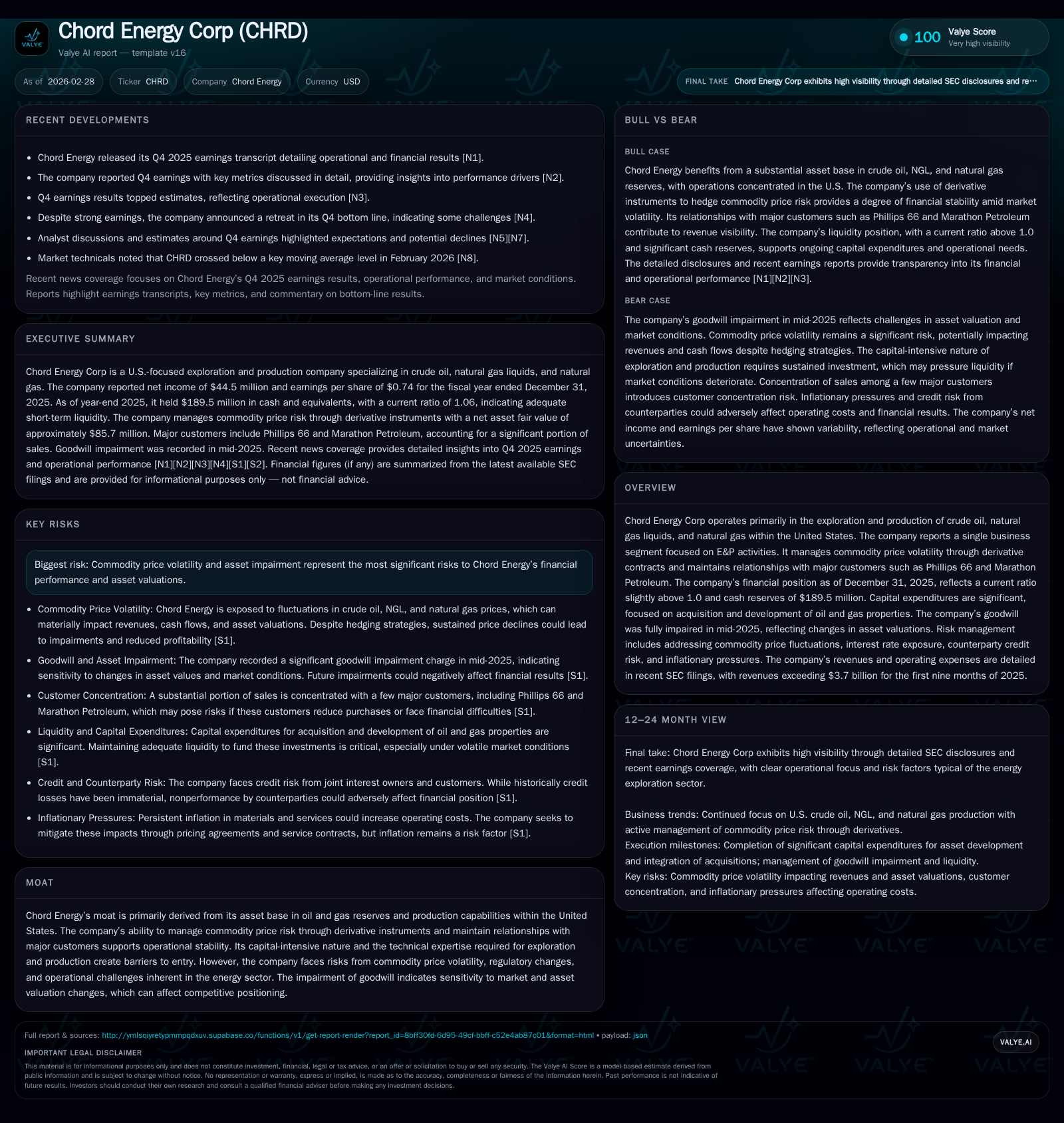

Chord Energy Corp’s Earnings Retreat Reflects Commodity Price Sensitivity and Capital Discipline

A sharp decline in Chord Energy's 2025 profitability underscores the impact of commodity price swings and the company’s calibrated capital allocation response.

In 2025, Chord Energy Corp experienced a pronounced contraction in earnings after a period of sustained growth, reflecting heightened sensitivity to fluctuations in crude oil and natural gas prices. The company's strategic deployment of derivative hedging instruments alongside stringent capital discipline—evident in substantial capex reductions and maintained shareholder returns via dividends and buybacks—aimed to buffer volatility. Robust liquidity standing, backed by an affirmed borrowing base and manageable debt maturities, supports operational resilience amid ongoing market uncertainty. Key performance indicators such as a modest 0.6% ROE and significant free cash flow generation spotlight financial stability but also signal challenges in translating top-line activity into net income.

Strong Growth History Undermined by 2025 Earnings Contraction

Chord Energy exhibited strong earnings growth from 2022 through 2024 with operating income peaking at $1.27 billion in FY2023 before declining to $1.10 billion in FY2024 [F1]. However, this momentum reversed sharply in FY2025 when operating income dropped approximately 82% year-over-year to $197 million [F1]. Net income similarly contracted by nearly 95%, falling to $44.5 million [F1]. Despite these declines, operating cash flow remained resilient at just over $2 billion for the year ended December 31, 2025, down slightly from prior periods [F1].

Capital expenditures fell dramatically by more than 250% in FY2025 compared to FY2024, reflecting a deliberate reduction in investment amid weaker profitability [F1]. The company’s liquidity position remained solid with a current ratio of approximately 1.06 supported by nearly $190 million in cash and equivalents at year-end [F1]. Key financial metrics are summarized below:

Historical performance (annual)

| FY | Net ($mm) | CFO ($bn) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 44 | 2.0 | 197 | -94.8% |

| 2024 | 849 | 2.1 | 1100 | -17.1% |

| 2023 | 1024 | 1.8 | 1273 | -44.8% |

| 2022 | 1856 | 1.9 | 1584 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 318 | 365 | 0.6 |

| 2024 | 530 | 444 | 9.8 |

| 2023 | 500 | 239 | 20.2 |

| 2022 | 655 | 152 | 39.7 |

Source: SEC companyfacts cache [F1].

Commodity Price Volatility: Derivative Hedge Strategies and Market Impacts

Chord Energy actively manages commodity price risk through derivative contracts including three-way collars, two-way collars, and fixed-price swaps extending through at least calendar year 2028 [S1]. These contracts cover millions of barrels of crude oil annually with structured price floors generally ranging from $45 to $49 per barrel and ceilings up to about $74 per barrel. Natural gas swaps cover volumes priced around $4 per MMBtu [S1].

This hedging program stabilizes revenue streams against volatile market prices while limiting downside exposure and capping some upside potential—a common approach within exploration and production firms [S1]. The company mitigates counterparty credit risk by engaging investment-grade counterparties primarily drawn from its lending syndicate [S21].

Reserve Valuations and Goodwill Impairment Amid Pricing Challenges

In mid-2025, Chord recorded a goodwill impairment attributed to downward revisions in reserve valuations linked to lower SEC benchmark prices ($65.34 per barrel crude oil; $3.39 per MMBtu natural gas for FY2025) [S1][F1]. The PV-10 metric—which reflects present value of estimated future net revenues based on SEC pricing—showed sensitivity of approximately ±30 million barrels of oil equivalent reserves or ±$1.8 billion valuation change under ±10% price swings [S1]. This adjustment underscores the material impact of prevailing commodity prices on asset valuations.

Capital Allocation: Dividends, Buybacks, and Capex Discipline

Chord balanced capital discipline with shareholder returns during FY2025 [S10][S14]. Dividends totaled approximately $318 million—a decline of about 40% from the prior year—reflecting adjusted payout policies amid earnings pressure [F1][S10]. Concurrently, the company repurchased nearly $365 million of common stock under an authorized $1 billion share repurchase program initiated in August 2025 [F1][S14]. These measures illustrate a calibrated approach to capital allocation focused on maintaining liquidity while returning value to shareholders.

Liquidity and Debt Profile: Credit Facilities and Senior Notes

At December 31, 2025, Chord had no outstanding borrowings under its senior secured revolving credit facility which features an elected commitment amount of $2 billion within an affirmed borrowing base totaling $2.75 billion following the latest redetermination cycle [S1][S4][S5]. Letters of credit outstanding were minimal at roughly $33 million leaving ample unused capacity nearing $2 billion [S11].

Long-term debt includes equal tranches of senior unsecured notes maturing in October 2030 ($750 million at a coupon rate of 6%) and March 2033 ($750 million at approximately 6.75%) that replaced earlier maturing notes retired during FY2025 [S12][S17][S18]. The weighted average interest rate on borrowings under the credit facility improved to about 6.52% for FY2025 from over seven percent the prior year due to favorable amendments reducing margin fees [S9]. All relevant debt covenants were met comfortably as reported in recent filings [S8][S9][S12].

Outlook: Operational Focus Amid Market Uncertainty

Management commentary accompanying Q4 earnings emphasized monitoring production volumes targeting four to five operated rigs during most of calendar year 2026 as well as timing considerations related to capital project execution pacing [N1][N2][S15]. Upcoming commodity derivative contract rollovers will reset hedge floors and ceilings reflective of prevailing market conditions which could affect revenue stability going forward.

Additional risks flagged include inflationary cost pressures impacting operating expenses as well as evolving regulatory requirements that may influence permitting timelines or operational flexibility [N2][S16]. The next scheduled borrowing base redetermination expected around April 2026 represents another key milestone potentially influencing credit availability amid fluctuating reserve values.

Key Financial Metrics: ROE and Free Cash Flow Support Stability

Chord’s return on equity stands at approximately 0.6% based on trailing net income relative to equity exceeding $8 billion as of fiscal year-end December 31, 2025 [F1]. Operating cash flow generation remains robust near $2 billion supporting estimated free cash flow around $2.3 billion after accounting for capital expenditures—a positive indicator for liquidity maintenance despite profit compression.

Ongoing scrutiny on production trends will be critical given their direct linkage to revenue trajectory; closely tracking reserve replacement efficiency and depletion rates will provide insight into medium-term operational sustainability amid challenging commodity markets.

This analysis synthesizes information from Chord Energy’s public filings through February 28, 2026 along with recent earnings discussion without extrapolation beyond stated company data or guidance. It aims to offer an informed perspective on the company’s financial condition and strategic posture within the US exploration & production sector.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments