CorVel Corp Q3 2026 Review: Solid Financials Amid Sector Ambiguity and Oversold Pressure

CorVel reported robust quarterly earnings and maintained strong liquidity despite facing unclear industry classification and oversold stock dynamics.

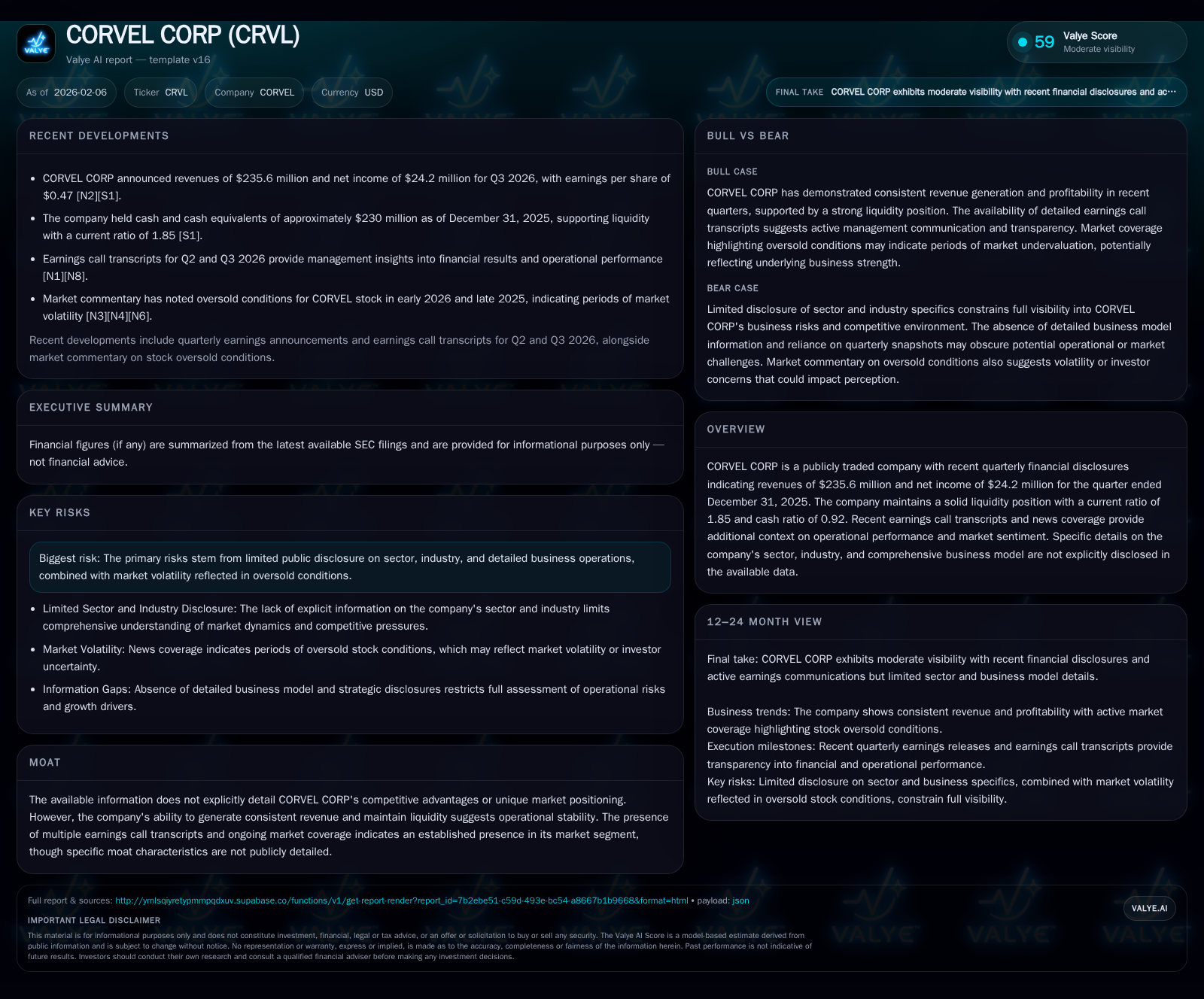

In Q3 2026, CorVel Corp delivered $235.6 million in revenues coupled with $24.2 million in net income, underscoring operational resilience. The company’s liquidity ratios—current ratio at 1.85 and cash ratio near 0.92—reflect a healthy balance sheet. Meanwhile, its stock trades under oversold conditions, a divergence from fundamental strength likely driven by market sentiment and informational opacity. Management commentary highlights cautious optimism but also acknowledges external uncertainties due to limited sector transparency.

Q3 2026 Results: A Closer Look at Revenue and Profitability

CorVel Corp closed the third quarter of fiscal 2026 with revenues of $235.6 million alongside net income of $24.2 million [F1][N2]. These results illustrate a continued trajectory of financial solidity amidst a backdrop of limited disclosure about its specific business lines or industry segments. While detailed year-over-year or quarter-over-quarter comparisons are not explicitly documented in the available transcripts, the absolute dollar figures convey steady operational productivity. This consistency is especially notable given the lack of clarity surrounding the company's primary market positioning.

The earnings call transcript reinforces a narrative of stable profit generation, with management emphasizing controlled cost structures and targeted revenue streams [N1]. The net margin implied by these figures—around 10.3%—suggests efficient conversion of sales into bottom-line results without pronounced volatility.

Liquidity and Financial Health: Unpacking the Numbers

Beyond top-line and profit metrics, CorVel demonstrates compelling financial health indicators through its balance sheet composition. The current ratio at 1.85 (current assets of approximately $463.9 million versus current liabilities near $250.4 million) signals comfortable short-term solvency buffers [F1]. Moreover, the cash ratio hovering close to 0.92 reveals substantial liquid assets readily available without reliance on inventory or receivables.

Such liquidity metrics often denote an organization prepared to meet near-term obligations while retaining optionality for investment or unexpected expenditures [S2]. This financial fortitude forms a crucial underpinning amid any external pressures arising from the broader capital markets or operational uncertainties.

Market Sentiment and Oversold Dynamics on CRVL Shares

Despite these strong fundamentals, CorVel’s stock currently experiences oversold conditions according to multiple Nasdaq analyses [N3][N4]. This disconnect between fundamental data and share price action indicates nuanced market perceptions possibly influenced by broader macro volatility, informational opacity, or investor risk aversion.

Overselling implies that technical momentum has pushed prices below levels justified by commonly used valuation measures, potentially creating mispriced entry points for certain market participants. Analysts note that such divergence is uncommon for companies exhibiting consistent revenue and liquidity strength but can occur when sector identity remains ambiguous or when broader market rotation affects small- to mid-cap stocks disproportionately [N4].

Insights from Management: What the Earnings Call Revealed

Management’s tone during the Q3 earnings call balances confidence with prudence. Executives highlighted operational priorities centered on sustaining revenue growth streams while managing expense discipline [N1]. Phrases like "steady execution" and "focused adaptation to evolving market environments" punctuated discussions.

Nevertheless, subtle caution was evident reflecting uncertainties tied to external factors beyond direct control—particularly those connected to limited industry transparency and challenges in projecting longer-term growth trajectories in an unclear competitive landscape.

The Elusive Moat: Assessing CorVel's Competitive Positioning

One conspicuous gap in public information pertains to CorVel’s competitive moat—or lack thereof within disclosed documents [F1][valye_report_excerpt]. No explicit sector affiliation or proprietary advantage emerged from filings or public narratives.

However, the company’s capacity for consistent revenue generation, paired with mature liquidity management, suggests operational stability that could be interpreted as an implicit form of inertia in its market niche. Without detailed disclosures, it remains speculative to assert deep moat characteristics; nevertheless, such steadiness typically signals some degree of customer retention or efficient service delivery frameworks underpinning ongoing business continuity.

Risk Layers: Transparency Gaps and Market Volatility

Risk factors detailed in recent SEC filings underscore the challenges imposed by limited clarity around CorVel’s exact business model and sector alignment [S2][valye_report_excerpt]. These informational gaps compound difficulties for investors seeking transparent valuation markers or sector comparables.

Moreover, increased equity price volatility potentially linked to these ambiguities enhances susceptibility to market swings detached from intrinsic corporate performance metrics. Oversold technical status exemplifies this phenomenon where sentiment-driven trading pressures overshadow solid financial underpinnings.

Sector and Industry Blind Spot: Challenges for Valuation

The absence of delineated sector or industry identifiers hampers comprehensive analyst coverage and peer benchmarking [valye_report_excerpt][N5]. While broader healthcare sector comparisons might provide some context given partial references by external sources, CorVel’s precise operational footprint remains undefined publicly.

Such obscurity complicates conventional valuation methodologies reliant on industry multiples or growth segment analysis. Consequently, investors must grapple with ambiguity when interpreting CorVel’s relative positioning or long-term scalability prospects vis-à-vis competitors operating within better-defined verticals.

Future Outlook: Navigating Ambiguity in an Unspecific Market Segment

Looking ahead, CorVel presents a dual narrative: financial robustness paired with informational opacity [N1][S2][N3]. Strong liquidity ratios combined with steady earnings offer a foundation capable of supporting resilience through variable market conditions.

Yet sustained ambiguity around sector classification and competitive moats injects uncertainty into growth forecasting and valuation precision. Management’s guidance hints at cautious optimism but underscores prudent monitoring of evolving external variables.

This juxtaposition suggests potential for stable near-term performance balanced against pricing volatility risks rooted largely in perceptual rather than fundamental weaknesses.

Disclaimer: This analysis is based exclusively on publicly available information as of February 2026 and does not constitute investment advice or recommendations regarding any securities discussed herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments