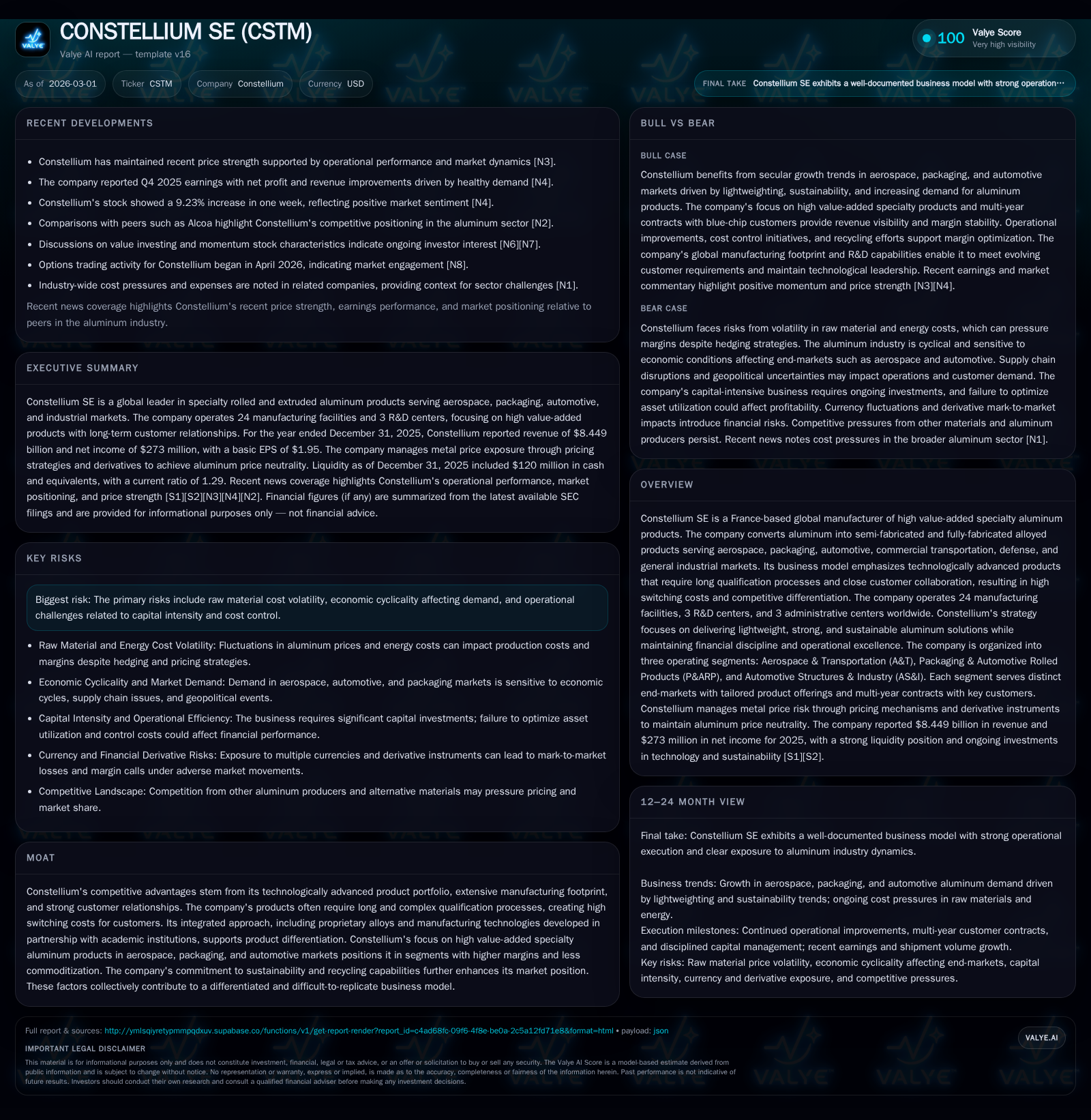

Constellium SE Expands Specialty Aluminum Leadership with Robust 2025 Performance

Constellium’s technology-led specialty aluminum portfolio and disciplined capital allocation powered strong 2025 growth and financial returns.

In 2025, Constellium SE demonstrated solid top-line growth of 8.6% and a remarkable 387.5% surge in net income compared to 2024, driven by operational improvements and favorable end-market dynamics. The company's diverse segment exposure across Aerospace & Transportation, Packaging & Automotive Rolled Products, and Automotive Structures & Industry combined with rigorous cost controls and metal price pass-through strategies helped mitigate input cost volatility. Strong cash flow generation enabled modest capex reduction alongside substantial share buybacks, underscoring disciplined capital management amid ongoing macroeconomic uncertainty.

Enabling Specialty Aluminum Growth: Historical Financial Momentum

Constellium SE reported robust financial results for fiscal year 2025, building on momentum from the previous year. Revenue expanded by approximately 8.6% year-over-year to nearly EUR 5.7 billion, signaling steady demand across its diversified product portfolio [F1]. Net income surged by an extraordinary 387.5%, reaching USD 273 million up from USD 56 million in 2024 [F1], highlighting significant operational leverage as well as the benefits from higher-value specialty product focus.

Operating cash flow (CFO) strengthened markedly by over 60% to USD 489 million while capital expenditures (capex) were curtailed by about one-fifth to USD 330 million [F1]. This capex reduction partly reflects optimized asset utilization and targeted cost management initiatives during a period of cautious macroeconomic outlook [S10]. The interplay of strong cash generation against moderate investments supports ongoing balance sheet flexibility.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 273 | 489 | 330 | +387.5% | ||

| 2024 | 56 | 301 | 413 | |||

| 2018 | 5.7 | +8.6% | ||||

| 2017 | 5.2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 115 | 159 | 28.7 |

| 2024 | 79 | -112 | 7.9 |

| 2018 | |||

| 2017 |

Source: SEC companyfacts cache [F1].

Note: Full revenue figures in EUR available for reference; all % changes calculated per [F1]

Dissecting End-Market Segments: Aerospace, Automotive, Packaging Dynamics

Constellium's business is stratified into three core segments: Aerospace & Transportation (A&T), Packaging & Automotive Rolled Products (P&ARP), and Automotive Structures & Industry (AS&I). In fiscal year 2025, P&ARP remained the dominant driver representing roughly 60% of total revenues yet contributed around 49% of segment adjusted EBITDA, underscoring its scale in canstock, closure stock, foilstock for food/beverage packaging, and automotive auto body sheet (ABS), heat exchanger materials and battery foils [S1][S4][S9].

Conversely, A&T comprised just under one-quarter of revenues but accounted for close to 47% of adjusted EBITDA, evidencing higher margin specialty aerospace alloys including Airware® aluminum-lithium variants tailored for space-defense platforms with long customer qualification cycles delivering structural performance criticalities [S9][S12][S16]. AS&I offered complementary strength principally through extruded crash management systems used extensively in premium European/North American OEMs as well as general industrial large profiles [S7][S9][S16].

Sector context underscores that while cyclicality impacts aerospace with ongoing inventory destocking in some supply chains dampening short-term volumes, packaging demand sustained resilient growth propelled by beverage industry commitments to sustainability and recycling—an area where Constellium’s closed-loop scrap recovery programs provide competitive advantage [N1][S4].[""]

Navigating Input Cost Pressures and Macroeconomic Headwinds

Aluminum raw material pricing sets a critical backdrop given its significant share of COGS. Constellium operates a hybrid pass-through pricing mechanism that closely aligns aluminum purchase costs (based on LME plus regional premiums such as Midwest Premium) with contract revenues through back-to-back customer arrangements or derivative hedges designed to neutralize metal price exposure [S19][S13]. This approach mitigates volatility but requires active market monitoring given recent sharp increases in spot scrap spreads across North America following trade tariff announcements in late-2025 [N1][S20].

Macroeconomic risks include inflationary pressures on energy costs—one of the largest non-metal operating expenses—and geopolitical uncertainties such as tariffs, export restrictions, sanctions, and currency fluctuations impacting foreign exchange dynamics since Constellium’s reporting oscillates between USD and EUR functional bases [N1][S22]. The company leverages currency forwards as part of its hedging strategy to stabilize margins against dollar-euro volatility [S13].

Technology and R&D: Foundation of High Switching Costs and Client Collaboration

Constellium’s moat rests heavily on its differentiated product innovation pipeline executed via three global R&D centers located in Voreppe (France), Plymouth (Michigan), and Brunel University (London) [S10][S4]. Long qualification cycles—often taking years especially in aerospace sectors—entwine customers into collaborative product development models using proprietary alloys like Airware® aluminum-lithium blends.

This innovation extends into joint projects with OEMs where design-for-lightweighting intersects sustainability goals requiring both enhanced formability and crashworthiness performance metrics. Such integration fosters significant barriers to entry for competitors given the technical complexity coupled with the costs borne over multi-year segmentation qualifications enhancing switching costs substantially [S10][S12][N1].

Capital Allocation Excellence: Strong Returns, Cash Flow, and Shareholder Distributions

A hallmark of Constellium’s recent financial discipline is its effective capital deployment balancing reinvestment with shareholder returns. The return on equity approximated 28.7% for fiscal year 2025 calculated as net income divided by average equity [F1], demonstrating attractive profitability leveraging improved margins alongside asset base optimization.

Free cash flow generation—estimated near USD 159 million after subtracting capex from operating cash flow—underscored robust liquidity enabling strategic share repurchases totaling approximately $115 million in fiscal year 2025 versus $79 million in prior year along with continuing dividends consistent with its policy framework prioritizing balanced shareholder value creation amidst disciplined spending on growth initiatives such as R&D and facility upgrades including Muscle Shoals operational enhancements targeting throughput gains [F1][S26][N1].

More than half of the company’s debt maturities lie beyond five years providing manageable leverage with notable liquidity reserves including $120 million cash equivalents and committed revolving credit facilities totaling hundreds of millions supporting short-term needs plus contingent margin call buffers tied to hedge positions [F1][S15][S17].

Strategic Outlook: Balancing Market Demand and Geopolitical Uncertainty

Looking forward into early-2026 management commentary underscores expectations that healthy demand trends will persist particularly supported by supply constraints noted within North American automotive rolled products impacting P&ARP positively while aerospace remains more subdued owing to supply chain destocking effects albeit continuing demand for highly specialized products remains sound [N1][S3].

The overall macroeconomic environment is anticipated to be “relatively stable” but vigilance is maintained regarding trade tariff evolutions regionally that could reverberate through supply chains or raw material input costs necessitating nimble pricing adjustments alongside continued operational efficiency drives targeting cost control gains amid energy pricing fluctuations typical in metals processing industries [N1][S3][S22].

Investor Considerations: What to Monitor Going Forward

Market participants aiming to assess Constellium's trajectory should carefully track several key indicators:

- Quarterly shipment volumes segmented by A&T, P&ARP, AS&I reflecting end-market cyclical shifts or recovery signals especially aerospace backlog reaccumulation post-destocking.

- Aluminum scrap spreads particularly spot vs contract prices affecting input cost pass-through effectiveness.

- Sustained capital allocation discipline visible through continued free cash flow yields supporting buyback programs or dividend growth.

- Updates related to operational excellence milestones at signature facilities such as Muscle Shoals which materially affect throughput efficiency.

- Earnings releases calibrated against guidance cues related to tariff impacts or energy cost escalations that might pressure margins despite structural advantages. These aspects combined frame the near-term execution alongside medium-term growth potential predicated upon Constellium’s unique technological assets combined with end-market diversity positioning the firm favorably relative to peers amid evolving economic landscapes [N2][N3][N6].[""]

This report is based solely on public documents from SEC filings ([F1],[S#]) and market news ([N#]) without any forward-looking investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments