Rand Capital's Shift to Higher Yield Debt: Evaluating Returns and Risks

Rand Capital’s strategic pivot to higher-yield debt instruments reshapes its income profile amidst credit risk challenges in the lower middle market.

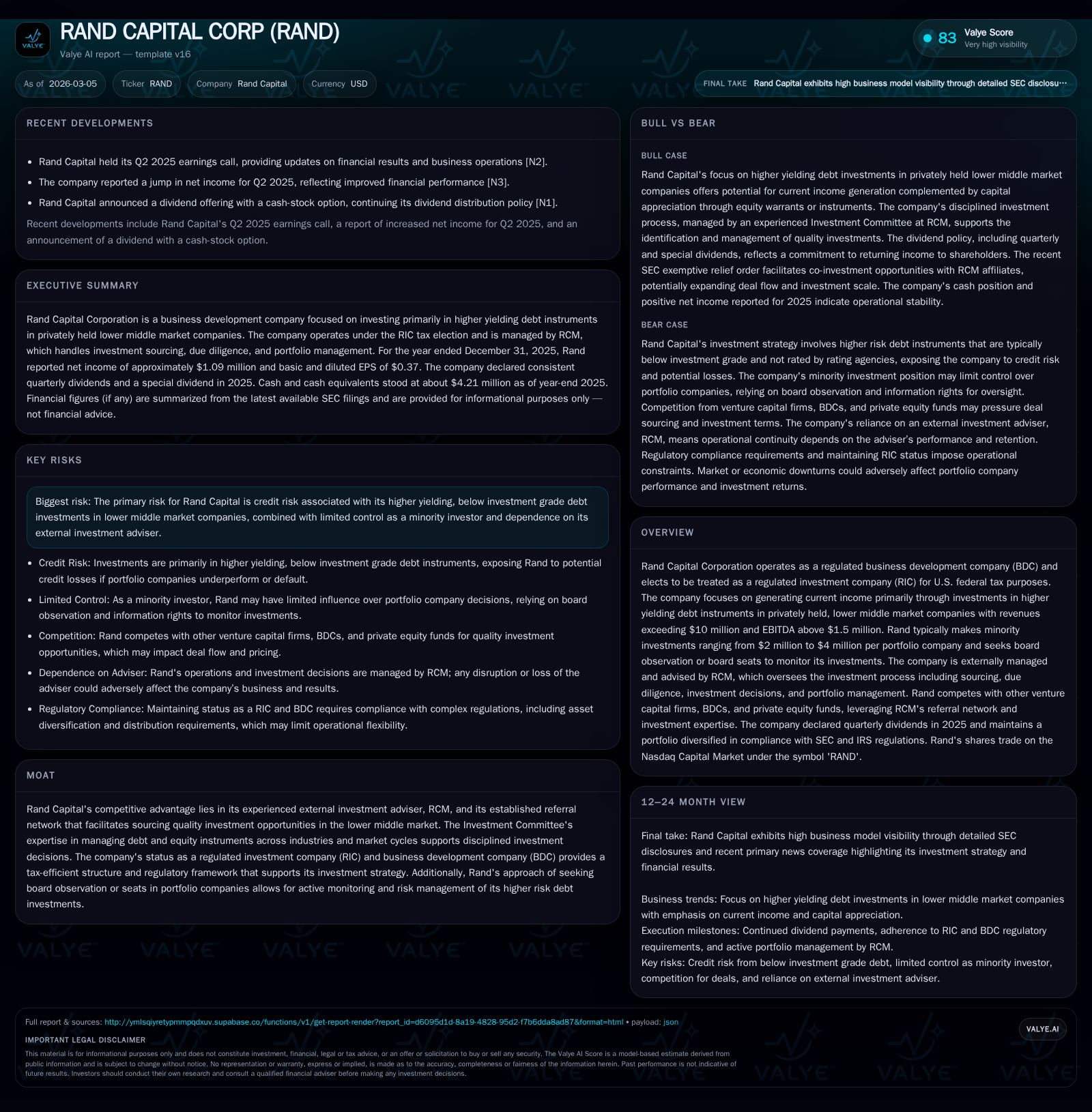

Rand Capital Corporation has transitioned its investment approach toward higher yielding debt instruments primarily targeting privately held lower middle market companies. This strategic evolution is reflected in its financial performance rebound, notably a return to positive net income for FY2025 after a loss in FY2024, supported by RCM’s external management expertise and established referral network. The company maintains disciplined portfolio sizing and governance protocols, including board observation rights, to mitigate risks tied to below investment grade debt investments. Dividend consistency and capital allocation remain focal points, with recent special dividends underscoring income distribution strategies. Key risks persist around credit exposure and limited control as a minority investor, necessitating close monitoring of portfolio and regulatory developments.

From Equity Struggles to Debt Focus: Historical Growth Analysis

Rand Capital's recent financial trajectory underscores a strategic pivot from equity holdings towards higher yield debt instruments focused on privately held lower middle market companies. In fiscal year (FY) 2024, the company posted a net loss of approximately $2.95 million but rebounded in FY 2025 with net income reaching about $1.09 million—a notable increase of nearly 137% year-over-year [F1]. This return to profitability reflects Rand's strategic shift post-transaction described in its Form 10-K to prioritize current income generation through higher yielding debt investments structured by its external adviser RCM [S1].

Operating cash flow (CFO) presents a contrasting picture; despite positive net income in FY 2025, CFO declined by roughly 27% year-over-year from about $15.3 million to $11.25 million, illustrating typical BDC cash flow volatility where timing differences influence realized liquidity differently than accounting profits [F1]. This divergence highlights the ongoing transition away from equity-like returns toward a more stable but yield-focused debt strategy.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Net YoY |

|---|---|---|---|

| 2025 | 1 | 11 | +136.9% |

| 2024 | -3 | 15 | -370.5% |

| 2023 | 1 | -8 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | ROE% |

|---|---|---|

| 2025 | 7 | 2.1 |

| 2024 | 2 | -4.5 |

| 2023 | 3 | 1.8 |

Source: SEC companyfacts cache [F1].

Figures in millions USD; data sourced from [F1].

The External Adviser Advantage and Investment Process at Rand

Rand operates as an externally managed BDC with RCM acting as its investment adviser and administrator under agreements renewed most recently in late 2025 [S6][S23]. RCM’s remit encompasses end-to-end investment responsibilities—from sourcing via an established referral network including bankers, lawyers, and accountants, through rigorous due diligence and Investment Committee approval processes, to active portfolio management.

The Investment Committee consists of seasoned professionals with expertise across industries and credit instruments, providing Rand a competitive advantage in identifying and managing risk-adjusted opportunities within the lower middle market segment [S6][S10]. Their evaluation includes business plans, operational reviews, customer/supplier references alongside pricing and security structuring deliberations.

RCM’s governance strategy includes seeking board observation rights or board seats when necessary allowing proactive monitoring—a critical feature given Rand’s minority investor position yet exposure to relatively high-risk privately negotiated debt claims [S6]. Fees payable combine base management fees and incentive fees aligned with performance metrics balancing manager motivation against shareholder interests.

Evaluating the Portfolio: Target Markets and Investment Size

Rand focuses investments on privately held lower middle market companies with committed management teams reporting revenues exceeding $10 million and EBITDA greater than $1.5 million per guidelines outlined in filings [N1][S6]. Lending primarily targets growth capital needs or ownership transition financings.

Initial investments typically range from $2 million to $4 million per issuer—enabling meaningful minority stakes without overconcentration issues regulated by SEC mandates governing BDC diversification thresholds [S6]. Instruments are generally unsecured or subordinated debt expected to be unrated but below investment grade based on company disclosures.

Risk management incorporates statutory provisions such as seeking board observation or board seats when appropriate facilitating significant managerial assistance consistent with BDC rules for qualifying assets while imposing disciplined oversight despite limited control position [N1][S6]. Co-investment opportunities occur pursuant to SEC exemptive relief orders permitting simultaneous terms with affiliated parties subject to Board majority approvals enhancing transparency within RCM-related transactions [S5].

Yielding Income: Dividend Trends and Capital Return Strategies

A hallmark of Rand’s appeal lies in its stable dividend policy paired with opportunistic special dividends reflecting realized gains or accumulated distributable earnings.

In calendar year 2025, dividends were consistently paid at $0.29 per share each quarter followed by a $0.56 per share special dividend at Q4 end evidencing steady current income generation complemented by episodic return of capital or excess profit distribution [N1][S6]. Prior large special dividends include a notable $4.20 per share stock-cash combination in late 2024 reinforcing commitment to meet Annual Distribution Requirements for favorable RIC tax status [S5].

Dividends paid surged markedly from roughly $2.14 million in FY2024 to approximately $7.28 million in FY2025 amid recovering earnings suggesting increased payout capacity supported by improved operating results despite some decline in cash flow metrics [F1]. This aligns with broader BDC practice prioritizing distributions derived predominantly from recurring interest income rather than capital gains given cyclical portfolio liquidity dynamics.

No significant share repurchases were reported during the latest fiscal periods reflecting sector norms where leverage constraints limit buybacks but liquidity balances remained healthy ensuring continued dividend coverage without undue strain [S27][S28].

Regulatory Compliance and Risk Management Measures

Rand maintains registration as a Business Development Company (BDC) under the Investment Company Act of 1940 electing Regulated Investment Company (RIC) tax treatment since January 2020 enabling pass-through taxable income benefits essential for its dividend-based model [S18][S21]. Compliance encompasses strict diversification requirements—minimum qualifying assets thresholds—and public disclosure obligations ensuring investor protection.

The company benefits from updated SEC exemptive relief orders allowing co-investments alongside RCM affiliates conducted on equal terms subject to Board oversight including required majority vote conditions designed to prevent conflicts of interest while leveraging affiliated deal flow advantages [S5]. These policies are buttressed by compliance procedures overseen by chief compliance officers for both Rand and RCM ensuring adherence.

Managerial assistance is explicitly extended through board participation or observation conferring operational counsel beyond mere capital provision aligning investments with portfolio company success principles demanded under regulations governing BDC "qualifying assets" definitions and supervisory duties [S20].

Capital Structure Dynamics and Liquidity Position

As of December 31, 2025, Rand had no senior securities outstanding negating asset coverage ratio calculations traditionally referenced under Section 61(a)(2) of the 1940 Act; prior compliance indicated a comfortable buffer above minimum coverage thresholds before retiring such senior notes [F1][S8]. Cash and equivalents totaled approximately $4.2 million reflecting prudent liquidity reserves relative to portfolio exposure supporting scheduled distributions and operating expenses without need for additional borrowings or leverage buildup [F1][S27].

The absence of senior secured indebtedness simplifies financial structuring though it may limit gearing benefits common among peer BDCs engaging more actively with debenture issuance; however this conservative posture reduces fixed charge obligations enhancing dividend sustainability under volatile credit cycles [S8][S27].

Share repurchases remain negligible consistent with management strategy focusing on organic portfolio growth rather than capital contraction during current market environment [S28].

Risks in Below-Investment-Grade Lending: Credit and Control Challenges

Principal risks stem from inherent credit uncertainties accompanying non-investment grade debt concentrated within lower middle market companies characterized by less liquidity access, opacity relative to public counterparts, and sensitivity to economic fluctuations [S9][S22]. As a minority lender holding junior or mezzanine debt positions without controlling equity stakes, Rand faces potential limitations on enforcement remedies or restructuring influence absent board representation—an important mitigant it actively pursues via seat acquisition or observation rights supporting early intervention capabilities.

Dependence on RCM as an external manager introduces operational risks including possible agent conflicts since RCM services other clients; however contractual indemnifications shield Rand partly from negligence claims barring willful misconduct transferring certain managerial risks while aligning incentives through performance-based fees contingent on realized investment inflows [S16][S19][S23].

Downward mark-to-market adjustments impacting accrued unpaid income-based fees also reflect credit impairment sensitivities translating into volatile fee accruals differentiating accounting earnings from actual cash realizations underscoring earnings quality considerations common among BDCs focused on subordinated credit instruments.

What to Watch: Upcoming Milestones and Potential Catalysts

Although explicit forward guidance remains absent through early March 2026 filings, stakeholders should monitor:

- Continuity of steady quarterly dividends including recurrent special dividends signaling distributable earnings health given tax-driven distribution mandates (notably maintaining Annual Distribution Requirement compliance) [N1][S3]

- Portfolio growth evidenced by follow-on investments potentially derived from preferred rights such as warrants supporting revenue ramping alongside exit outcomes yielding capital gains influencing incentive fee accruals positively or negatively depending on realized valuations [S10]

- Regulatory changes particularly surrounding co-investment exemption renewals or modifications impacting RCM-aligned transactions affecting Rand’s deal sourcing moats enforced via Board majority approvals guarding shareholders’ interests [S5]

- Liquidity profile shifts influenced by capital calls support from new senior notes issuance or internal free cash flow efficiency reflecting evolving balance sheet leverage strategy balancing growth ambitions versus risk tolerance boundaries observed historically [F1][S8]

- Broader credit cycle movements within lower middle market echoing macroeconomic conditions possibly affecting portfolio asset quality thus requiring reassessment of underwriting conservatism underpinning future profitability outlooks.

These factors frame a watchlist balancing prudent risk oversight against pursuit of enhanced current income characteristic of Rand’s repositioned business model emphasizing higher-yielding debt assets.

This analysis consolidates publicly available financial data from SEC filings including Form 10-Ks/10-Qs supplemented by company disclosures while adhering strictly to presented factual information without offering investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments