Costamare Bulkers Holdings: Evaluating Growth Dynamics and Capital Discipline Post Spin-Off

Post-spin-off Costamare Bulkers Holdings leverages its dry bulk fleet amid shipping market cyclicality while maintaining robust financial controls.

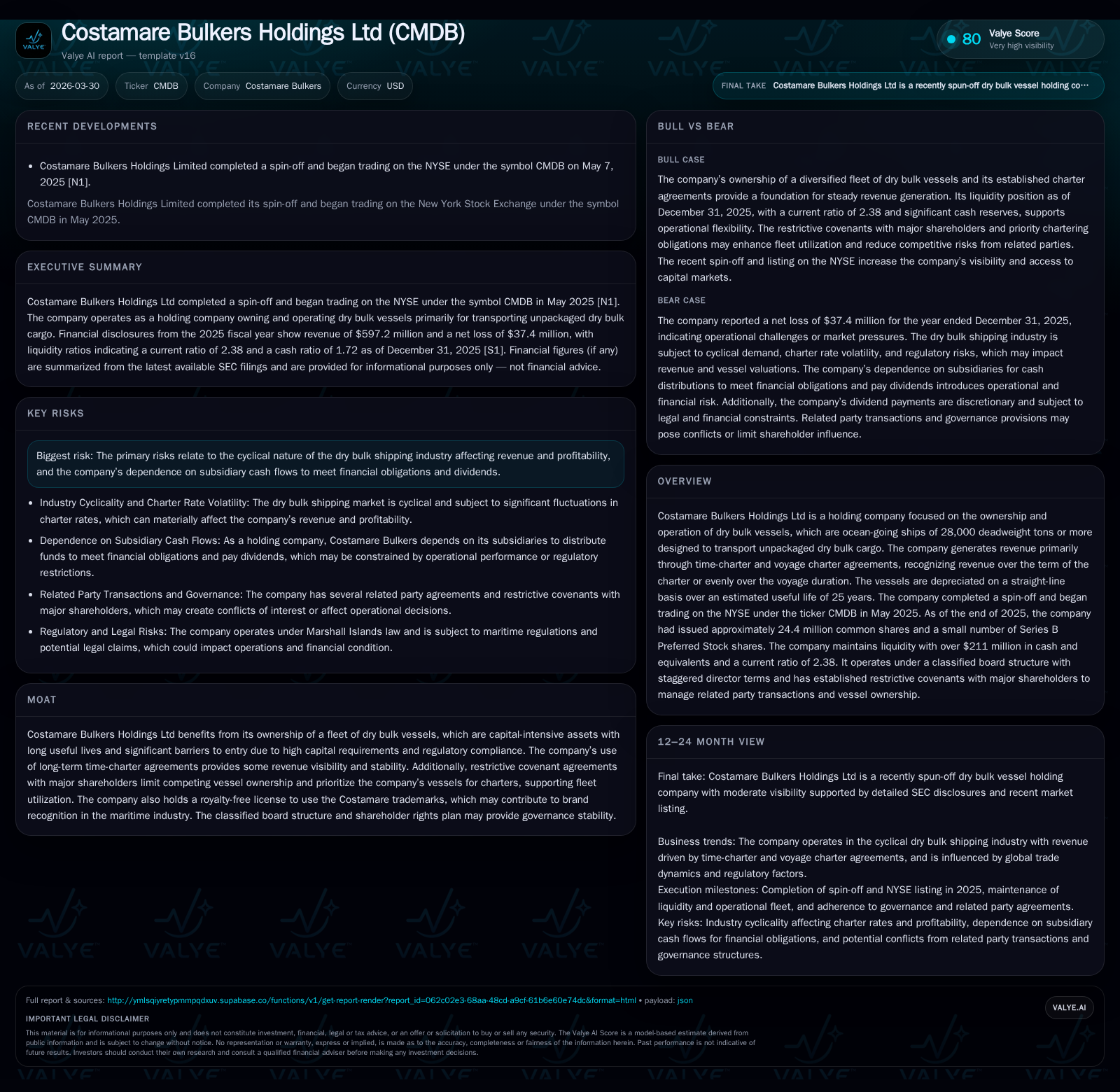

Costamare Bulkers Holdings Ltd entered the NYSE as an independent entity in May 2025, focusing exclusively on owning and operating dry bulk vessels over 28,000 deadweight tons. In its inaugural full year, the company generated $597 million in revenue but recorded an operating loss of $30.6 million amid soft charter markets. The firm’s business model anchors revenue visibility through long-term time-charter agreements, supported by restrictive shareholder covenants that prioritize fleet utilization. With strong liquidity marked by $212 million in cash and a current ratio of 2.38, cost discipline is evident despite negative returns on equity. Key risks include dry bulk market cyclicality and related-party dependencies, while governance structures such as classified boards and shareholder rights plans aim to protect stability.

Spin-Off Milestone and Foundation of Costamare Bulkers’ Business Model

Costamare Bulkers Holdings Ltd emerged as an independent public company when it completed its spin-off from Costamare Inc. in May 2025, debuting on the NYSE under ticker CMDB [S1]. This strategic separation crystallized its focus exclusively on the ownership and operation of dry bulk vessels—specifically ocean-going ships above 28,000 deadweight tons (dwt) engineered to transport unpackaged dry bulk cargo such as coal, iron ore, or grain. The spin-off delineated distinct capital deployment and operational frameworks aimed at capturing value within the cyclical commodity freight sector. Revenue recognition follows the charter contract tenor or voyage progress method depending on time-charter or voyage charters respectively [S1], facilitating predictable cash flow profiles tied to contracted earnings.

This structural realignment positions Costamare Bulkers to cultivate a fleet-centric growth approach, leveraging large capital-intensive assets governed by stringent maritime regulations. The company's depreciation schedule reflects straight-line amortization over an estimated useful life of 25 years for these vessels, standard industry practice providing tangible insight into asset aging [S1].

Historical Revenue and Profitability Trends with Commentary on Market Drivers

In its first full fiscal year post-spin off, Costamare Bulkers reported total revenues of approximately $597 million [F1]. Despite this respectable top-line scale, operating income registered a loss of $30.6 million for 2025, dragged down primarily by prevailing softness in charter rates reflecting global trade headwinds facing the dry bulk sector [F1][S2]. Net income also followed suit with a negative figure close to $37.4 million contributing to a return on equity (ROE) of -5.6% [F1].

The interconnectedness between vessel utilization rates and volatile charter pricing materially influenced margins during the reporting period. Although volume utilization remained stable due to contractual obligations under long-term time charters, average daily time charter equivalent (TCE) rates declined compared to historical averages affecting profitability negatively [S1]. This dynamic underscores the sensitivity of revenue quality not merely to fleet deployment but also cyclical macroeconomic factors shaping commodity demand patterns.

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

Table: Selected Annual Financial Summary for Costamare Bulkers Holdings Ltd (2025 full year) sourced from [F1]

Fleet Utilization, Charter Rate Cyclicality, and Their Impact on Operating Metrics

Fleet utilization remains a critical driver for Costamare Bulkers’ operational performance. The company benefits from restrictive covenant agreements entered with major shareholders, notably Konstantinos Konstantakopoulos and Achillefs Konstantakopoulos. These covenants restrict these principals from owning competing dry bulk vessels exceeding defined deadweight tonnage thresholds or participating directly or through associated entities in rival ownership ventures [S24]. Consequently, Costamare’s vessels receive prioritized opportunities for charters when overlapping availability arises between their fleet and those affiliated with these major shareholders.

Charter rate cyclicality in the dry bulk sector is pronounced; spot market rates can swing widely based on global supply-demand imbalances driven by economic cycles and raw material flows. To mitigate these fluctuations’ accounting impacts, the company employs impairment testing assumptions aligned with ten-year average historical one-year time charter rates rather than short-term market spikes or troughs [S1]. This prudent valuation approach tempers volatility in reported asset values while recognizing underlying shipping cycle realities.

Time charter equivalent (TCE) metrics provide a composite measure reflecting realized voyage revenues minus voyage costs normalized across fixed ship days—integral for comparability both internally among fleet segments and externally against peer benchmarks in maritime finance literature.

Evaluating Asset Impairments and Critical Accounting Policies

Costamare Bulkers applies an extensive two-step impairment test framework upon detecting indications that vessel carrying values may not be recoverable [S1]. The initial step involves calculating undiscounted future net operating cash flows expected from each vessel considering contracted revenue streams from existing time charters combined with conservative estimates based on ten-year historical average rates for unfixed days less forecasted operating expenses including scheduled dry-docking capital expenditures.

If carrying amounts exceed expected undiscounted cash flows (indicating potential impairment), Step Two assesses fair value using Level 2 inputs per fair value hierarchy principles—leveraging available market data validated by third-party valuations [S1]. For fiscal years ended December 31, 2024 and December 31, 2025 no impairment losses were recorded reflecting either prudent procurement timings or resilient asset valuations despite cyclicality [S1]. However, in FY2023 an aggregate non-cash impairment loss of $0.4 million was recognized principally related to two older vessels.

Such rigorous valuation discipline accords transparency essential to investor confidence given fraught macroeconomic shipping conditions underpinning residual value risk exposure.

Projected Growth Trajectory and Revenue Visibility From Time-Charter Agreements

While explicit financial forecasts are absent from public disclosures due to industry unpredictability and spin-off recency [N1][S2], future growth prospects hinge heavily on renewal or extension of long-term time-charter contracts comprising the bulk of quoted revenues. These contracts typically span multiple years offering staggered revenue visibility correlated closely with committed daily hire rates providing resilience against spot downturns.

Management's adherence to contracting vessels primarily under long-term arrangements limits exposure to sudden rate drops though caps upside potential should spot prices rise substantially beyond contracted floors [S1]. New charter awards or re-negotiations are key catalysts observed carefully as indicators for prospective earnings momentum enabling efficient fleet deployment aligned with market cycles.

Balance Sheet Strength: Liquidity, Capital Structure, and Shareholder Restrictions

Costamare Bulkers exhibited robust liquidity at December 31, 2025 represented by $211.8 million in cash and cash equivalents accompanied by a healthy current ratio of approximately 2.38 evidencing comfort meeting short-term obligations without immediate refinancing pressure [F1][S3].

Capital structure accommodates issuance of both common shares totaling roughly 24.4 million outstanding plus limited Series B Preferred Stock shares amounting to just over two hundred units held solely by major shareholder Konstantinos Konstantakopoulos conferring enhanced voting control via weighted voting rights yet no dividend rights or transferable capabilities [S4][S22].

The Series B stock issuance effectively functions as a governance safeguard preventing U.S persons from gaining controlling voting interest beyond stipulated thresholds amidst evolving regulatory contexts potentially affecting port fee regimes particularly involving China [S15][S22]. Restrictive covenants enacted concurrently impose additional business conduct limitations preserving company-first priorities regarding fleet utilization vis-à-vis affiliated parties' shipping assets [S24].

These multi-layered controls exemplify integrated capital stewardship blending liquidity preservation with strategic shareholder alignment across volatile operating climates.

Capital Allocation Review: Dividends, Share Buybacks, and Cash Flow Management

Dividend policy remains cautious reflecting cyclical earnings pressures coupled with holding company status reliant upon subsidiary distributions for cash inflows imperative to meet debt obligations or return capital to shareholders [S6][S16]. Dividend declarations are discretionary per board judgment factoring earnings quality liquidity reserves regulatory compliance alongside anticipated investment needs including potential vessel acquisitions or dry-dock expenditures.

Currently no active share repurchase programs have been reported underscoring conservative capital allocation prioritizing balance sheet strength over financial engineering during early standalone operational phases [S7][F1]. This disciplined approach mitigates downside leverage risks inherent in shipping finance cycles ensuring flexibility amid charter rate volatility.

Key Risks: Industry Cyclicality, Regulatory Landscape, and Related Party Dynamics

Cyclicality remains paramount risk for Costamare Bulkers as episodic supply-demand imbalances influence freight rates directly impacting revenue scale profitability margins leading to earnings unpredictability despite contractual buffers [S15]. Further exposure exists regarding trade protectionism trends particularly involving China whose export-import activities materially affect bulk cargo volumes impacting charter demand prospects.

Regulatory risks center around potential reinstatement of special port fees previously contemplated in certain Asian jurisdictions prompting defensive issuance of Series B Preferred Stock designed both as ownership safeguard mechanism limiting control concentration risks amongst non-U.S investors as well as as contingency against tariff shocks [S15][S22].

Related party transactions especially concerning management service agreements with entities controlled by key shareholders necessitate formal approval protocols overseen by independent directors preventing conflicts while aligning operational integrity with minority investor interests [S13][S24].

Indicators to Watch: Market Charter Rates, Fleet Expansion, and Governance Developments

Investment community focus should remain attuned to trajectory changes in dry bulk one-year average time charter rates serving as primary proxy for future earnings quality given their central role feeding into asset impairment assumptions.

Contract renewals or expansions offer tangible signals about fleet utilization sustainability amid competitive dynamics heightened by restrictive covenant commitments limiting affiliated owner ship options ensuring priority access for Costamare’s vessels.

Additionally monitoring board election results under staggered structure governance reforms post-spin off will shed light on strategic continuity versus emergent shifts potentially affecting capital allocation philosophies or corporate control structures critical during cyclical troughs.

This analysis reflects publicly disclosed information as cited exclusively without providing investment recommendations or price forecasts. Readers should refer directly to official filings for comprehensive data interpretation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments