Cerus Corporation Bolsters Blood Safety Tech with Solid Q1 Revenue Growth

Cerus’ latest quarterly results highlight growing product adoption and strengthened governance, supporting its foothold in the blood safety segment.

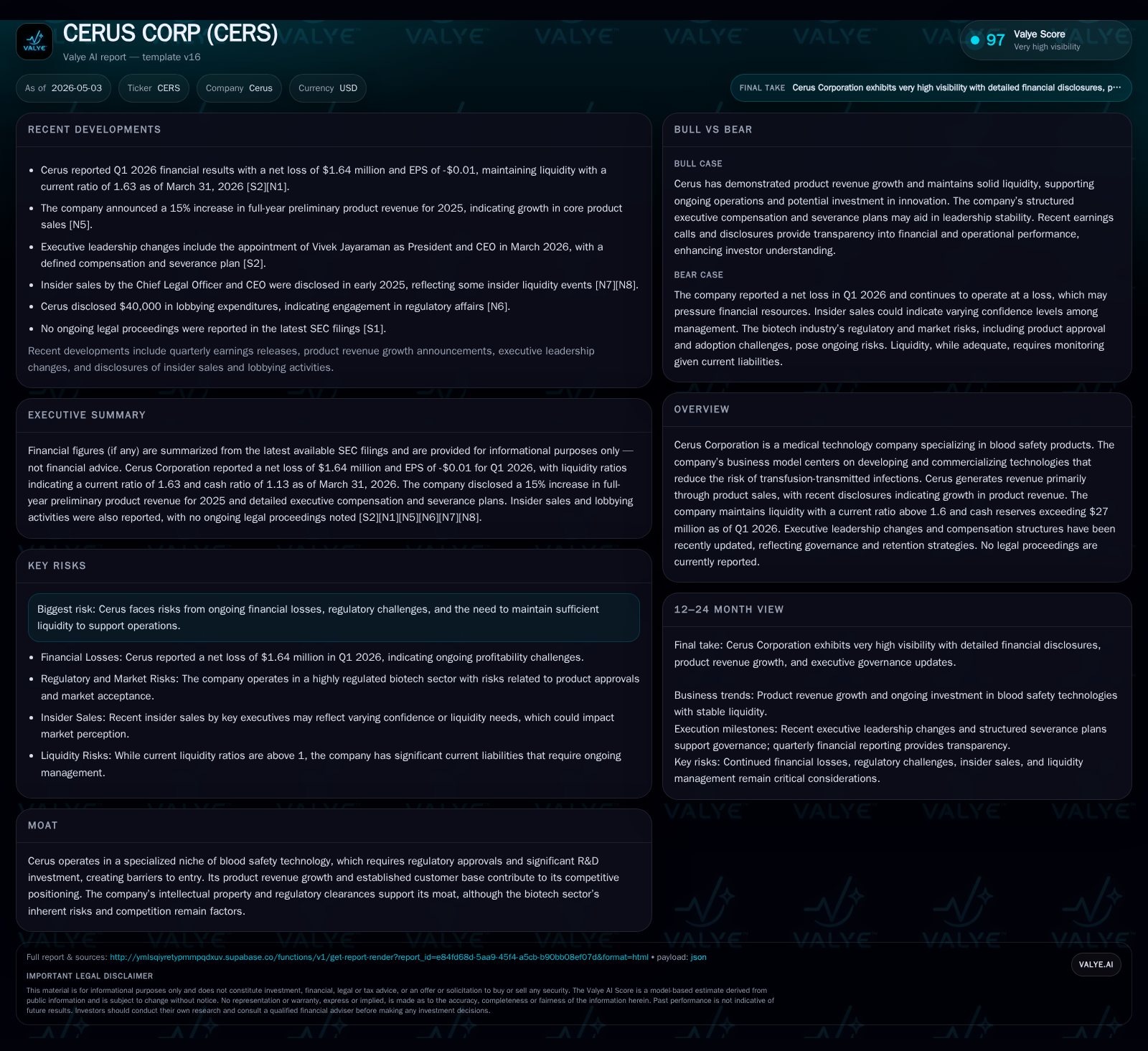

Cerus Corporation’s Q1 2026 filings reveal meaningful growth in product revenue alongside updates in executive severance policies, signaling fortified leadership alignment. The company’s core business centers on medical technologies aimed at reducing transfusion-transmitted infections, underpinned by a specialized regulatory and IP moat. Market expansion and new product initiatives drive near-term growth potential, although challenges include ongoing losses, liquidity management, and regulatory hurdles. Key upcoming milestones include monitoring sales momentum and regulatory progress as Cerus pushes for broader clinical adoption amid competitive pressures.

Q1 2026 Operating Highlights: Momentum Builds in Product Sales

Cerus Corporation’s latest quarterly report filed on April 30, 2026 (Form 10-Q) spotlights an acceleration in product revenue driven by expanding adoption of its blood safety solutions across its existing customer base and new market entrants [S2]. The company's financial results for Q1 underscore a strengthening business trajectory despite the backdrop of persistent net losses. Additionally, an 8-K filing on the same date disclosed a revised severance plan for key executives designed to incentivize retention and align leadership interests amid ongoing commercialization efforts [S24][S26], which may improve organizational stability during critical growth phases.

The company announced its first quarter performance including both top-line growth and strategic governance updates simultaneously – reinforcing Cerus’ commitment to operational scalability and executive accountability. This synergy of commercial traction with corporate policy advancement marks a pivotal inflection in Cerus' execution cadence [N1].

Cerus’ Business Model: Innovation at the Heart of Blood Safety

Cerus generates revenue primarily through sales of patented medical technologies that mitigate transfusion-transmitted infections — a life-threatening risk in blood transfusions [S1][S2]. The core of Cerus’ offering is its pathogen reduction system which treats blood components such as platelets and plasma to inactivate viruses, bacteria, and parasites. Hospitals, blood banks, and transfusion service providers constitute the primary customers who pay for consumable kits and related equipment.

The revenue mechanics link closely to volume usage (number of treated blood units), pricing per treatment kit, and contract renewals. Product revenues gradually scale as more institutions adopt Cerus’ systems given regulatory clearances that provide clinical validation and reimbursement pathways. Margins benefit from proprietary technology and recurring kit sales; however, investment in R&D remains essential to maintain efficacy against emerging pathogens and broaden product indications.

Customer retention hinges on clinical trust due to the safety-critical nature of blood products; thus switching costs are significant. Distribution is managed through specialized channels servicing hospital networks with training support to ensure correct usage — further embedding Cerus within transfusion workflows.

Competitive Moat and Industry Structure: Navigating Regulatory Barriers

The blood safety segment inhabited by Cerus is niche yet heavily regulated — creating formidable entry barriers for competitors. Regulatory approvals from agencies like the FDA require rigorous clinical trials demonstrating pathogen reduction efficacy without compromising blood component quality [S1][S5]. This gatekeeping effect protects incumbents such as Cerus who have invested over years in scientific validation.

Cerus maintains an intellectual property portfolio protecting its proprietary photochemical treatment processes which further limits rivalry. Industry players must surmount not only scientific challenges but also navigate complex reimbursement environments tied to healthcare regulation.

R&D intensity is high relative to the size of the addressable market; this acts as a deterrent for new entrants who would face steep development timelines before generating meaningful revenues. Additionally, hospitals demonstrate inertia once integrated due to procedural risk aversion around blood safety — strengthening Cerus’ customer stickiness.

Growth Drivers: Commercial Expansion and New Product Initiatives

Looking ahead, several factors are poised to drive Cerus’ growth trajectory. First, expanded penetration into untapped geographic markets with nascent adoption supports incremental volume gains [S2][N1]. Second, pipeline developments aimed at new clinical applications or enhancements to existing products could broaden usage across additional blood components or patient populations.

Recent order bookings suggest rising commercial momentum as hospitals incorporate pathogen reduction more broadly [S3]. Regulatory filings underway or anticipated may unlock further approvals that catalyze expansion beyond current indications. Strategic initiatives also hint at scaling manufacturing capabilities to meet growing demand efficiently.

This stage reflects a structural growth environment fueled by structural shifts toward safer transfusion practices globally — less reliant on cyclical trends — supported by robust clinical evidence discouraging substitution.

Risks and Constraints: Regulatory, Liquidity, and Market Adoption Challenges

Notwithstanding positive operational signals, Cerus faces several risks illuminated through recent filings. Losses persist at the operating level driven by ongoing investment in R&D and commercial infrastructure required to penetrate complex healthcare markets [S2][F1]. Sustaining sufficient liquidity remains critical given a substantial net debt position reflected by $57M approximate net leverage versus cash reserves just below $28M at quarter end [F1].

Regulatory uncertainties remain material risks inherent to biotech segment firms such as Cerus; any delays or adverse outcomes in approval processes could stall adoption curves or require costly post-market commitments [S19]. Moreover, hospital budgets cyclically pressure new capital expenditures limiting speed of new system installations or kit purchases despite clinical benefits.

Lastly, competition from alternative infection mitigation technologies or novel approaches represents ongoing threats requiring continuous innovation.

What to Watch Next: Key Milestones and Execution Metrics Ahead

Market participants should closely monitor subsequent quarterly releases for sustained product revenue growth metrics indicating deepening customer footprint beyond initial wins [S3]. Any announced regulatory clearances or submission updates will be important leading indicators of potential near-term addressable market expansion.

Partnership developments or distribution agreements could amplify commercial reach while management commentary from earnings calls offers qualitative insight into execution risks or emerging trends influencing demand trajectory [N1]. Finally, tracking operating cash flow dynamics against capital requirements will be crucial to assessing financial flexibility amid loss-making status.

Financial Snapshot: Liquidity, Leverage, and Capital Position

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $28mm | |

| 2026-03-31 | ||

| Total debt | $85mm | |

| 2026-03-31 | ||

| Net debt | $57mm | |

| 2026-03-31 | ||

| Current assets | $175mm | |

| 2026-03-31 | ||

| Current liabilities | $107mm | |

| 2026-03-31 | ||

| Current ratio | 1.63x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value | Period Ended |

|---|---|---|

| Cash & Equivalents | $27.85M | |

| 2026-03-31 | ||

| Total Debt | $84.90M | |

| 2026-03-31 | ||

| Net Debt | $57.05M | |

| 2026-03-31 | ||

| Current Assets | $175.34M | |

| 2026-03-31 | ||

| Current Liabilities | $107.38M | |

| 2026-03-31 | ||

| Current Ratio | 1.63x | |

| 2026-03-31 |

Cerus enters Q2 with a balanced liquidity profile highlighted by a current ratio above 1.6x evidencing an adequate buffer over near-term obligations despite elevated leverage levels dominated by long-term debt figures [F1][S2]. Cash reserves near $28 million provide some runway for operational needs though capital raising may eventually be needed given sustained negative earnings trends.

This financial stance underscores a phase typical of medtech innovators gaining traction yet investing heavily ahead of profitability milestones.

This analysis synthesizes facts strictly disclosed through the latest SEC filings alongside corroborated news transcripts without speculative extrapolation beyond documented evidence. It aims to provide an informed industry viewpoint emphasizing operational developments contextualized within sector dynamics relevant to Cerus Corporation’s current standing.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments