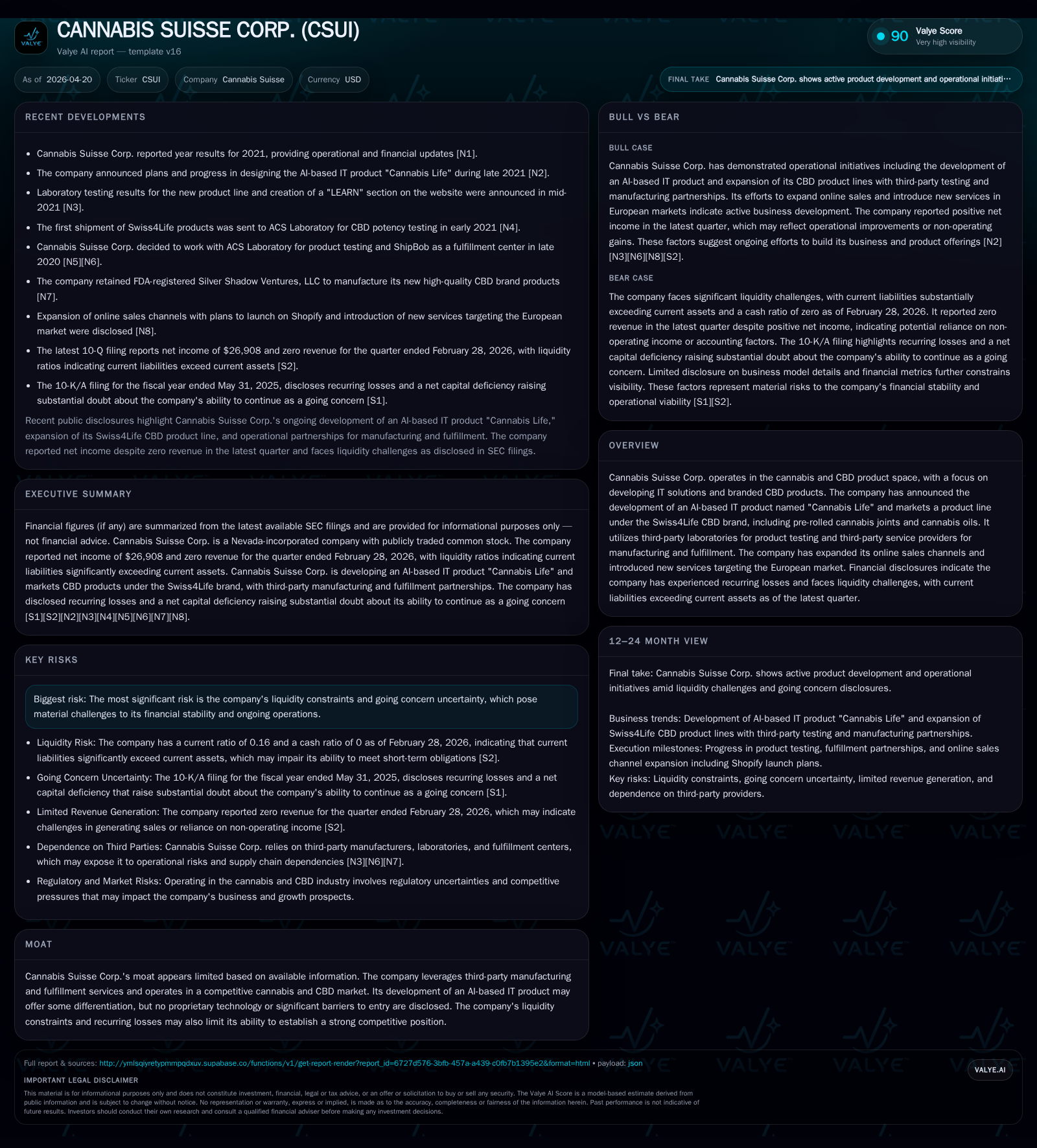

Cannabis Suisse Corp. Faces Operational Challenges While Expanding AI-Driven CBD Solutions

The company’s latest quarter reveals worsening liquidity and sustained losses as it attempts to grow via AI-based product offerings and expanded European sales channels.

Cannabis Suisse Corp.’s Q3 2026 filing underscores its critical liquidity strain with a current ratio of just 0.16 and near-zero cash reserves, exacerbating concerns over its operational viability. The company markets branded CBD products alongside a newly developed AI-driven IT solution aiming to differentiate in a crowded European cannabis market. However, reliance on third-party manufacturing and fulfillment coupled with intense price competition limits margins and strategic control. Growth prospects hinge on successful commercialization of the AI platform and scaling online sales while navigating persistent cash burn and competitive pressures.

Latest Quarterly Update: Deepening Liquidity Stress and Operating Deficits

Cannabis Suisse Corp.’s latest quarterly filing dated April 20, 2026 (10-Q) continues to reveal critical financial distress signaling heightened operational risk. As of February 28, 2026, current liabilities stand at approximately $423,000 while current assets are only around $66,000—yielding a dangerously low current ratio of about 0.16. Compounding this cash flow crunch is virtually depleted cash-on-hand at just $75 [F1]. This liquidity profile sharply constrains the company's ability to cover near-term obligations or invest in business growth.

On the income side, recent operating performance remains weak with continuing losses; the fiscal year ended May 31, 2025 reflected an operating income deficit of roughly -$288,000 alongside a net loss north of -$456,000 [F1]. Although the company modestly increased revenue from approximately $10,000 in FY2023 to $22,500 in FY2025, this top-line expansion has been insufficient to stem persistent negative profitability.

This worsening financial position raises substantial doubt about Cannabis Suisse’s status as a going concern absent new capital infusion or operational restructuring [S8][S9]. The combination of a tight current ratio coupled with recurring operating losses signals limited operational flexibility in the immediate future.

Business Model: Third-Party Manufacturing Meets AI-Driven CBD Product Innovation

Cannabis Suisse operates across two main facets: a branded consumer product line under Swiss4Life and an emerging technology-driven platform called 'Cannabis Life.' The Swiss4Life brand encompasses traditional cannabis-related products such as pre-rolled joints and cannabis oils primarily sold online targeting European marketplaces [S1]. Revenue generation thus centers on product sales within the rapidly expanding but also highly fragmented cannabis and CBD personal wellness segments.

Notably, Cannabis Suisse relies extensively on third-party providers for key parts of the value chain including laboratory testing for product quality assurance as well as contract manufacturing and fulfillment services [S1]. This outsourced model reduces upfront capital expenditures but simultaneously limits direct cost oversight and supply chain control. Such reliance potentially restrains margin expansion versus vertically integrated competitors who can internalize production efficiency gains.

On the innovation front, the company has developed "Cannabis Life," an AI-based IT solution aimed at supplementing its traditional offerings with data-driven tools presumably focused on consumer engagement or supply chain optimization . While this represents an attempt at differentiation within a commoditized marketplace, the extent of monetization achieved by this technology remains unclear given early-stage development and limited disclosure.

Overall, Cannabis Suisse functions as a hybrid between consumer product retailing underpinned by value-added digital services; however, third-party dependencies underscore structural limitations on scalability without significant reinvestment into proprietary capabilities.

Industry Context: Navigating a Crowded European Cannabis and CBD Marketplace

The European cannabis and CBD industry environment is characterized by intense competition marked by numerous small-to-medium players offering largely undifferentiated products amid evolving regulatory frameworks. Cannabis Suisse faces typical industry headwinds such as low barriers to entry combined with variable country-level compliance standards impacting distribution strategies [S1].

Product commoditization exerts downward pressure on pricing power—customers can easily switch among brands given minimal switching costs typically associated with wellness-focused CBD items. In this context, building a durable moat through brand loyalty or unique pricing leverage proves challenging absent patent-protected formulas or exclusivity agreements.

The use of standard third-party laboratories for testing further dilutes product uniqueness since many competitors have access to similar certification services. Additionally, regulatory complexity across Europe mandates nuanced compliance approaches but does not necessarily confer competitive advantage on smaller entities like Cannabis Suisse.

These dynamics collectively position Cannabis Suisse within a fragmented low-margin segment where operational efficiency and customer acquisition via digital channels become critical battlegrounds.

Growth Catalysts: Expansion of Online Channels and AI Product Rollout

To combat industry pressures and stimulate growth despite prevailing liquidity constraints, Cannabis Suisse has strategically expanded its online sales channels providing wider geographic reach into European markets [S2]. Direct-to-consumer e-commerce leverages reduced overheads relative to physical retail while enabling richer customer data collection potentially feeding into their AI platform’s monetization funnel.

The rollout of the "Cannabis Life" AI-based IT product introduces an innovative angle designed to differentiate from competitors primarily selling commoditized goods. Although specifics are sparse regarding functionality or commercial uptake levels thus far, this initiative could evolve into an additional revenue stream or enhance existing product engagement metrics if successfully integrated.

Operationally this dual-channel strategy may improve gross margins—digital sales typically carry lower distribution costs than traditional wholesale or dispensary models—but demands tightened execution against cash-flow limitations .

In summary, these initiatives represent vital growth engines yet remain early stage; true impact on reversing negative earnings trends depends on customer adoption rates and continuous investment capacity.

Challenges Ahead: Market Competition, Cash Burn, and Structural Weaknesses

Several material risks cloud Cannabis Suisse’s near-term outlook. Chief among them is persistent liquidity scarcity posing going concern uncertainties addressed explicitly in management disclosures [S8][S9]. This constraint restricts internal funding for marketing efforts needed to accelerate online channel traction or for scaling proprietary technology development.

The company’s thin balance sheet compounded by recurring operating losses (operating income declined by approximately 12% YoY in FY2025) undermines investor confidence potentially hampering access to favorable financing terms [F1]. Cost structure rigidity stems partly from reliance on third parties where opportunities for internal efficiency gains remain limited without vertical integration.

Furthermore, competitive intensity within Europe’s cannabis/CBD domain compresses pricing power while proliferating substitute options for consumers undermines brand exclusivity. Regulatory shifts pose ongoing compliance risks that could disrupt distribution pathways or alter product approval processes adding volatility.

Collectively these structural weaknesses may cap scalability without substantial reconfiguration either through capital injections permitting enhanced control or strategic partnerships broadening capabilities beyond commoditized offerings.

Milestones to Monitor: Product Development, Revenue Trajectory, and Funding Events

Cannabis Suisse’s near-term viability hinges on several execution-sensitive milestones:

- Quarterly revenue progression indicating whether online channel expansion materially lifts top-line beyond historical sub-$25K annual runs [S2][F1].

- Commercial progress markers related to "Cannabis Life" including user metrics or monetization achievements clarifying value-add beyond pilot phases.

- Cash flow stabilization signals such as narrowing operating deficits or improved current ratio via debt refinancing or equity raises mitigating near-term default risk.

- Any announcements regarding strategic partnerships or proprietary manufacturing investments that might reduce dependence on external providers improving margin outlook.

Close scrutiny over these indicators will provide early insight into potential turnaround trajectories versus entrenched financial stress patterns documented most recently.

Financial Overview: Revenue Trends, Loss Trajectory, and Liquidity Analysis

Historical performance (annual)

| FY | Rev ($) | Net ($) | CFO ($) | OpInc ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 22500 | -456142 | -45112 | -288013 | -25.0% | +61.6% |

| 2024 | 30000 | -1186613 | -45637 | -256937 | +200.0% | -237.5% |

| 2023 | 10000 | -351547 | -163960 | -342682 | +28.7% | -87.1% |

| 2022 | 7770 | -187890 | -32089 | -157155 |

Source: SEC companyfacts cache [F1]. Figures in USD; all sourced from latest available SEC filings[F1]

The data illustrates marginal revenue growth accompanied by deeply entrenched losses across all income levels. Operating cash flows remain steadily negative (~-$45K annually most recent years), eroding capital reserves necessary for solvency maintenance. The balance sheet snapshot as of February 2026 significantly highlights short-term obligation imbalances where current liabilities exceed assets by over sixfold—a dire liquidity situation constraining operational maneuvering [F1].

Despite some improvement in net loss magnitude relative to the prior year (FY2025 showed a narrower deficit than FY2024), sustainable profitability remains elusive especially given revenue declines year-on-year (-25% from FY2024 to FY2025). Lack of meaningful positive free cash flow reinforces urgency for fresh capital or cost restructuring initiatives to preserve enterprise continuity.

Disclosures herein are grounded exclusively upon filings made publicly available through SEC databases as of April 20, 2026 ([S1], [S2], [F1]) supplemented by expert sector analysis reflecting standard market dynamics within European cannabis/CBD industries. No investment advice or forward-looking financial predictions are offered.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments