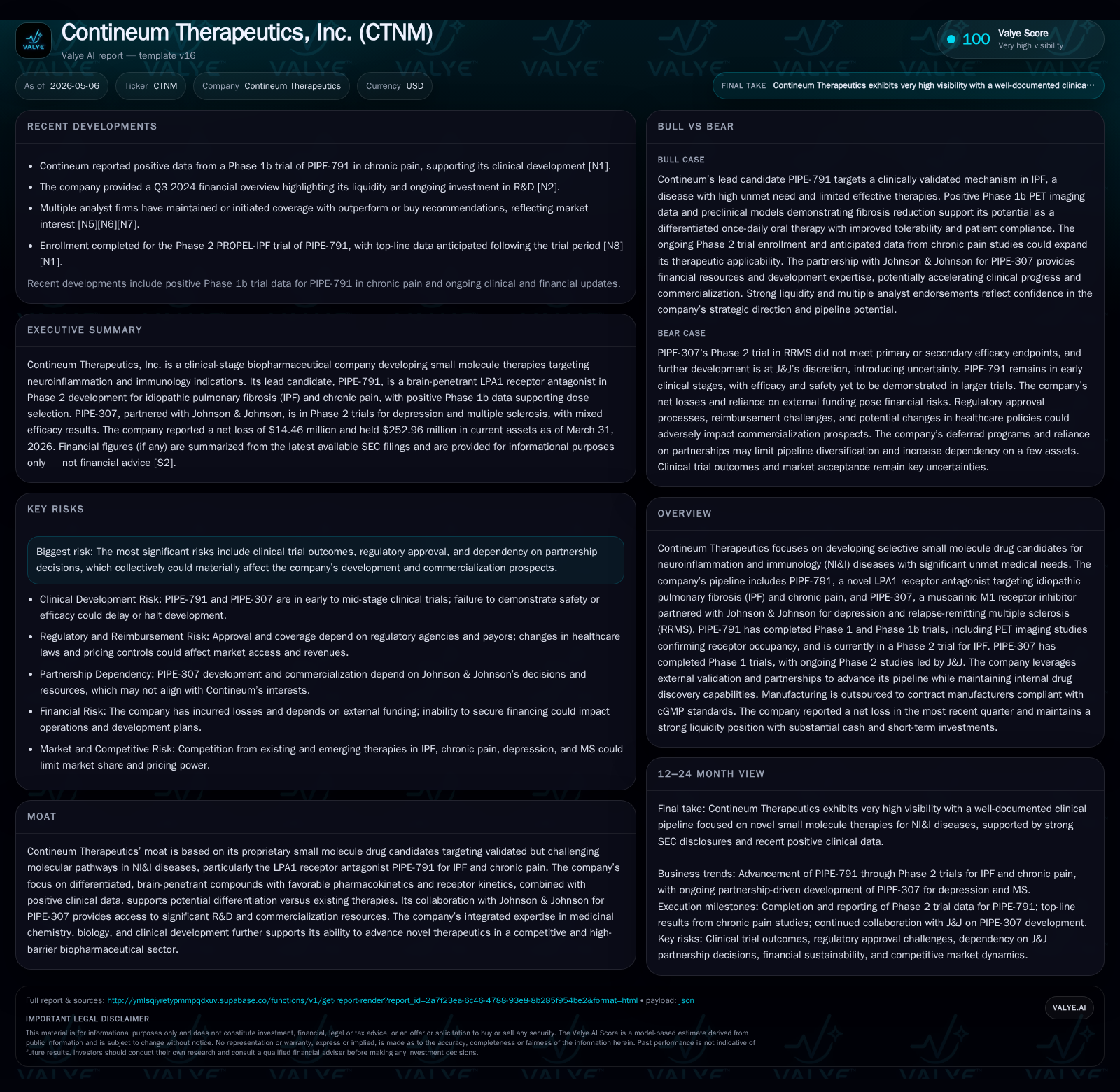

Contineum Therapeutics Advances PIPE-791 Phase 2 Amidst Strategic J&J Partnership Dynamics

The company progresses PIPE-791 into Phase 2 for IPF while managing pivotal partnership developments on PIPE-307 with Johnson & Johnson.

In its Q1 2026 filing, Contineum Therapeutics reported initiation of a Phase 2 clinical trial for PIPE-791 targeting idiopathic pulmonary fibrosis, alongside promising Phase 1b chronic pain data expected imminently. The partner-led PIPE-307 program under Johnson & Johnson exhibits mixed Phase 2 results, with J&J retaining sole discretion over future development. The firm's proprietary focus on selective small molecules for neuroinflammation and immunology, coupled with a strategic alliance and manufacturing outsourcing, underpin its developmental progress in a competitive and capital-intensive sector. Significant risks remain tied to clinical outcomes and regulatory pathways, balanced by solid liquidity and measured operating cash use.

Latest Quarterly Operating Update: Insights from Q1 2026 Filing

Contineum Therapeutics’ latest quarterly report filed on May 5, 2026 ([S2]) marks a notable operational inflection point as the company transitions PIPE-791—a lysophosphatidic acid 1 receptor (LPA1R) antagonist—into its Phase 2 clinical trial for idiopathic pulmonary fibrosis (IPF), initiated in December 2025. This advancement is materially supported by prior pharmacokinetics (PK) and positron emission tomography (PET) receptor occupancy data affirming adequate target engagement and dose selection. Additionally, the company completed enrollment in a randomized Phase 1b study examining PIPE-791’s safety and efficacy in chronic osteoarthritic and low back pain indications.

Anticipation builds around the Q2 2026 top-line disclosure of this chronic pain study, following positive signals highlighted in an April press release ([N1]). These developments collectively strengthen PIPE-791’s clinical validation trajectory beyond the pulmonary space.

Meanwhile, the partnered drug candidate PIPE-307—an M1 muscarinic receptor inhibitor developed in collaboration with Johnson & Johnson (J&J)—continues its evaluation after mixed results from the November 2025 Phase 2 VISTA trial in relapse-remitting multiple sclerosis (RRMS) patients ([S1], [S3]). Despite acceptable safety profiles at tested doses, the trial failed to meet primary or secondary efficacy endpoints. J&J now holds sole discretion over further development directions across both RRMS and major depressive disorder (MDD) indications studied in ongoing trials.

Business Model and Drug Candidate Differentiation

Contineum operates as a clinical-stage biopharmaceutical innovator specializing in selective small molecule therapies targeting neuroinflammation and immunology (NI&I) disorders with high unmet needs ([S1], Valye excerpt). The core of its business model leverages proprietary chemistry assets to address molecular pathways difficult to modulate via existing approaches.

PIPE-791 epitomizes this strategy—a brain penetrant LPA1R antagonist exhibiting low plasma protein binding combined with prolonged receptor residence time—potentially enabling differentiated therapeutic effects for IPF and chronic pain relative to currently approved options. Manufacturing responsibilities are outsourced to contract organizations compliant with Good Manufacturing Practices (cGMP), providing scalability while concentrating internal resources on discovery and clinical development ([S1]).

PIPE-307 complements this pipeline as a selective muscarinic M1 receptor inhibitor partnered with J&J. This alliance not only supplies upfront capital but also access to J&J’s global R&D infrastructure and future commercialization capabilities—critical given the costly nature of CNS drug development.

The company’s revenue-generation prospects hinge primarily on milestone payments from partnered programs like PIPE-307 plus potential royalties following commercialization; wholly-owned assets such as PIPE-791 represent longer-term value creation dependent on successful late-stage trials.

Competitive Position within Neuroinflammation & Immunology Therapeutics

The NI&I sector is characterized by complex biology requiring significant R&D investment compounded by stringent regulatory scrutiny. Contineum distinguishes itself through small molecules targeting validated but challenging receptors such as LPA1R—areas traditionally overshadowed by monoclonal antibodies or biologic agents due to delivery difficulties across the blood-brain barrier ().

Additionally, Contineum’s integration of medicinal chemistry expertise with translational biology supports tailored compound profiles optimizing bioavailability and receptor kinetics—key differentiators that elevate its candidates above generic approaches.

The strategic partnership with J&J enhances competitive positioning by mitigating development risks for PIPE-307 while opening pathways toward broader indications if efficacy hurdles can be overcome.

Outsourcing manufacturing to cGMP-compliant contract manufacturers minimizes capital-intensive asset buildout while maintaining supply chain integrity—a crucial operational facet given the sensitivity of clinical-stage drug production ([S1]).

Key Growth Drivers: Clinical Trials and Strategic Collaborations

Near-term expansion hinges on multiple clinical catalysts:

- Completion and reporting of Phase 1b chronic pain trial data for PIPE-791 anticipated in Q2 2026 could substantiate pipeline diversification beyond IPF ([N1]).

- Ongoing recruitment and initial safety/tolerability analyses from the ongoing Phase 2 IPF study will further validate dosing regimens chosen via prior PET imaging studies ([S2]).

- Meanwhile, J&J’s decisions regarding continuation or termination of the PIPE-307 program for RRMS or MDD will materially influence pipeline breadth and milestone revenue potential ([S3]).

These events are tightly linked to measurable KPIs such as patient enrollment rates, dose-confirmation studies from receptor occupancy imaging, regulatory feedback during IND reviews, and partner-funded R&D investments—all informing valuation inflection points.

Risks and Constraints: Clinical, Regulatory, and Partnership Dependencies

Significant risks envelop Contineum’s operations:

- The binary nature of clinical trial readouts poses an inherent volatility risk: failure to demonstrate efficacy or unforeseen safety issues could derail pivotal programs ([S4], ).

- Regulatory approval processes remain costly and protracted; ensuring compliance across multiple jurisdictions compounds complexity.

- Heavy reliance on J&J's discretion over PIPE-307’s development introduces uncertainty that limits Contineum’s control over a key asset’s trajectory ([S3]).

- Third-party contract manufacturers present operational risks including potential delays due to compliance failures or capacity constraints.

- Product liability insurance costs increase exposure during late-stage trials and eventual commercial launch phases.

While these cautionary factors are prevalent industry-wide among clinical-stage biotechs, their materialization could sharply affect operability and investor confidence.

Upcoming Catalysts: Pipeline Milestones and Market Signals

Market participants should closely monitor:

- Q2 2026 top-line data release from PIPE-791 chronic pain study may validate multi-indication potential indicating market sizing expansion.[N1]

- Interim readouts or safety updates from ongoing Phase 2 IPF trial (initiated December 2025) offering early signals for dose optimization or adverse event profiles.[S2]

- Formal decisions by J&J regarding continued investment or licensing actions related to PIPE-307 following mixed Phase 2 results.[S3]

Successful outcomes across these milestones could unlock incremental licensing revenues or bolster royalty trajectories contingent upon regulatory approvals.

Financial Snapshot: Liquidity and Operating Cash Flow Context

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $20mm | |

| 2026-03-31 | ||

| Current assets | $253mm | |

| 2026-03-31 | ||

| Current liabilities | $7mm | |

| 2026-03-31 | ||

| Current ratio | 38x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As of March 31, 2026 ([F1]), Contineum held approximately $20.16 million in cash and equivalents alongside $253 million in current assets against modest current liabilities near $6.7 million—a resultant current ratio near an ample 38 signaling near-term liquidity sufficiency.

Operating losses continue consistent with early-stage biotech norms; latest available operating income was negative $68 million as per year-end figures ([F1]), reflecting heavy investment in pipeline advancement rather than revenue generation at this stage.

Solid capital reserves reinforce runway coverage through key clinical milestones presently underway without an immediate need for capital raising; however, eventual scalability toward commercialization will necessitate additional funding mechanisms or partnership expansions.

This analysis synthesizes Contineum Therapeutics' latest SEC disclosures compellingly anchored on May 2026 filings incorporating precise clinical developments contextualized with strategic business considerations. While recognizing substantial sectoral risk factors intrinsic to early-stage biopharma innovation, Contineum demonstrates forward momentum via targeted pipeline execution underpinned by judicious external collaborations. Continued monitoring of forthcoming data readouts alongside partner dynamics remains essential to assess evolving investment narratives.

This report is informational only; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments