U.S. states plus Puerto Rico and 28 countries internationally strengthens brand recognition and vendor negotiating power [S1].

By narrowing focus, Xponential aims for higher operational efficiency and consistent studio performance through deepened investment in its integrated platform rather than diluting resources across multiple niche ventures.

2025 Financial Performance: Recovery Trend with Revenue Headwinds

Financial results reflected both the strategic divestitures as well as lingering execution challenges. Reported total revenue for FY2025 fell to approximately $11.1 million—a sizable decline of roughly 20.7% compared to $14.0 million in FY2024 [F1]. This drop corresponds mainly to the divested brands’ removal from the consolidated base plus slower-than-expected new studio openings attributable to site acquisition hurdles faced by some franchisees [N3][S1].

Despite this top-line contraction, operating income rebounded strongly from a significant loss of $53.6 million in FY2024 to a positive $19.8 million in FY2025 representing a remarkable 137% year-over-year improvement [F1]. This inflection owed chiefly to cost reductions stemming from streamlining brand portfolios alongside restructuring-related savings realized during the period [N3]. Operating expenses contracted significantly even as sales fell because divested brands carried outsized operating costs relative to their contribution.

Net income remained negative but improved materially from a loss of $67.7 million in FY2024 to approximately -$38.7 million in FY2025—a year-over-year enhancement exceeding 40% [F1]. The persistence of net losses relates largely to non-cash impairment charges recorded on goodwill and intangible assets attached to past acquisitions as well as legal reserves tied to ongoing governmental investigations into franchise disclosure compliance [S1][S8].

Cash flows from operations surfaced strongly at $28.3 million for FY2025—more than doubling the prior year’s figure—reflecting improved profitability adjustments plus working capital movements stabilizing after prior disruption [F1][S6]. Capital expenditures shrank modestly by about 24%, totaling roughly $3.58 million as Xponential exercised discipline over growth investments post-divestiture [F1]. After accounting for capex needs, free cash flow generation stood near $24.7 million underscoring tangible recovery momentum despite residual challenges.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 11 | -39 | 28 | 20 | -20.7% | +42.8% |

| 2024 | 14 | -68 | 12 | -54 | +4.4% | -7392.6% |

| 2023 | 13 | -1 | 35 | 40 | +4.5% | -146.8% |

| 2022 | 13 | 2 | 52 | 15 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | 25 | 14.4 |

| 2024 | 0 | 7 | 31.2 |

| 2023 | 50 | 28 | 0.7 |

| 2022 | 43 | -1.2 |

Source: SEC companyfacts cache [F1].

Table: Xponential Fitness Historical Financial Summary from FY2022–FY2025 [F1]

Franchise Economics and Operational Drivers Behind Past Growth

Xponential’s revenue base largely derives from upfront franchise fees upon studio license grants alongside recurring royalties tied to franchisee sales performance plus ancillary revenues encompassing marketing contributions, technology platform fees, merchandise sales commissions, and training services rendered under its one-stop integrated platform [S1]. Its multi-brand approach lends itself well to higher aggregate lead flow facilitating more cost-effective franchise recruitments while also securing ongoing development from existing partners expanding additional units.

Unit economics are structured so initial franchisee investments average around $554 thousand mostly funding physical studio build-outs between roughly 1,500 to 2,500 square feet tailored by brand vertical demand profiles—for instance Pure Barre studios optimizing ballet barre setup versus Club Pilates requiring specialized reformer equipment [S22]. Through this format size optimization combined with proximity-driven cluster economics where multiple branded studios concentrate geographically sharing overhead lines such as management staffing or local marketing spend Xponential franchises can boost profitability.

Studio count remains a critical KPI influencing royalty flow streams; however approximately thirty percent of licensed studios contracted for opening remain significantly overdue beyond typical development timelines—particularly impacted during transitions or economic downturn periods where site selection becomes restricted or construction financing tightens [S22][N2]. Such delays throttle immediate revenue growth potential rendering earnings somewhat lumpy despite contractual commitments.

Assessing Future Growth Pathways and Market Penetration Challenges

Looking forward into 2026+, management maintains ambitions to grow physical footprint via greenfield expansion focusing on North American markets where penetration remains below saturation plus selective international territories leveraging master franchise partners already embedded per existing agreements across twenty-eight countries [N1][S1]. Yet realization of these ambitions is contingent on overcoming execution risks primarily:

- Securing suitable real estate sites which has tightened amid inflationary pressures;

- Resolving liquidity constraints amongst franchisees impacting their ability to complete build-outs;

- Fending off intensifying competition both from legacy gym chains adopting boutique concepts plus digitally native fitness platforms expanding hybrid models;

- Navigating regulatory complexities particularly around pending FTC investigations mandating disclosure compliance improvements that could temporarily restrict new license issuances or renewal approvals [S8].

Brand reputation stewardship will be equally vital as consumer preferences evolve towards integrated wellness experiences demanding not just workouts but holistic health offerings potentially requiring future service innovation pipelines beyond current modalities.

Capital Structure, Liquidity, and Their Impact on Strategic Flexibility

As of December 31, 2025, Xponential held total indebtedness comprising a $525 million term loan facility maturing December 2030 accompanied by a smaller revolving credit line of up to $25 million for operational flexibility [S4][S6][S28]. The debt is secured via first priority liens on substantially all assets with covenants notably including total net leverage ratio ceilings periodically tested starting Q1 2026 onward with compliance reported currently satisfactory [S4][S25].

The covenant package restricts incremental debt incurrence plus imposes limitations on asset sales outside ordinary course along with bans on dividend payments or share repurchases absent lender consent thus constraining discretionary capital deployment avenues [S6][S14][S25]. Future breaches would trigger defaults risking accelerated repayment demands adversely affecting operational liquidity.

Cash balances including restricted funds approximated $33.7 million excluding earmarked marketing funds while operating cash flow generation outpaced capital expenditures offering projected runway coverage for at least twelve months under current assumptions per management commentary [S4][S6]. Incremental capital needs arising from acquisitions or digital platform investments could necessitate external financing subject to market conditions given existing leverage profiles.

Return Metrics and Capital Allocation: Dividends, Buybacks, and Free Cash Flow

Equity remains deeply negative nearing -$269 million reflecting cumulative net losses augmented by impairment charges primarily linked to legacy intangible assets from past acquisitions; consequently traditional return metrics such as ROE are distorted yet imply an approximate positive ~14% when assessed against latest net income figures accounting for equity deficits cautiously [F1].

Importantly free cash flow calculated conservatively as operating cash flow minus capex totaled roughly $24.7 million in FY2025 indicating solid internal cash sustainability despite net loss positions [F1][S19]. Capital allocation activities ceased share repurchases since FY2023 following aggressive buyback campaigns before pivoting towards deleveraging efforts inclusive of convertible preferred stock redemptions fully executed during fiscal periods leading up to the latest report cycle [F1][S19][S24]. No dividends have been declared reflecting balance sheet preservation priorities.

Key Risks: Franchise Execution, Competition, and Regulatory Environment

Several material risks bear continued monitoring:

- Variability in franchisee financial health affects royalty inflows unpredictably;

- Delays or failures in site selection slow network expansion limiting scalable recurring fee accretion;

- Investigations by U.S Federal agencies including the FTC concerning disclosure compliance could limit franchising activities or result in fines impacting financials negatively [S8];

- Intensifying competitive pressures within boutique fitness space especially from tech-enabled at-home fitness solutions might erode customer retention;

- Elevated debt levels present refinancing risk amid rising interest rate environments restricting maneuverability if cash flow targets are missed leading potentially to covenant breaches triggering default consequences [S25];

- Operational dependencies include reliance on third-party providers for information systems integral to centralized operations amplifying risk should disruptions occur.

Legal proceedings including securities class action suits add layers of litigation uncertainties detracting management focus away from strategic growth imperatives impacting stockholder confidence [S13][S17].

What to Watch: Indicators for Milestones and Trajectory Validation

Looking ahead analysts should track several metrics indicative of trajectory sustainability:

- Pace of new studio openings vis-à-vis contractual commitments serving as bellwether for franchise execution efficacy;

- Same-store sales trends informing underlying brand health especially within core verticals;

- Digital platform adoption rates enhancing member engagement underpinning retention mechanisms;

- Debt covenant compliance reports starting March quarter revealing financial discipline adherence;

- Developments around FTC consent order finalization influencing regulatory overhang removal timing;

- Operating leverage efficiency gains reflecting how integrated platform investments mature into margin expansions;

- Management changes or shifts signaling strategic recalibrations responsive to competitive dynamics.

Such updates will provide early visibility into whether financial improvements evidenced in FY2025 can be translated into consistent profitable growth bridging past challenges toward long-term stability.

This analysis relies solely on information available through official SEC filings dated March 4th, 2026 ([F1],[S1]-[S29]) and recent news transcripts ([N1]-[N3]). It does not constitute investment advice but serves as an informed synthesis valuable for professional understanding of Xponential Fitness’s business transformation phases and financial positioning as of early 2026.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments