NewLake Capital Partners Steadies Growth with Triple-Net Cannabis Real Estate Amid Tenant Credit Risks

Specialized focus on cannabis real estate underpins stable rental income while regulatory and tenant credit challenges persist.

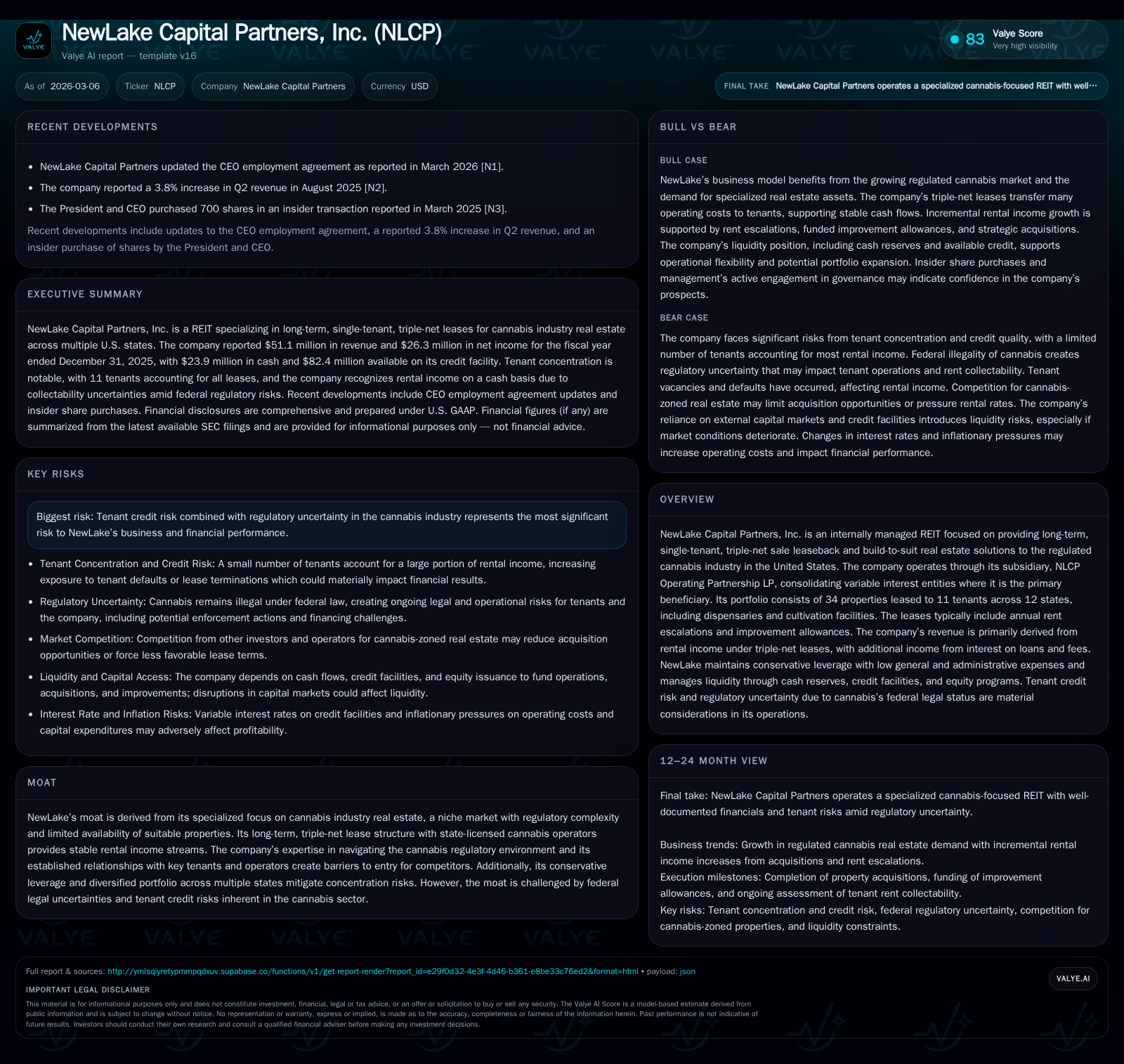

NewLake Capital Partners, Inc. operates as an internally managed REIT dedicated to single-tenant, triple-net leased cannabis industry properties across multiple U.S. states. The company’s historical growth has been driven by portfolio expansion and rent escalations, with 2025 revenue reaching $51.1 million, up 1.9% year-over-year. Future growth hinges on securing new tenants amid ongoing tenant defaults and regulatory uncertainties that affect lease stability. Capital allocation emphasizes dividend continuity backed by strong operating cash flows, conservative leverage, and an undrawn revolving credit facility, although tenant credit performance remains a key risk.

Company Overview

NewLake Capital Partners, Inc. (NLCP) is an internally managed real estate investment trust specializing exclusively in the regulated U.S. cannabis sector real estate market [S1]. The firm's portfolio consists of 34 single-tenant properties, including dispensaries and cultivation facilities leased on long-term, triple-net leases to 11 tenants operating in 12 states [S1]. These leases typically incorporate annual rent escalations and require tenants to cover real estate taxes, insurance, maintenance, and utilities—shifting operational cost burdens away from NewLake [S1].

The company's moat stems from its niche specialization in cannabis-specific real estate—a market marked by complex regulatory overlays and limited suitable property availability—which creates entry barriers for competitors . It also benefits from its expertise navigating the regulatory landscape and established relationships with licensed operators.

Historical Financial Performance

NewLake has seen steady financial growth over recent years, driven primarily by portfolio acquisition and rent escalations under triple-net leases despite operational obstacles within its tenant base:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 51 | 26 | 42 | 27 | +1.9% | +0.8% |

| 2024 | 50 | 26 | 43 | 27 | +6.0% | +6.2% |

| 2023 | 47 | 25 | 40 | 25 | +5.6% | |

| 2022 | 45 | 37 | 23 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 35 | 6.8 | |

| 2024 | 34 | 0 | 6.6 |

| 2023 | 33 | 12 | 6.1 |

| 2022 | 29 |

Source: SEC companyfacts cache [F1].

[Source: SEC filings [F1]]

Revenue climbed modestly by nearly two percent in 2025 compared to the prior year due primarily to contractual rent increases and portfolio stability [F1]. Operating income showed commensurate growth at roughly 1.7%, reflecting managed expense controls amid inflationary headwinds [S1]. Despite COVID-era disruptions lingering into earlier years for many operators, net income remained resilient with just under one percent improvement year-over-year.

Operating cash flow dipped marginally by about two percent in 2025 but continued to exceed net income comfortably—underlining strong cash generation from rental collections even amid some tenant payment irregularities [F1]. For example, two major tenant defaults impacted three properties during the year: AYR Wellness ceased paying rent after July while Revolutionary Clinics vacated its Fitchburg facility mid-2025 following receivership proceedings [S1].

The company posted impairment losses related to tenant credit issues including a $522 thousand write-down connected to Revolutionary Clinics’ warrants previously held [S13]. Nonetheless, NewLake actively pursued re-leasing vacated facilities to restore occupancy.

Portfolio Composition and Lease Structure

NewLake's portfolio diversification across multiple states balances geographic concentration risk inherent to cannabis operations given varying state regulations and market maturity levels . Tenant concentration is meaningful though diversified across leading Multi-State Operators (MSOs) such as Curaleaf (24%), Cresco Labs (14%), Trulieve (11%), among others—with top tenants accounting for the majority of annualized rental income [S2].

All leases are structured as triple-net agreements where tenants assume operational costs alongside fixed lease payments—allowing NewLake predictable revenue streams insulated from fluctuating expenses [S1]. Annual escalation clauses embedded within leases support steady income growth aligned with inflationary pressures noted at ~2-3% CPI trends in recent years [S1].

Tenant Credit Risk and Regulatory Environment

Tenant creditworthiness remains the pivotal challenge for NewLake’s business model due to volatile industry dynamics:

- AYR Wellness's restructuring agreement led to non-payment of rents for two cultivation facilities representing approximately 5% of total rental income in late-2025 [S1].

- Revolutionary Clinics operated at half rent before entering receivership and leaving its leased property vacant mid-2025 [S1].

- These cases underscore risks associated with tenants’ limited operating histories and ongoing capital market pressures facing MSOs with notable maturities through upcoming years [S1].

Federal prohibition continues to cast a shadow of uncertainty over state-regulated cannabis businesses limiting access to traditional banking and financing solutions which introduces volatility potential for lease renewals and collections [S1]. Re-leasing defaulted properties remains a critical operational priority but subject to legal timelines and local market conditions.

Growth Prospects and Constraints

Future growth depends largely on acquiring additional suitable assets within regulated markets and achieving lease renewals or replacements at or above current rents [N1][S1]. Expansion opportunities may manifest through build-to-suit developments or sale-leasebacks with emerging operators needing compliant facilities.

However, federal legal status ambiguity restrains broader capital access thereby impeding MSOs expansion pace which indirectly caps NewLake’s leasing pipeline velocity [S1]. Competition from diverse investor groups targeting ancillary cannabis real estate could pressure acquisition pricing dynamics.

Incremental development or redevelopment initiatives are currently modest but require close monitoring due to evolving material costs and supply chain considerations impacting project timelines [S1]. As of December 31, 2025, unfunded capital commitments were limited (~$0.4 million) indicating conservative expenditures aligned with leasing progress.[S24]

Capital Allocation and Financial Positioning

Returns to shareholders have been prioritized through consistent dividends aligning with REIT distribution requirements:

- In aggregate, cash dividends on common shares totaled approximately $35.3 million ($1.72/share) for FY 2025 versus $34.3 million ($1.70/share) in FY 2024 reflecting stable payout policy even amid earnings fluctuations [F1][S25][S17].

- No repurchases occurred under a board-approved stock buyback program that permits up to $10 million in repurchases but remains largely unused given liquidity preferences [S4][S5].

Financial leverage is low for a REIT of this profile:

- Revolving Credit Facility outstanding balance was only $7.6 million as of December 31, 2025 against a total commitment expanding up to $90–100 million subject to borrowing base availability [F1].

- The facility transitioned from fixed rate at

5.65% through May 2025 to variable tied to prime + margin (7–8% effective rate by year-end) without significant near-term interest cost impact due to low drawdown levels [S15][S16][S12]. - Equity capitalization remained stable with approximately 20.55 million common shares outstanding end-2025; institutional agreements provide nomination rights ensuring governance stability [S8][S9].

The calculated approximate return on equity based on reported net income divided by shareholders’ equity stood at around 6.8% for FY 2025—a level typical for specialized net-leased REITs balancing steady income versus growth profile constraints . Operating cash flows have been consistently ample relative to dividends paid ensuring coverage ratios remain healthy.[F1][S10]

Key Milestones & Monitoring Points

While explicit guidance beyond archived reporting is unavailable, investors and observers should watch for:

- Tenant lease renewal outcomes especially addressing previously defaulted properties dosed off in late-2024/early-2026.

- Changes in federal regulatory posture or banking access reforms affecting MSO credit profiles.

- Acquisition or disposition activity that would signal shifts in strategic portfolio management.

- Utilization levels of available debt capacity or ATM equity issuance programs highlighting capital strategy adjustments.

- Dividend sustainability vis-à-vis AFFO dynamics as detailed per SEC disclosures.

Sector Context Analysis

Cannabis-focused real estate REITs inhabit a narrow niche combining real estate fundamentals with unique industry risks—chief among them regulatory flux and tenant credit challenges atypical outside this sector given constrained financing options for operators. Triple-net lease structures grant landlord protections uncommon elsewhere yet cannot fully insulate against operator insolvency risks given concentration profiles frequently observed. As legalization spreads state-by-state gradually, pressure mounts for federal clarity which would greatly expand tenant pool quality over time. Liquidity management strategies such as sizable revolvers coupled with ATM programs prepare companies like NewLake for opportunistic asset deals or smoothing working capital needs amid cyclical shock absorption.

Disclaimer

This report is prepared solely for informational purposes based on publicly available information compiled by Valye News as of March 6, 2026; it does not constitute investment advice or endorsement of securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments