flyExclusive's Fiscal Turnaround: Evaluating Growth Drivers and Legal Headwinds

flyExclusive shows marked financial recovery while managing tight liquidity and significant litigation challenges.

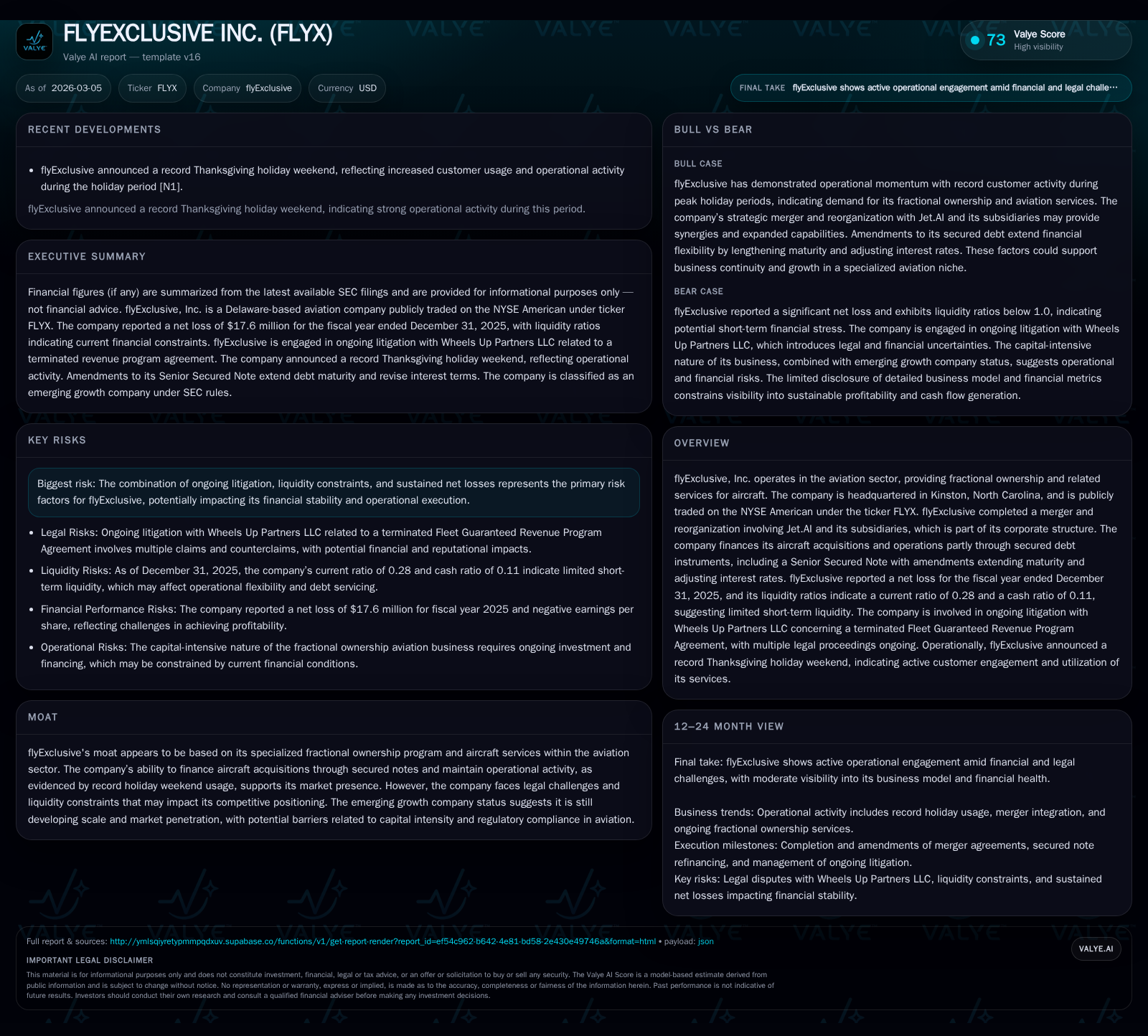

flyExclusive, an emerging player in the fractional aviation ownership sector, has demonstrated improving operating and net income trends from 2022 through 2025 despite substantial losses and negative equity. Its operational momentum is powered by a specialized fractional ownership program and a strategic merger with Jet.AI. However, persistent legal disputes with Wheels Up Partners LLC present sizable risks to liquidity and management focus. The firm’s capital structure relies heavily on secured debt with recent amendments extending maturities but maintaining high interest rates, coinciding with limited short-term liquidity metrics. Going forward, watch for legal resolutions, liquidity events, and integration milestones to gauge sustainability of growth.

From Losses to Recovery: Historical Financial Performance Trends

Over the period from fiscal year (FY) 2022 through FY2025, flyExclusive experienced a pattern of improved operating results despite remaining unprofitable. Operating income was -$4.1 million in FY2022 before deteriorating sharply to -$82.8 million in FY2024 and then improving by nearly 43% to -$47.2 million in FY2025 [F1]. This suggests an inflection where operational efficiencies or revenue streams began absorbing cost structures more effectively.

Net income followed a similar trajectory: after modest profits of $3.7 million in FY2022, the company swung into losses of -$21 million in FY2024 before narrowing the net loss to approximately -$17.6 million in FY2025 [F1]. Despite this progress, equity ended deeply negative at roughly -$327 million as of FY2025 due to accumulated losses and investments [F1].

Cash flow trends were volatile; operating cash flow (CFO) improved substantially to $6.7 million positive in FY2025 from a negative $10.9 million outflow the prior year [F1]. Capital expenditures (Capex) declined from over $83 million in FY2023 to about $31 million last year [F1], indicating a more cautious investment pace post-merger integration.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -18 | 7 | -47 | 31 | +16.5% |

| 2024 | -21 | -11 | -83 | 57 | -7148.2% |

| 2023 | 0 | 9 | -51 | 84 | -91.8% |

| 2022 | 4 | -1 | -4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -24 | 5.4 |

| 2024 | -68 | 9.0 |

| 2023 | -75 | 0.6 |

| 2022 | -27.7 |

Source: SEC companyfacts cache [F1].

The scale of negative equity points to underlying capital intensity and past losses creating leverage against financial flexibility [F1].

Operational Drivers Behind Recent Improvement

flyExclusive focuses on a specialized fractional aircraft ownership program serving a niche within private aviation that balances service quality with flexibility. The company reported record holiday weekend usage indicative of increased customer engagement and efficient fleet utilization despite broader economic pressures [S7].

A key strategic milestone is the merger with Jet.AI finalized through planned transactions culminating in early 2026 [S21]. This reorganization aims to consolidate complementary capabilities including fleet expansion and technology integration for enhanced booking and service efficiency.

Aircraft acquisitions have been financed using secured debt instruments which allow fleet growth while deferring upfront capital requirements [S13]. Such arrangements enable scaling under tight liquidity but impose fixed obligations requiring consistent utilization levels for profitability.

Ongoing Litigation Risks

flyExclusive faces protracted legal conflict with Wheels Up Partners LLC regarding termination of the Fleet Guaranteed Revenue Program Agreement dated November 2021 [S4], [S5], [S6], [S8]. Following termination notice due to alleged breaches by Wheels Up—including unpaid amounts—Wheels Up filed multiple lawsuits alleging wrongful termination.

The dispute has involved procedural motions across federal and state courts with jurisdictional challenges continuing through late 2023 into 2025 [S6]. Additional claims include unfair trade practices and fraudulent misrepresentation brought by Wheels Up [S8]. flyExclusive has denied claims and filed counterclaims seeking damages exceeding $75,000.

This litigation imposes financial uncertainties including potential settlement costs or legal expenses as well as management distraction from core operations.

Liquidity and Capital Structure

At fiscal year-end FY2025 flyExclusive had current assets totaling approximately $74.4 million against current liabilities of about $270 million resulting in a current ratio of just 0.28—a sign of significant short-term liquidity pressure [F1]. Cash & equivalents were about $29.3 million at that date.

The company carries secured debt including a Senior Secured Note initially issued for approximately $25.8 million primarily for fleet financing [S13]. Amendments extended maturity to January 26, 2028 but set interest rates between 13% and 15%, increasing cash flow strain [S27]. The note requires quarterly principal repayments starting mid-2026 with no revolving advance feature available after amendments.

Capital Allocation: Debt Focused; No Returns Reported

There are no reports or disclosures indicating dividends or share repurchases through early-2026 filings [S9],[S10],[S12],[S14],[F1]. With net losses against deeply negative equity nearing -$327 million at FY25-end and free cash flow (operating CFO minus capex) roughly estimated negative at -$24 million annually [F1], return metrics like ROE are distorted — approximate ROE stands near +5.4% due to negative book value skewing calculations.

The capital allocation strategy centers on managing secured debt amortization rather than shareholder returns.

Growth Outlook Amid Industry Challenges

As an emerging growth company within a capital-intensive private aviation market segment focused on fractional ownership services enhanced by technology platforms such as Jet.AI’s integration,[S21] flyExclusive targets scalable service models balancing fleet expansion with digital booking efficiencies.

However regulatory complexities around aircraft operations combined with high upfront capital requirements constrain rapid scaling absent sustained external funding or margin improvement.

Competitive pressures persist from charter operators and other fractional providers backed by stronger balance sheets.

Key Milestones To Monitor

- Resolution timeline and financial impact of ongoing Wheels Up litigation;

- Liquidity events including potential refinancing beyond January 2028 maturity or equity raises;

- Realization of synergies from Jet.AI merger affecting fleet utilization and customer retention;

- Sustained seasonal usage trends supporting fixed cost absorption;

- Regulatory developments impacting fractionation programs or cost structures.

These factors will be critical indicators for assessing whether recent improvements can translate into sustainable profitability amidst structural headwinds.

Disclaimer: This report is prepared solely for informational purposes referencing publicly available data sources without any express or implied recommendation regarding securities transactions related to flyExclusive Inc. Readers should perform their own due diligence or consult professional advisors prior to acting upon any information contained herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments