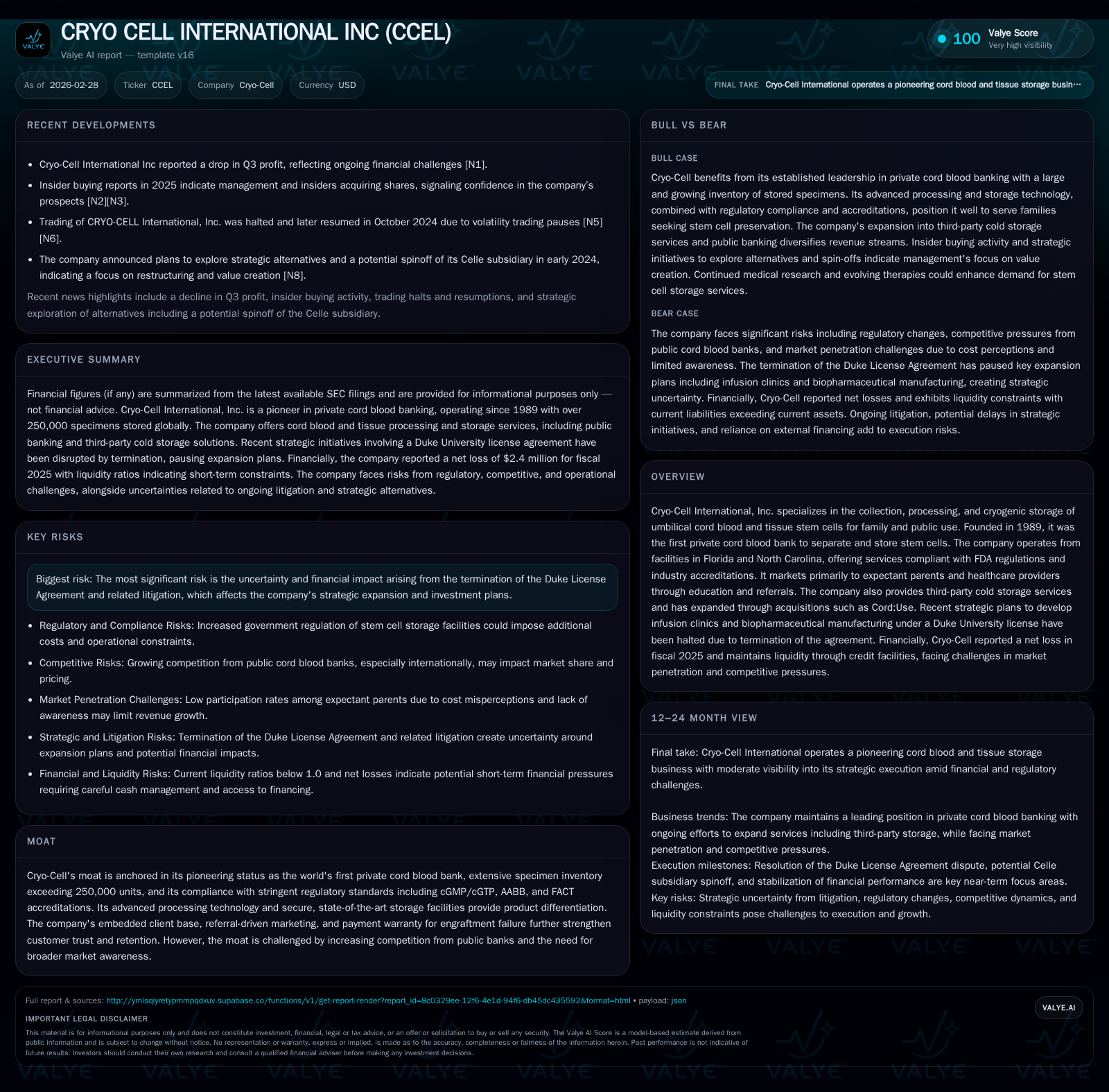

Cryo-Cell International's Transition: Assessing Growth, Litigation, and Financial Resilience

Cryo-Cell International balances historic market leadership in cord blood storage with litigation setbacks and evolving competitive pressures.

Cryo-Cell International, established as the first private cord blood bank, has sustained modest revenue growth yet faces tightening operating margins and net losses in its latest fiscal year. Its competitive moat is rooted in extensive specimen inventory and regulatory compliance, though strategic expansion plans linked to Duke University were halted due to license termination and ongoing arbitration. The company maintains positive operating cash flow but contends with suboptimal liquidity and a negative equity position while continuing shareholder returns through dividends and buybacks. Upcoming litigation resolutions and market developments remain key to its near-term financial trajectory.

Foundations of Growth: Historical Revenue and Operating Trends

Cryo-Cell International has demonstrated steady revenue growth from FY2014 through FY2017, with revenue increasing from approximately $20.1 million to about $25.4 million [F1]. The latest annual report for FY2025 shows revenue of approximately $28.57 million, marking a 9.8% increase over FY2024's $26.03 million [F1].

Despite top-line growth, profitability has weakened considerably. Operating income declined sharply by 86% to roughly $482 thousand in FY2025 from $3.48 million in FY2024 [F1]. Concurrently, net income swung back into a loss of approximately $2.43 million in FY2025 against a modest profit of $402 thousand the prior year [F1]. These results highlight increasing cost pressures amid competitive challenges.

Operating cash flow remained positive at about $5.48 million in FY2025 but contracted by nearly 9% compared to $6.01 million in FY2024 [F1]. Capital expenditures decreased substantially by over 90%, falling to roughly $230 thousand after heavier investments in previous years [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -2 | 5 | 0 | 0 | -704.2% |

| 2024 | 0 | 6 | 3 | 2 | +104.2% |

| 2023 | -10 | 9 | -12 | 7 | -443.6% |

| 2022 | 3 | 9 | 4 | 12 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($) | FCF ($mm) |

|---|---|---|---|

| 2025 | 3 | 169502 | 5 |

| 2024 | 2 | 1423871 | 4 |

| 2023 | 0 | 799036 | 2 |

| 2022 | 8 | 1819915 | -4 |

Source: SEC companyfacts cache [F1].

Historical data reflects steady revenue gains but recent profitability pressures despite positive cash flow.

Core Business Segments and Competitive Landscape

Cryo-Cell operates through three main segments: private family cellular processing and cryogenic storage focusing on umbilical cord blood and tissue stem cells; manufacturing of its proprietary PrepaCyte® CB Processing System; and public cord blood banking acquired via Cord:Use [S1][S19]. The company stores over 250,000 specimens globally, supporting substantial scale and service reliability [S1].

Facilities include processing operations headquartered in Oldsmar, Florida, with cryogenic storage conducted at an advanced facility in Durham, North Carolina utilizing commercial-grade units [S1][S19].

Regulatory compliance is rigorous with FDA registration under the Public Health Service Act and adherence to cGMP/cGTP standards complemented by AABB and FACT accreditations that underpin quality assurance [S21][S24]. These certifications help differentiate Cryo-Cell within an increasingly crowded market.

The company’s marketing focuses on direct-to-consumer education targeting expectant parents supported by a national network of field educators engaging healthcare providers for referrals—key drivers of new enrollments [S24]. Digital advertising campaigns also augment outreach.

Competition intensifies with roughly twenty-five other national private cord blood banks vying for customers alongside public cord blood banks offering no-cost donation options backed by government agencies [S13][S24]. This dynamic challenges growth potential for private banks like Cryo-Cell.

Duke License Termination and Legal Proceedings Impacting Strategy

A critical disruption occurred with Duke University's notice terminating the Patent and Technology License Agreement effective May 17, 2025 [S3][S18]. This license had granted Cryo-Cell rights to proprietary processes aimed at enabling regenerative therapies including planned infusion clinics addressing conditions such as cerebral palsy.

The termination halted development plans related to biopharmaceutical manufacturing capabilities under Cryo-Cell’s wholly owned subsidiary Celle Corp., which was intended to commercialize these technologies [S3][S17]. Arbitration commenced late 2024 with hearings scheduled for April 2026 [S3][S18].

Cryo-Cell contests Duke's counterclaims vigorously but acknowledges inherent uncertainty given the complexity of litigation which could materially impact financial results depending on arbitration outcomes [S3][S18]. The dispute pauses further capital deployment on these initiatives beyond limited comparability studies estimated under $350,000 [S17].

This setback curtails diversification prospects into clinical therapeutics beyond core storage services that previously forecasted multi-million dollar investments over five years before license termination [S17][S18].

Liquidity Position and Capital Structure Overview

At fiscal year-end November 30, 2025, Cryo-Cell reported current assets of approximately $11.75 million against current liabilities near $19.79 million resulting in a current ratio around 0.59 indicating near-term liquidity constraints despite positive operating cash flow generation [F1][S19].

Cash and cash equivalents stood at about $319 thousand at year-end [F1], down from prior periods partly due to debt repayments aligned with its credit arrangements.

The company maintains financing facilities comprising a revolving credit line up to $10 million and an outstanding term loan originally sized at approximately $8.96 million from Susser Bank with maturity in July 2032 [S4][S8][S9]. An interest rate swap was employed to manage floating rate risk but was terminated early April 2024 yielding proceeds recorded as income [S4][S9].

Operating cash flow of roughly $5.48 million against minimal capital expenditures (~$230 thousand) yielded free cash flow exceeding $5 million reinforcing internal funding capability despite negative shareholders' equity near -$18.6 million at fiscal year-end reflecting accumulated losses [F1].

Management anticipates discretionary capital spending around $1 million focused on equipment upgrades aligned with ongoing service enhancements while monitoring liquidity amid uncertain legal outcomes [S17][S19].

Dividend Payments and Share Repurchase Activity Reflect Capital Allocation Priorities

Despite recording net losses in FY2025 (-$2.43 million), Cryo-Cell distributed dividends totaling approximately $3.23 million demonstrating continued commitment to shareholder returns even amid profitability challenges [F1]. This represents an increase relative to ~$2 million dividends paid the previous fiscal year.

Share repurchases amounted to roughly $170 thousand during FY2025—a reduction from prior years' higher repurchase levels—reflecting more cautious capital deployment consistent with tighter financial conditions [F1].

These capital return activities appear primarily supported by strong operating cash flows rather than external financing given constrained liquidity profiles.

Strategic Refocus Following Duke Dispute

Following the abrupt cessation of Duke-related regenerative therapy commercialization plans due to license termination and ongoing arbitration, Cryo-Cell has reemphasized its historical core business of cellular preservation services providing stability amid strategic disruption [S3][S17].

R&D spending linked to these innovative therapies remains paused except for limited activities pending resolution of legal proceedings scheduled for mid-2026.

This retrenchment tempers near-term capital intensity but narrows competitive positioning relative to firms pursuing integrated therapeutic delivery models that could command higher margins.

Outlook: Key Considerations Ahead

Investor attention should focus on the April 2026 arbitration outcome between Cryo-Cell and Duke University as it will materially influence future financial performance and potential revival or redefinition of innovation strategies related to licensed therapies [S3][S18].

Competitive pressures from numerous private banks alongside public donation alternatives continue posing risks to demand growth among cost-sensitive families evaluating stem cell banking value propositions.

Ongoing regulatory scrutiny including FDA inspections under cGMP/cGTP standards combined with cybersecurity challenges necessitate operational vigilance given reputational dependencies inherent in healthcare services sectors [S21][S11].

Technological advances present both opportunities for product expansion post-storage as well as obsolescence threats if emergent therapies diminish conventional cord blood utility.

Maintaining strategic agility while managing litigation uncertainties will be essential for Cryo-Cell’s ability to sustain growth momentum anchored by its longstanding industry leadership established since pioneering private cord blood storage over three decades ago.

This analysis is based exclusively on audited SEC filings ([F1],[S#]) without speculative forecasts or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments