CBL & Associates Properties: Unpacking the Turnaround of a Retail REIT Giant

CBL's strategic portfolio optimization, integrated operations, and capital restructuring underpin its financial resurgence amid retail sector shifts.

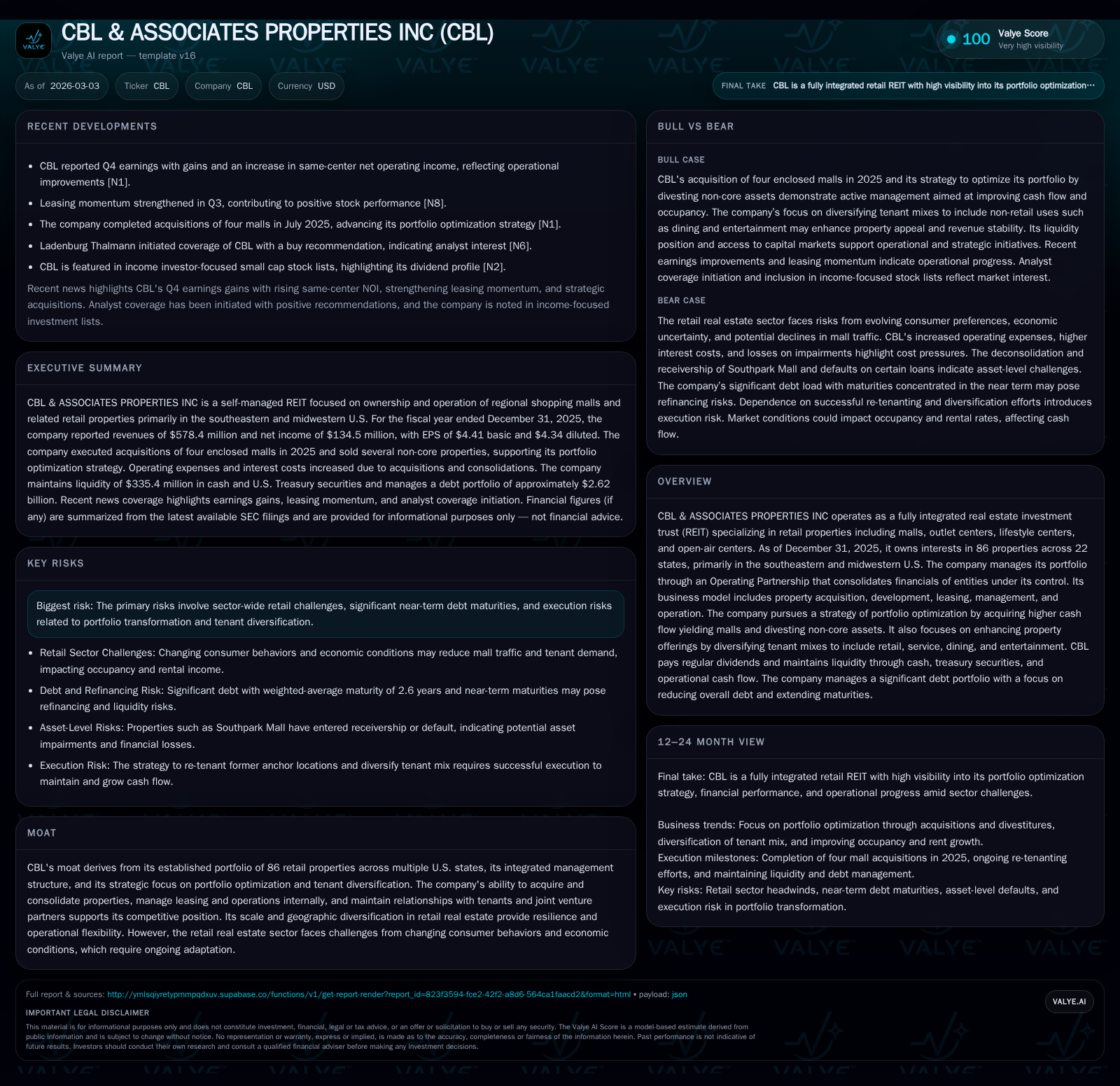

CBL & Associates Properties has reversed multi-year losses into robust profitability in 2025, driven by a targeted acquisition strategy and operational efficiency. The company's focus on portfolio optimization through acquiring higher-yield enclosed malls and divesting non-core open-air centers improves occupancy and cash flow. A disciplined capital management approach, including debt maturity extensions and dividend increases, supports shareholder returns while preparing for retail real estate headwinds. Going forward, monitoring lease-up progress and refinancing outcomes will be crucial to assess sustainability of growth.

Financial Revival: Tracing CBL's Recent Growth Trajectory

CBL & Associates Properties' financial turnaround in FY2025 is striking when contrasted against recent years of volatility. Total revenue climbed 12.2% year-over-year to approximately $578 million, fueled primarily by increased rental revenues and gains from property sales [F1][S1]. Net income more than doubled (+130.6%) to about $136 million, reflecting not only top-line strength but also substantial equity earnings and gains on sales—$57.6 million higher compared to the prior year [S1]. Operating cash flow (CFO) improved by 23.5%, reaching nearly $250 million, bolstering internal liquidity [F1]. This robust cash generation supports ongoing capital requirements and dividends.

Nevertheless, expenses increased across several categories: depreciation & amortization rose $24.6 million, interest costs were up $21.5 million due to refinancings at higher rates, and property operating costs increased by $29.2 million amidst portfolio expansion [S1]. These cost pressures have yet to offset operational gains fully but underscore the importance of ongoing portfolio discipline.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|

| 2025 | 578 | 136 | 250 | +12.2% | +130.6% |

| 2024 | 516 | 59 | 202 | -3.7% | +800.9% |

| 2023 | 535 | 7 | 184 | -4.9% | +107.0% |

| 2022 | 563 | -93 | 208 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 77 | 18 | 36.3 |

| 2024 | 50 | 36 | 18.2 |

| 2023 | 118 | 1 | 1.9 |

| 2022 | 24 | -25.2 |

Source: SEC companyfacts cache [F1].

Table: Historical Financial Summary for CBL & Associates Properties Inc (2019–2025) highlighting recent recovery and capital returns [F1].

Portfolio Optimization: Strategic Acquisitions and Divestitures Driving Occupancy

Central to CBL's turnaround is its deliberate portfolio optimization: focusing on acquiring higher cash-flow yielding enclosed malls while divesting non-core open-air properties with lower returns or higher volatility [S1]. The July 2025 acquisition of four enclosed malls—Ashland Town Center (KY), Mesa Mall (CO), Paddock Mall (FL), and Southgate Mall (MT)—represents a material shift utilizing proceeds generated from recent open-air center sales like The Promenade and Fremaux Town Center [S1]. This selective capital recycling aims at improving occupancy profiles and enhancing net operating income (NOI).

Same-center mall occupancy remained stable at around 88.6%, while open-air centers held above 90%, reflecting effective asset management despite broader sector headwinds [S28]. The acquired malls contribute geographic diversification spanning primarily southeastern and midwestern U.S., consistent with CBL’s footprint.

These moves exemplify a recycling of capital characteristic of mature REITs seeking yield stability rather than aggressive expansion—a prudent response given evolving tenant demand patterns.

Integrated Operations and Tenant Mix Diversification as Competitive Advantages

CBL operates an integrated platform encompassing ownership, leasing, management, and redevelopment—eschewing reliance on external managers [S1]. This vertical integration enables nimble re-tenanting strategies: converting vacated anchor locations into diverse uses including service providers, dining establishments, entertainment venues, alongside traditional retail tenants.

Such diversification mitigates concentration risk inherent in anchor-heavy shopping malls amid ongoing closures across department stores nationally. Inline tenant occupancy costs held steady near historical norms (~10.6%), underscoring sustainable tenant economics even amidst market challenges [S28].

Moreover, CBL leverages re-tenanting as a tactical tool to stabilize rents and maintain foot traffic metrics critical for overall property performance—a key competitive advantage within retail REIT operations.

Capital Structure Reshaping: Managing Debt Maturities and Interest Costs

CBL’s capital structure as of December 31, 2025 features approximately $2.62 billion of pro rata debt ($335 million unrestricted liquidity buffer), predominantly secured by property-level assets with roughly 95% classified as non-recourse loans limiting corporate liability exposure [S4][S8]. Fixed-rate debt amounts to about $1.87 billion with a weighted average rate near 5.51%, balancing fixed cost certainty against rising interest rate environment [S7]. Variable-rate debt composes approximately 28.7% of total borrowings at a blended rate around 7%, reflecting timing differences in refinancings.

The weighted average maturity extends modestly beyond prior year levels (~2.6 years), reflecting active management through extensions like those on secured term loans due in November 2026 that carry extension options under certain conditions [S10][S17][S26]. These efforts reduce rollover risks amid uncertain credit markets.

Figures excluding deferred financing costs show a net mortgage indebtedness decline from prior years owing to asset sales coupled with refinancing activity aimed at lowering borrowing costs whilst preserving balance sheet flexibility.

Notable challenges include defaulted loans on select properties such as Southpark Mall placed into receivership July 2025 and leases maturing on key assets requiring refinancing or disposition decisions shortly [S17][S26][N1]. Liquidity reserves alleviate immediate pressures but necessitate monitoring going forward.

Dividend Policy and Shareholder Returns in a Transitional Phase

Reflecting enhanced cash flow generation, CBL raised dividends paid from approximately $50 million in FY24 to nearly $77 million in FY25 despite ongoing portfolio transformations emphasizing selective asset disposals over aggressive growth initiatives [F1][S13][S15]. Common stock dividends per share ranged from $0.40 early in the year increasing to $0.45 per quarter later combined with a special dividend ($0.80 per share) distributed in Q1 2025 ensuring REIT compliance norms were met.

Authorized share repurchases were scaled back from $36 million executed in FY24 to about $18 million in FY25 indicating cautious capital allocation prioritizing balance sheet rehabilitation over buybacks during this transitional phase.

The approximate return on equity exceeding 36% based on trailing net income over equity signals meaningful value creation consistent with turnaround success metrics observed among similarly situated real estate operators leveraging operational leverage post-reorganization [F1].

Navigating Retail Real Estate Headwinds: Sector Risks and Execution Challenges

CBL explicitly cites critical risks including imminent substantial debt maturities totaling over $670 million due in the current year subject to extensions or refinancing outcomes—processes complicated by ongoing lender negotiations amidst sector-wide retailer volatility [S16][N1]. Tenant credit risk remains elevated given macroeconomic uncertainty affecting discretionary spending patterns contributing to occupancy fluctuations particularly within legacy mall formats.

Execution risks inherent in repositioning legacy anchor spaces into viable mixed-use or non-retail usages require careful project management capabilities alongside favorable leasing momentum; failure here could impair projected NOI improvements critical for servicing elevated leverage loads.

Additionally, litigation contingencies related to foreclosure processes on select assets such as Jefferson Mall underline operational challenges navigating distressed holdings.[S16]

Forward-Looking Indicators: Growth Catalysts and Performance Milestones to Watch

Absent explicit formal guidance beyond steady dividend declarations, investor attention should focus on several leading indicators identified by management and recent filings:

- Same-center net operating income growth trends indicate operational momentum post-acquisition cycle completion [N1];

- Lease-up rates for reconfigured anchor spaces directly impact future rent roll stability;

- Debt refinancing executions for key maturing loans especially secured term loan due late 2026;

- Further asset sales enabling potential reinvestment into higher-yielding properties or deleveraging;

- Development pipeline execution including joint ventures focused on non-retail uses such as hotels strengthening portfolio resilience over time [S3][S24].

Tracking these milestones will clarify whether CBL can sustain its regained profitability level while managing sector volatility effectively.

This analysis compiles data from CBL & Associates Properties’ SEC filings alongside relevant news releases without extrapolating beyond stated facts or forecasts provided by the company. It is intended solely for informational purposes without any investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments