Cleveland-Cliffs Inc. 2025 Review: Navigating Steel Market Pressures and Strategic Realignment

A detailed examination of Cleveland-Cliffs’ 2025 financial challenges, strategic initiatives, and market context within North American steel production.

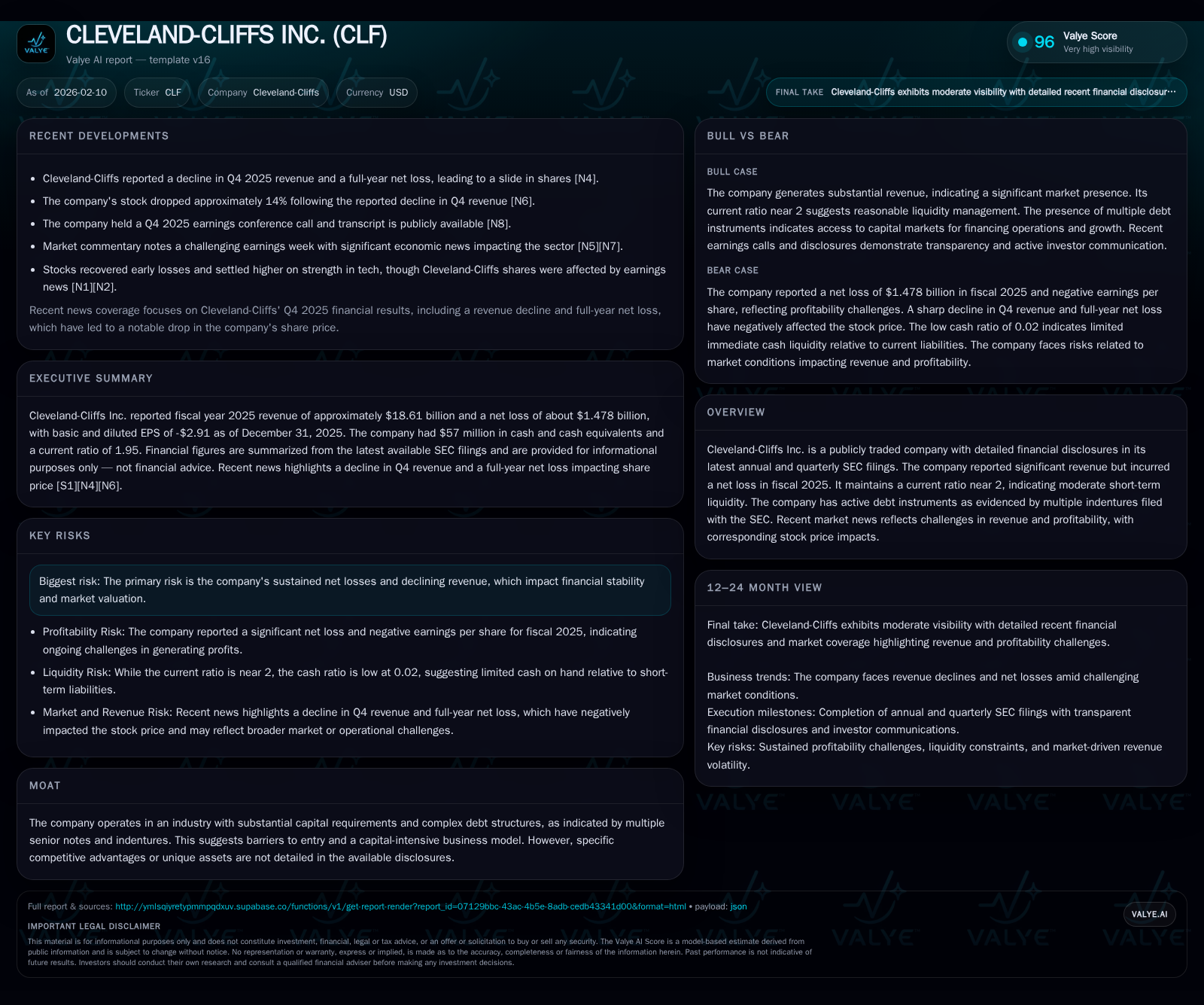

Cleveland-Cliffs Inc. faced a difficult 2025 marked by a net loss of $1.48 billion amid declining revenue and ongoing market headwinds in the steel industry. The firm took steps to optimize its operational footprint, forge strategic partnerships, and extend debt maturities, positioning for long-term competitiveness despite near-term pressures. Steel tariffs and North American automotive industry demand remain critical external factors influencing outcomes. Operational efficiencies and new commercial contracts with automotive OEMs underpin optimism for recovery.

Introduction

Cleveland-Cliffs Inc., a leading North American steel producer primarily serving the automotive sector, reported a challenging fiscal year in 2025. Despite navigating a turbulent macroeconomic landscape marked by recessionary signals and fluctuating steel demand, the company undertook strategic initiatives aimed at consolidating its market position and enhancing operational efficiency. This analysis synthesizes the company’s financial results, operational adjustments, market dynamics, risks, and strategic outlook as detailed in their latest SEC filings and supplemented by recent market commentary.

Financial Performance Overview

The company's revenue in 2025 declined to approximately $18.6 billion (F1) from $19.2 billion in the previous year, signaling contraction amid weaker steel demand and competitive pressures [N7]. Operating costs outpaced revenues, culminating in an operating loss of $1.58 billion compared to a loss of $763 million in 2024 ([S1]). The net loss attributable to shareholders deepened significantly to $1.48 billion.

Liquidity remains adequate though constrained; the current ratio stands at about 1.95 ([F1]), indicating the company's ability to cover short-term obligations but highlighting limited cash reserves ($57 million at year-end) relative to liabilities ([S1]). Long-term debt increased slightly to approximately $7.25 billion but senior note maturities were extended beyond 2029 enhancing refinancing flexibility.

Selling general and administrative expenses rose modestly while unit costs decreased year-over-year—reflecting effective cost management despite top-line declines [S1]. Restructuring charges reduced compared to prior years due to completion of asset rationalizations.

Operational and Strategic Initiatives

In response to ongoing market softness, Cleveland-Cliffs optimized its asset footprint by idling or permanently closing six operations during 2025 ([S1]). These moves targeted underperforming units while preserving flat-rolled steel capacity considered core for automotive supply commitments.

A key strategic highlight is the Memorandum of Understanding signed with POSCO—a prominent global steelmaker based in Korea—which may lead to collaboration opportunities leveraging Cliffs’ North American presence [S1]. The prospect aligns well with Cleveland-Cliffs’ efforts to strengthen its competitive moat through alliances rather than organic expansion alone.

Multi-year fixed price contracts with major automotive OEMs secure stable demand for high-margin product lines amidst industry volatility. Despite North American light vehicle production slipping slightly from prior years (15.3 million units versus pre-COVID averages near 17 million), these long-term arrangements provide revenue visibility [S1]. Notably, Cliffs successfully collaborated on producing defect-free exposed automotive steel stamped parts using existing aluminum-forming equipment—showcasing technical innovation that caters directly to client manufacturing processes.

Capex discipline was evident as capital expenditures fell by roughly 19%, underscoring prioritization of cash flow management while investing selectively such as commissioning a new bright anneal line operational facility [S1].

Industry and Market Environment

The steel sector in North America has been shaped heavily by government intervention and trade policies. The imposition of steep tariffs (50%) on imported steel under the Trump administration profoundly altered competitive dynamics by elevating domestic pricing power ([S1], [N13]). While this benefited Cleveland-Cliffs through reduced import volumes and higher Hot Rolled Coil (HRC) prices—averaging around $851/ton (10% above previous year)—demand remained subdued due to macroeconomic headwinds.[S1]

Canadian operations experienced pressures from dumped imports priced below market value but saw some relief with newly enacted tariff-rate quotas aiming at protecting local industry margins beginning mid-2025 [S1]. Continued government support on both sides of the border remains crucial as global overcapacity issues persist worldwide.

Automotive demand—Cleveland-Cliffs’ primary revenue driver—was slightly weaker than usual yet shows signs of bottoming out as interest rates gradually ease [S1]. Efforts toward reshoring manufacturing driven by recent U.S. economic policy promises incremental steel demand growth over medium term.

Risk Factors

Persistent net losses weigh heavily on financial stability and shareholder value; compounded by macroeconomic uncertainties including potential recessionary conditions affecting customer industries [S1]. Heavy indebtedness requires careful management amid volatile commodity prices and cyclical end-use markets.

Supply chain disruptions or raw material cost spikes could undermine margin improvement efforts despite operational efficiencies. Additionally, evolving greenhouse gas regulations pose compliance costs risks though current disclosures suggest measurement standards are still developing with inherent uncertainties [S2].

Competition from lower-cost foreign producers employing subsidized tactics continues as a structural challenge despite tariffs aimed at leveling the playing field [S1]. Failure to maintain regulatory protections or adapt rapidly may accelerate margin erosion.

Competitive Moat Considerations

The capital-intensive nature of integrated steel production combined with complex debt structures creates high entry barriers for new competitors [S1]. The extended maturity profile of debt instruments provides some breathing room while enabling capital deployment for modernization.

Cliffs’ position as a North American leader in flat-rolled steels tailored toward automotive applications establishes differentiated credibility against commoditized imports. The partnership discussions with POSCO further aim at leveraging complementary assets and scale globally, potentially solidifying their competitive stance beyond geographic boundaries.

Nevertheless, no singular proprietary technology or unique input advantage is highlighted clearly; thus competitive sustainability relies heavily on scale efficiencies, customer relationships, tariff protections, and technical collaboration achievements like stamping innovations.

Management Outlook and Investor Sentiment

Management stresses the transitional nature of current challenges and highlights successful safety improvements alongside execution on strategic contracts as foundational progress [S1]. Market reaction following Q4 earnings was negative on revenue misses resulting in share price declines nearing 14% as investors digest ongoing profitability concerns [N3],[N13].

Looking forward, slower easing of interest rates combined with sustained tariff regimes may stabilize domestic demand while new governmental manufacturing policies could catalyze growth opportunities over ensuing years.

Conclusion

Cleveland-Cliffs confronts a complex intersection of macroeconomic adversity, policy-driven trade environments, and internal restructuring imperatives. Its sizeable net losses contrast with noteworthy advances in operational discipline, safety records, contractual security within the automotive sector, and strategic global partnership exploration.

While financial stress remains evident through declining earnings and tight liquidity buffers, management’s proactive footprint optimization coupled with tariff-induced market insulation affords some confidence toward medium-to-long term viability.

Investors should monitor evolving trade policies, North American manufacturing trends—particularly automotive—and how Cleveland-Cliffs advances integration efforts with partners like POSCO alongside sustainable cost reductions going forward.

This report is an informational analysis based solely on publicly available data including Cleveland-Cliffs’ SEC filings and relevant market reports. It is not investment advice or an endorsement of any company or security.

Comments