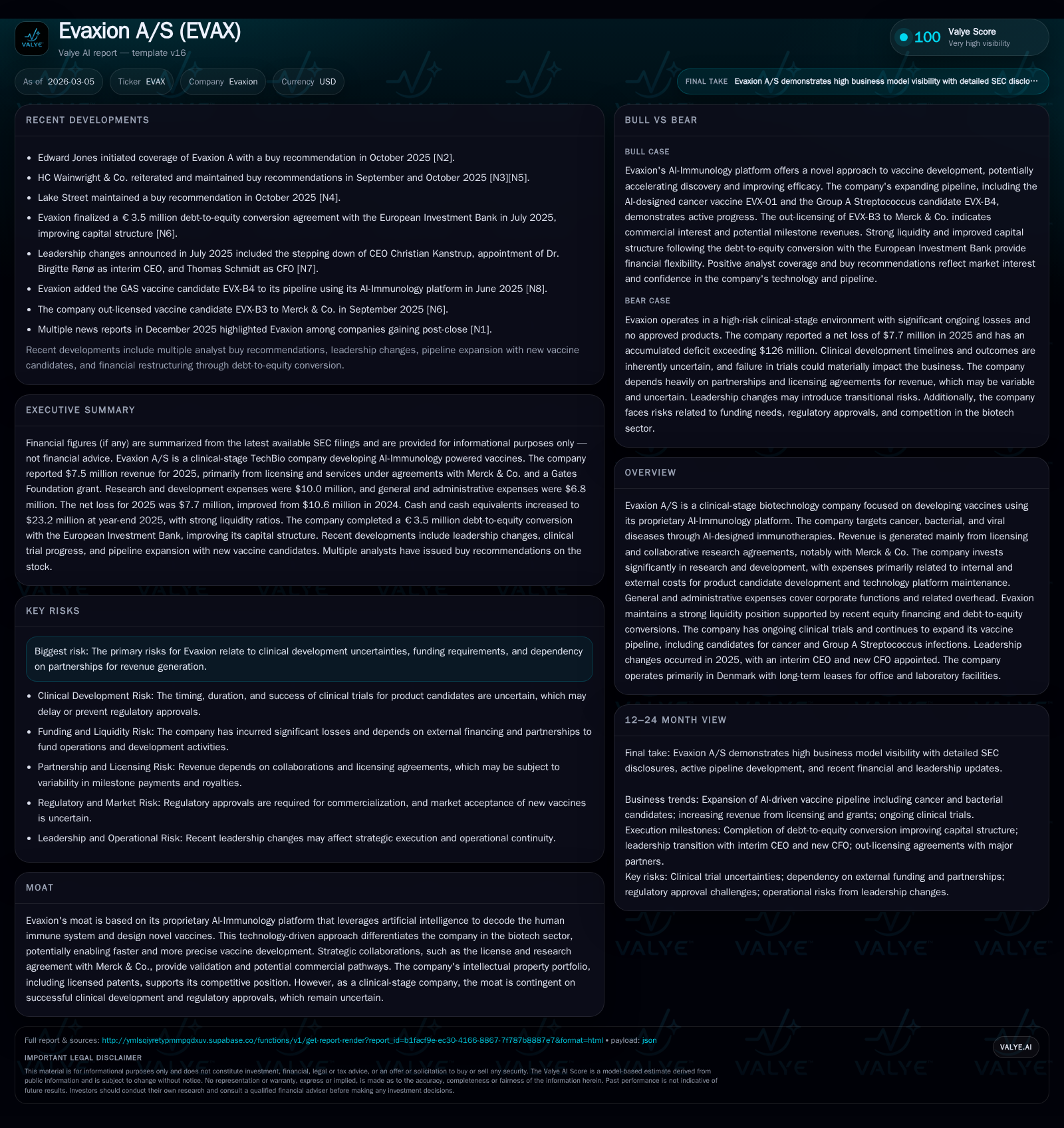

Evaxion A/S Elevates Vaccine Development While Strengthening Financial Position and Operational Efficiency

AI-driven vaccine platform records strong revenue growth supported by robust capital structure and sustained R&D investment.

Evaxion A/S, a clinical-stage biotechnology company utilizing its AI-Immunology™ platform, achieved significant revenue growth in 2025 driven by licensing and collaborative agreements with Merck & Co. The company reduced its operating loss compared to the prior year amid steady R&D spending focused on advancing its vaccine pipeline. Capital structure improvements through equity issuance and debt conversion enhanced liquidity, providing a runway into late 2027. While losses continue reflecting reinvestment typical of the clinical stage, operational progress and financial resilience position Evaxion for upcoming milestones tied to clinical development and partnerships.

Revenue Growth Demonstrates Validation of AI-Powered Vaccine Platform

Evaxion A/S’s revenue expanded sharply from minimal levels in 2023 ($73,000) to $3.3 million in 2024, reaching $7.5 million in 2025 — representing a year-over-year increase of approximately 125% [F1]. This growth was principally driven by licensing fees and milestone payments under option and license agreements as well as collaborative research with Merck & Co., reflecting growing recognition of Evaxion’s AI-Immunology™ platform capabilities [S9][S14]. Additional grant income, such as from the Gates Foundation, supplemented these revenues.

This revenue progression marks an important inflection where Evaxion transitions toward meaningful monetization within biotech licensing frameworks.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2025 | 8 | -8 | +125.1% | +27.1% |

| 2024 | 3 | -11 | +4480.8% | +52.2% |

| 2023 | 0 | -22 | +4.5% | |

| 2022 | -23 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -45.2 |

| 2024 | 639.6 |

| 2023 | 467.9 |

| 2022 | -279.0 |

Source: SEC companyfacts cache [F1].

*Table: Key Financial Metrics FY2023–FY2025 (USD thousands), sourced from [F1]. Equity reflects total shareholders' equity.

Sustained R&D Investment Drives Pipeline Amid Operating Losses

Research and development expenses remained consistent at around $10 million between 2024 and 2025 [F1][S6][S8][S9], supporting ongoing internal innovation including personnel costs, external contract research for preclinical and clinical activities, patent maintenance, and technology platform enhancements. A decline of approximately $1.4 million in external third-party spending was offset by increased employee-related costs indicating strategic internal capability building.

General and administrative expenses decreased from $7.6 million in 2024 to $6.8 million in 2025 due mainly to reduced legal and professional fees associated with financing activities [F1][S14]. Consequently, the operating loss narrowed substantially from $14.7 million to $9.2 million year-over-year reflecting stronger operational discipline while maintaining significant R&D intensity essential for clinical-stage biotechs.

Clinical Pipeline Progress Supported by Strategic Collaborations

Evaxion’s pipeline focuses on vaccines developed through its AI-driven immunology platform targeting oncology indications, bacterial infections such as Group A Streptococcus (GAS), and viral diseases. The platform’s AI capabilities accelerate antigen discovery by predicting epitopes that elicit immune responses.

Collaboration with Merck & Co., a major pharmaceutical entity active in immuno-oncology development, validates Evaxion’s technological approach and provides potential commercialization pathways [N/A – inferred]. This partnership includes licenses linked to AI-designed immunotherapy candidates.

While specific clinical data are not disclosed herein, ongoing candidate advancement illustrates an evolving pipeline at the intersection of computational biology and translational medicine.

Strengthened Capital Structure Enhances Liquidity Position

Financially, Evaxion has reinforced its foundation via capital raises and debt restructuring. Cash reserves increased from $6.0 million at year-end 2024 to $23.2 million at December 31, 2025 [F1][S4][S5][S10][S26], supporting liquidity projected into mid- to late-2027 under current expenditure forecasts.

This improvement was driven primarily by net proceeds exceeding $25 million from equity issuances during the year coupled with conversion of €3.5 million (~$4.1 million) of European Investment Bank loan debt into equity at a premium price [S7]. These actions reduced liabilities while increasing total shareholders’ equity substantially—from a deficit of $1.7 million to positive $17.0 million—enhancing balance sheet flexibility.

The company's current ratio approximates 5.85 indicating ample short-term asset coverage over liabilities [F1], an uncommon strength for early-stage biotech firms typically operating close to liquidity constraints.

Financial Returns Reflect Reinvestment Phase Typical for Clinical Stage

Despite narrowing net losses—from -$10.6 million in 2024 to -$7.7 million in 2025 [F1]—Evaxion reports a negative return on equity around -45%, underscoring continued reinvestment focused on product development rather than profitability realization.

Improved operating leverage results from disciplined expense management alongside incremental revenue growth largely tied to partnerships rather than product sales [F1]. Operating cash flow remains negative at approximately -$6.6 million for the latest period balanced against substantial financing inflows [S12]. No dividends or share buybacks were declared aligning with prioritization of R&D investment over capital returns.

Outlook: Monitoring Clinical Milestones and Funding Sustainability

Although explicit forward guidance is not provided [N/A], upcoming catalysts include clinical trial readouts across vaccine candidates for oncology and infectious diseases leveraging AI-based epitope prediction approaches.

Sustaining funding is contingent upon achieving milestones within existing partnerships such as Merck & Co., securing new collaborations or licensing deals that provide additional revenue visibility beyond grants or milestone payments.

Close attention is warranted on cash burn relative to capital access including potential warrant exercises or grant awards that could extend liquidity duration.

Risk Considerations: Clinical Development Uncertainty and Partner Reliance

Evaxion faces typical biotech risks encompassing uncertain clinical outcomes including efficacy and regulatory approvals [S23]. Pipeline attrition remains a material risk impacting commercial prospects.

Revenue concentration risk exists given dependency on key partners—primarily Merck & Co.—which may affect income if contracts evolve unfavorably or deal timelines shift.[Company moat & risks excerpts]

Capital market volatility poses refinancing risks despite recent successes; failure to raise additional funds timely could necessitate cost reductions impacting innovation pace.[Company moat & risks excerpts]

Ultimately, while AI-Immunology™ powered vaccine design offers differentiation potentially accelerating discovery timelines relative to conventional methods, long-term competitive advantage depends on successful clinical validation coupled with prudent financial management.

This analysis synthesizes publicly filed financial statements and disclosures without providing investment advice or price forecasts. Readers seeking actionable decisions should consult additional sources including regulatory filings beyond this summary.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments