AMC Entertainment Faces Liquidity Constraints as Q1 2026 Loss Narrows Amidst Refinancing Progress

AMC's latest quarter shows improving revenue but ongoing net losses and high leverage present significant near-term challenges.

In its Q1 2026 filing, AMC reported a net loss yet exceeded revenue expectations, maintaining strong brand presence through premium formats and loyalty initiatives. The company’s extensive theatre network and strategic refinancing efforts underpin its competitive moat. However, persistent dilution, sub-1.0 current ratio, and evolving industry demand patterns constrain growth visibility. Monitoring debt maturities, box office trends, and execution of synergistic enhancements will be critical in the near term.

Recent Operating Update: Results and Refinancing Developments

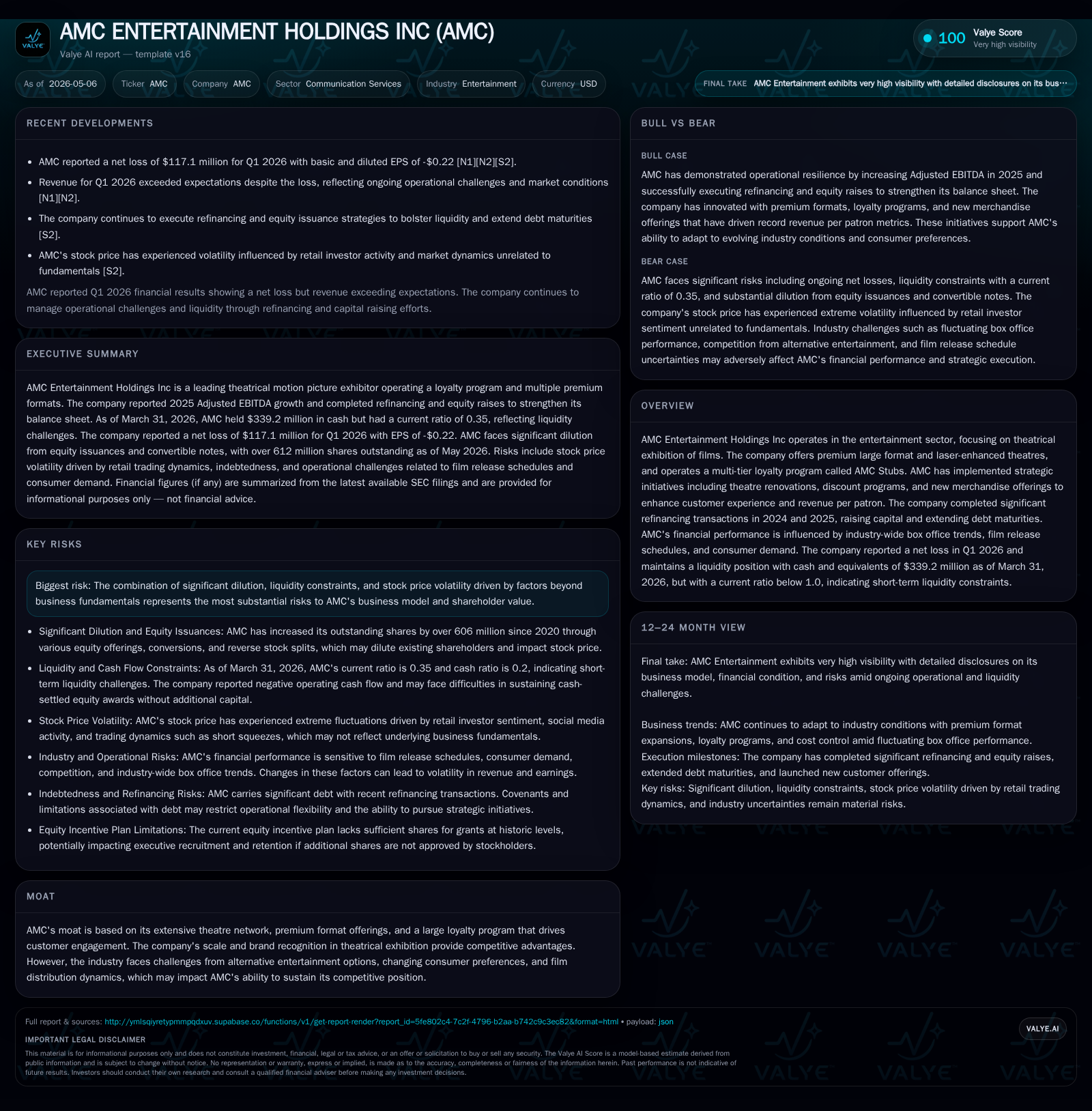

AMC Entertainment Holdings Inc’s Q1 2026 quarterly filing and associated event disclosures reflect a nuanced picture of operational resilience shadowed by financial strain. The company announced a net loss for the quarter ended March 31, 2026; however, reported revenues surpassed analyst expectations amid a gradual normalization of cinema attendance post-pandemic pressures [S2][N1]. This uptick is notable given the broader entertainment sector dynamics.

AMC held approximately $339 million in cash and equivalents while total current assets stood at $582.7 million against current liabilities of $1.665 billion, resulting in a challenging current ratio of 0.35 [F1]. This indicates AMC faces near-term liquidity constraints that could pressure working capital requirements absent improved cash flow generation or external financing support.

The company's total debt level remains elevated at roughly $4.02 billion with net debt near $3.68 billion after adjusting for available cash reserves [F1]. Recent refinancing transactions completed between mid-2024 through 2025—including large-scale note issuances by Muvico LLC (an AMC subsidiary), exchangeable notes conversions, and extending debt maturities—have partially mitigated immediate refinancing risks but have contributed to dilution via new equity issuance linked to note conversions and preferred stock exchanges [S1][S2]. These moves extend capital runway but increase complexity in AMC’s capital structure.

Business Model: Theatrical Exhibition with Strategic Enhancements

AMC’s primary revenue model centers on theatrical exhibition across its expansive global network of movie theatres. The offering leverages premium large-format screens enhanced with laser technologies that command higher ticket pricing — a differentiation rooted in quality presentation standards that justify consumer spend beyond standard viewing experiences [S1]. Concurrently, AMC operates AMC Stubs, a multi-tier loyalty program designed to enhance patron retention through rewards and tiered benefits that encourage repeat visits.

Revenue inflows derive from ticket sales (affected by volume and pricing), concession sales (food/beverage), advertising within theatres, and ancillary streams such as merchandise offerings introduced recently to augment per-customer revenue yields [S1]. Customer adoption is influenced by film content availability dictated by studios' release schedules (which have fluctuated due to pandemic-related strikes), competitive entertainment options including streaming services and home-viewing alternatives, as well as consumer discretionary spending trends.

Pricing power exhibits some elasticity; while premium formats enable ticket rate premiums, broader pricing sensitivity persists given alternative entertainment substitutes. Therefore, AMC’s strategy includes discount programs aimed at increasing volume while balancing yield optimization [S1]. Service quality improvements through renovations contribute to enhanced customer experience—a necessary step to maintain competitiveness.

Industry Structure and Competitive Position

The theatrical exhibition market is characterized by high fixed costs related to real estate leases, labor, technology upgrades, and maintenance. AMC's scale—being one of the largest chains—provides advantage through bargaining power with distributors and economies of scale in operations.

Competition arises notably from other major cinema operators as well as digital streaming platforms eroding traditional exclusivity of feature films in theatres. The industry's evolution towards shortened theatrical windows further compresses potential revenue capture from high-profile releases.

AMC’s brand recognition enhances its moat alongside its loyalty program which functions as a switching cost mechanism fostering recurring customer engagement. Nonetheless, the shift in consumer preferences toward at-home entertainment necessitates continuous innovation in premium experiences to sustain foot traffic.

Growth Drivers

Key growth drivers identified include:

- Box Office Recovery: As global markets stabilize post-pandemic disruptions, the resurgence in film releases supports incremental attendance gains.

- Premium Formats Expansion: Augmentation of IMAX-style or laser-enhanced auditoriums increases per-ticket revenue potential.

- Loyalty Program Monetization: Enhancements to AMC Stubs aim at deeper patron capture with potential upsells on concessions and exclusive offers.

- Strategic Renovations: Upgrading physical venues to elevate overall guest experience aligns with market demand for differentiated settings amid growing leisure competition.

- Synergistic Debt Refinancing: Refinancing reduces near-term obligations stress allowing focus on operational improvements.[S3][N1]

These drivers hinge on successful film content pipelines remaining robust without extended delays or labor stoppages which have previously disrupted studio schedules significantly.

Risks / Watchpoints / Growth Constraints

The foremost risk remains AMC’s substantial debt load coupled with liquidity pressures evidenced by the low current ratio – both impart operational constraints on funding discretionary investments or absorbing downturns effectively [F1][S2]. Significant recent equity dilution raises concerns over shareholder value erosion and introduces volatility decoupled from fundamental business performance.

Entertainment industry structural shifts challenge AMC’s traditional exhibition dominance: increased streaming penetration reduces exclusive theatrical windows; alternative leisure activities compete for discretionary dollars; supply chain issues increase operating costs; labor markets affect staffing/social distancing norms impacting capacity utilization.[S5]

Restrictive covenants embedded within recent credit agreements limit flexibility for mergers/acquisitions or aggressive capital expenditures essential for circuit optimization.[S26] Lastly, reliance on blockbuster film releases injects cyclicality into revenue streams requiring careful capacity planning.

What to Watch Next

Investors should closely track:

- Quarterly box office attendance trends domestically and internationally post-COVID normalization.

- Execution milestones on refinancing terms finalized in early 2026 including adherence to covenant constraints.[S3][S26]

- Financial performance stabilization especially margin improvement stemming from cost management and pricing initiatives.

- Loyalty program metrics including member growth rates and average spend enhancement which signal customer engagement strength.

- Potential regulatory or technological developments impacting exclusive theatrical release windows or AI adoption in filmmaking affecting content supply.[S1]

Financial Profile Summary (Q1 2026 Snapshot)

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $339mm | |

| 2026-03-31 | ||

| Total debt | $4.0bn | |

| 2026-03-31 | ||

| Net debt | $3.7bn | |

| 2026-03-31 | ||

| Current assets | $583mm | |

| 2026-03-31 | ||

| Current liabilities | $1665mm | |

| 2026-03-31 | ||

| Current ratio | 0.35x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

Source: Company filings Q1 10-Q dated May 5, 2026 [F1]

The financial snapshot underscores the tight liquidity situation despite strong cash reserves due to sizable short-term liability load.

Disclaimer: This analysis is provided for informational purposes only based on publicly available information as of May 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments