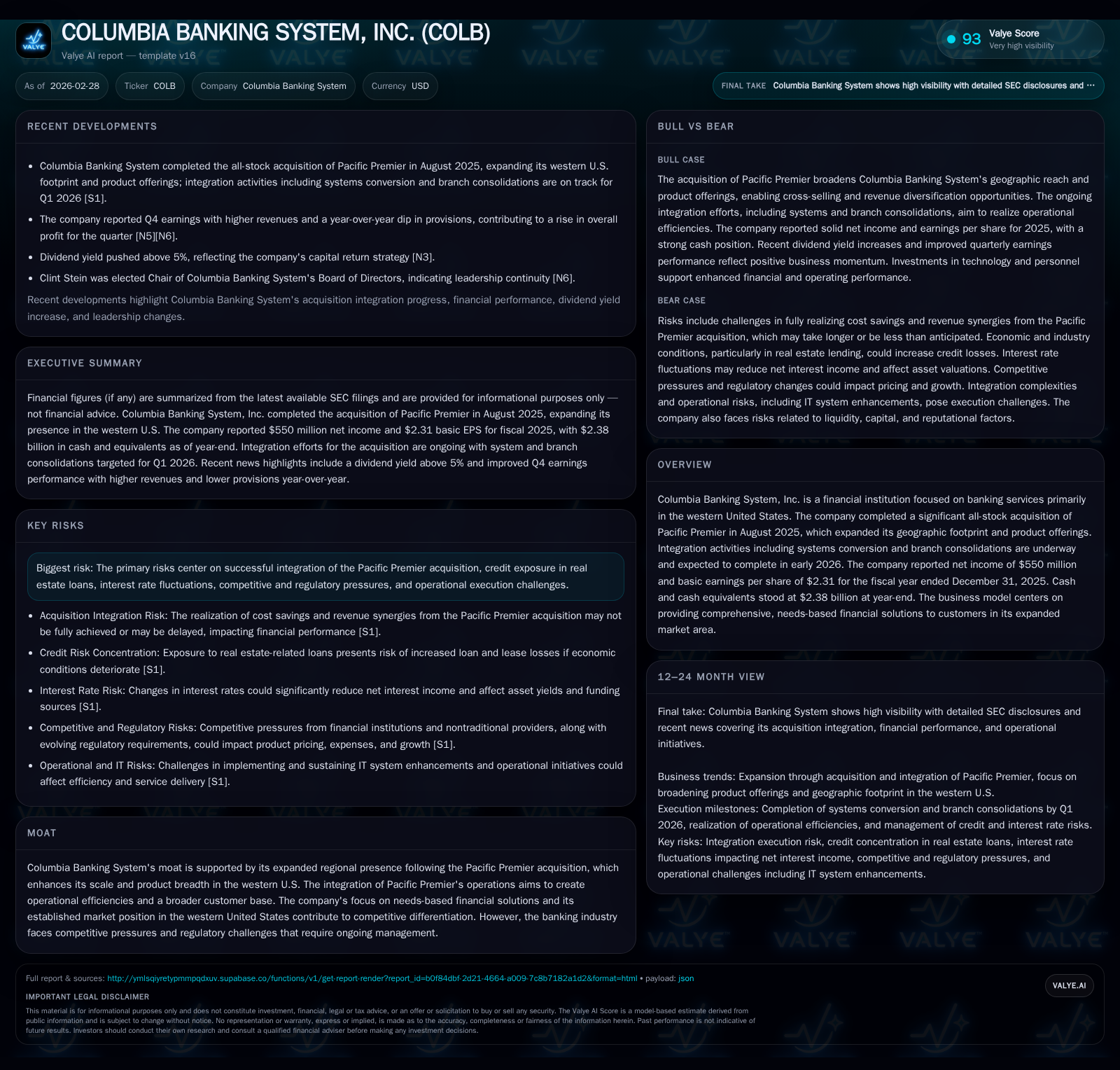

Columbia Banking System Strengthens Western Foothold with Strategic Acquisition

The pivotal Pacific Premier acquisition in 2025 reshapes Columbia’s scale and operational footprint across the western U.S., underpinning growth and capital strategy.

Columbia Banking System’s 2025 results demonstrate robust earnings expansion driven by its transformative all-stock acquisition of Pacific Premier completed in August 2025. This strategic deal enlarged the bank’s regional presence and product offerings, positioning it as a leading financial institution in the western United States. The company reported $550 million in net income for FY25, supported by steady deposit growth, improved loan portfolio diversification, and disciplined credit loss provisioning. Integration efforts are on pace for completion in early 2026 but present execution risks. Capital allocation remains balanced with dividends and buybacks underpinned by strong cash flow generation.

Transformational Acquisition: Completing the Pacific Premier Deal

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 550 | 746 | +3.1% | |

| 2024 | 534 | 659 | +53.0% | |

| 2023 | 349 | 670 | 27 | +39.4% |

| 2022 | 250 | 301 | 7 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 335 | 109 | |

| 2024 | 300 | 6 | |

| 2023 | 270 | 6 | 643 |

| 2022 | 94 | 0 | 293 |

Source: SEC companyfacts cache [F1].

In August 2025, Columbia Banking System completed a material all-stock acquisition of Pacific Premier, effectuating an exchange where Pacific Premier shareholders received 0.9150 shares of Columbia common stock per Pacific Premier share held [S1][S7]. This transaction notably broadens Columbia's geographic footprint across the western United States and enhances product breadth through complementary service capabilities. The acquisition establishes Columbia among the region's leading banking institutions — a strategic objective driven by expanding customer reach and the ability to deliver more comprehensive, needs-based financial solutions.

Post-close integration phases focus primarily on systems conversion and branch consolidation, both underway with targeted completion during the first quarter of 2026. These efforts are centrally coordinated by Columbia's Integration Management Office, reflecting best practices in M&A execution within banking circles where technology platform harmonization and physical footprint rationalization are key to unlocking targeted efficiencies and cross-selling opportunities [S1][S7]. However, such integrations carry inherent execution risk given complexity involving data migration, system compatibility, regulatory approvals, and customer retention amidst branch network adjustments.

Financial Growth and Earnings Drivers Over Recent Years

Columbia’s trajectory from FY22 through FY25 illustrates robust earnings expansion fueled principally by organic growth supplemented recently by acquisition impact. Net income rose from approximately $250 million in FY22 to a record $550 million in FY25 — a compound uplift propelled by a combination of net interest income growth, effective management of provision expenses, and revenue diversification driven by expanded lending and deposit franchises [F1][N3][N14]. The latest year-over-year increase of roughly 3.1% confirms momentum at scale despite macroeconomic headwinds.

Deposit growth remains foundational to funding loans that now encompass a broader mix post-acquisition. The bank reported stable or improving net interest margins supported by strategic loan portfolio rebalancing, even as easing interest rates present repricing pressures [N11]. Concurrently, provisions for credit losses declined year-over-year reflecting cautious underwriting standards amid ongoing real estate and commercial loan reviews by management — important given elevated market sensitivities around CRE valuations [N3][N14]. This prudent allowance approach underscores a conservative stance toward credit risk that guards profitability amid economic uncertainties.

Integration Efforts and Operational Synergies Underway

The post-acquisition period focuses intensively on integrating legacy operations to achieve projected synergies. Major tasks include transitioning to unified information technology platforms through system conversions that require meticulous planning to avoid disruption in transaction processing or customer experience. Branch consolidations aim to eliminate redundancies while optimizing access points — particularly critical where overlapping presences existed pre-deal [S1][S7][N10].

Operational synergy realization hinges on managing employee transitions, systems harmonization timelines, regulatory compliance for combined entities, and retention of key deposit relationships. Banking sector experience cautions that cross-company workflow alignment can test initial projections; hence Columbia’s appointment of an Integration Management Office is neither novel nor casual but reflects governance rigor appropriate for such complex endeavors [N10]. Monitoring progress against milestones will be essential through early 2026.

Strategic Outlook: Navigating Growth and Margin Pressures

Looking ahead into 2026, Columbia faces challenges typical for mid-sized regional banks undergoing transformational deals combined with evolving economic conditions. Loan portfolio management must carefully address real estate exposure concentration risks given potential CRE valuation fluctuations that remain a noted risk factor [S8][S10]. Interest rate easing trends weigh on net interest margin stability; loan repricing cadence will be slower versus funding cost reductions affecting overall asset yield spreads [N11][N10].

Competition appears intensifying from consolidated institutions as well as fintech entrants offering alternative deposit products or digital lending services. Regulatory oversight remains vigilant post-pandemic emphasizing capital adequacy frameworks aligned with Basel III guidance which may influence balance sheet optimization strategies [S8]. Thus Columbia's ability to adapt pricing models dynamically and maintain credit discipline will likely influence its sustainable growth path.

Capital Allocation Focus: Dividends, Buybacks, and Cash Generation

Through FY25 Columbia sustained disciplined capital allocation balanced against expansion needs. Operating cash flow grew meaningfully to approximately $746 million, enabling dividend payments totaling $335 million alongside share repurchases around $109 million — marking a notable acceleration over prior years’ buyback levels [F1][S19][S20]. The board’s commitment is reflected in consistent dividend declarations with the quarterly rate holding steady at $0.37 per common share as recently affirmed [S20].

This translates into a dividend yield breach above 5%, representing both attractive income generation for shareholders and confidence in internal free cash flow sustainability (free cash flow estimated near $719 million after capex) [F1][N13]. Capital returns have been managed without jeopardizing core liquidity reserves maintained at approximately $2.38 billion year-end [F1], signifying financial prudence even amid sizable merger integration expenditures.

Risk Exposure: Credit, Interest Rates, and Competitive Challenges

Material risks emphasize successful execution of integration strategies essential for synergy capture—the timing and scale of which remain somewhat dependent on complex operational factors consistent with recent banking M&A experiences [S8].[S10] Credit exposure is significantly concentrated within commercial real estate loans where macroeconomic variables such as construction activity slowdowns or shifting property valuations could increase problem asset formation [S8].[S6]. Interest rate volatility poses persistent threat to income consistency given potential mismatches between asset yields versus funding costs especially as central bank policies evolve.

Industry consolidation heightens competitive pressures placing stress on fee structures and client retention strategies while regulatory landscapes continue advancing emphasizing stringent capital adequacy and compliance cost burdens—all requiring agile management responses from Columbia leadership teams.[S8] Considering these vectors alongside reputational factors related to merger executions rounds up the core risk profile warranting ongoing close monitoring.

Balance Sheet Metrics: Liquidity, Equity Expansion, and ROE Analysis

Balance sheet dynamics have shifted substantially post-acquisition with total equity ballooning from about $2.21 billion at end-2022 to nearly $7.84 billion at end-2025 reflective of transaction-related equity issuances plus retained earnings accretion [F1].[S4] Cash & equivalents remain robust at $2.38 billion supporting operational liquidity needs amid expanding asset bases.[F1] Despite this substantial scaling effect on equity base results translate into an approximate return on equity near 7% for FY25—a metric indicative of moderate capital efficiency challenges inherent when absorbing large acquisitions without immediate margin expansion benefits.[F1].[S9]

Management commentary acknowledges these scale effects with strategic emphasis on optimizing capital usage through operational improvements linked directly to integration success plus prudent credit provisioning.

Performance Milestones to Monitor Through 2026

Investor focus should prioritize these key performance indicators relating to successful delivery against stated plans: first-quarter completion of systems conversions paired with branch consolidations; stabilization of loan portfolio risk profiles amidst unfolding macroeconomic developments including CRE exposure tracking; evolution of net interest margin reflecting loan mix adjustments balanced against funding costs contemporaneous with national interest rate policy shifts; realization trajectory of cost savings tied directly to merger synergies.[N10][N11],[S9]

Additional concerns include monitoring changes in credit loss provisions reflecting actual loan performance versus modeled expectations plus continued transparency regarding regulatory capital buffers ensuring dividend payment flexibility will remain intact.[S9] Execution agility coupled with effective communication will remain paramount throughout this transitional phase for sustaining stakeholder confidence.

Disclaimer: This analysis is based solely on disclosed facts from Columbia Banking System's filings and cited news sources without incorporating any subjective investment opinions or forecasts beyond those explicitly stated by company management or public disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments