Swvl’s Strategic Shift to Corporate Transportation Accelerates Geographic Reach and Profitability

Swvl’s latest quarterly results underscore robust revenue growth driven by enterprise contract expansion across key regions, balanced against liquidity and control challenges.

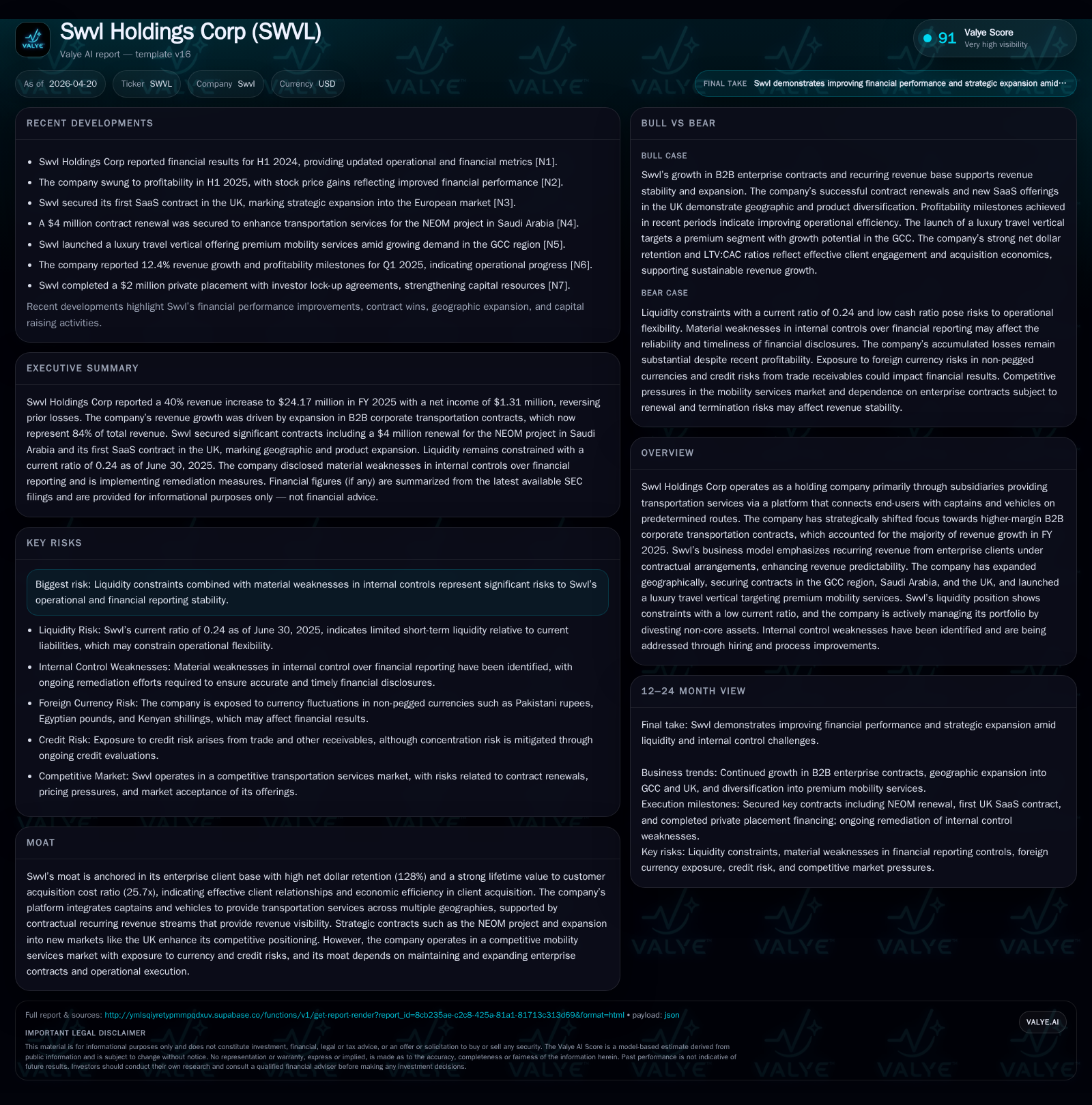

In Q1 2026 filings, Swvl Holdings Corp reported a 40% revenue boost in FY 2025, propelled by a 56% jump in B2B corporate transportation contracts that now dominate its revenue mix. The company’s strategic focus on enterprise clients has enhanced recurring revenues and geographic penetration in the GCC, KSA, and UK markets. However, liquidity remains constrained with a low current ratio and ongoing material weaknesses in internal controls posing operational risks. Swvl is managing these challenges through asset divestitures and new audits, while maintaining strong customer retention metrics reflected in a net dollar retention (NDR) of 128%. Financially, Swvl has achieved positive net income for the first time since 2023, marking a pivotal profitability turnaround.

Q1 2026 Operating Update Highlights: Revenue Surge from Enterprise Contracts

Swvl Holdings Corp’s most recent interim disclosure [S2], coupled with its FY 2025 annual filing [S1], reveals a decisive pivot toward high-margin business-to-business (B2B) corporate transportation contracts that fueled a substantial top-line acceleration. Swvl reported consolidated revenue of $24.17 million for FY 2025, marking a sharp 40% increase from $17.21 million in FY 2024. The lion’s share of this growth stemmed from a striking 56% year-over-year expansion in B2B revenues to $20.27 million, driven both by onboarding new enterprise clients within existing geographies such as Egypt and Saudi Arabia (KSA), and by geographic entry into the United Arab Emirates (UAE).

This wholesale shift away from lower-margin business-to-consumer (B2C) rides—down by 8% to approximately $3.9 million—was a result of strategic route reductions targeting less profitable segments [S1]. The practical effect is twofold: revenue predictability through contract-backed enterprise arrangements, and improved margin sustainability given higher corporate yields per ride.

Geographic expansions have complemented this contract growth; notably, revenue originating from the Gulf Cooperation Council (GCC) region surged by over 120%, reflecting successful penetration into new regional mobility networks [S2]. This expansion strengthens Swvl’s presence beyond traditional emerging markets positioning it competitively alongside regional incumbents.

Swvl's Business Model: Platform Integration and Recurring Revenue Dynamics

Central to Swvl’s value proposition is a digital platform that orchestrates transportation logistics by connecting captains (drivers) operating vehicles along predetermined routes with end users—both individual commuters and corporate clients requiring consistent transit solutions [S1]. The company acts as principal in these transactions under IFRS 15 recognition principles, thereby reporting gross revenues.

The platform’s strategic emphasis has shifted decisively towards enterprise customers who commit via contracts typically spanning one to five years. Approximately 84% of total revenues are now recurring in nature under these agreements [S1], offering greater revenue visibility relative to transactional B2C rides.

Economic efficiency metrics underscore the strength of this model: the lifetime value to customer acquisition cost ratio (LTV:CAC) achieved was an impressive 25.7x on a consolidated basis during FY 2025 [S6]. This means each enterprise client generates nearly 26 times more gross margin over its lifetime compared to what Swvl spends acquiring them—an indicator of sticky relationships supported by contractual switching costs.

Complementing base offerings is Swvl's newly launched luxury travel vertical aimed at premium corporate clientele seeking differentiated mobility experiences—an attempt to capture higher price points and further diversify product mix [S1]. Profitability margins are notably stronger on contract-driven services than on ad hoc B2C rides due to volume commitments and reduced price sensitivity.

Competitive Environment: Positioning in the B2B Mobility Services Market

Within the global mobility landscape focused on enterprise transportation as-a-service, Swvl operates amid intense competitive pressures including incumbent shuttle providers and emergent platform-based integrators leveraging AI-driven routing or fleet management enhancements .

The company's moat hinges on multi-market enterprise client relationships delivering sustained contract renewals at high rates (NDR exceeds 128%) [S6]. Strategic assets such as the NEOM city project contract reinforce barriers to entry given complex contracting processes and required integration capabilities.

Nevertheless, risks persist: exposure to currency fluctuations remains material given operations across unpegged currencies like Egyptian Pounds versus USD-pegged Emirati Dirham [S22]. Credit risk from receivables also warrants monitoring though diversification mitigates single-customer concentration.

Material weaknesses flagged in internal controls over financial reporting highlight operational risk areas that could impact investor confidence or lead to regulatory scrutiny if not remediated promptly [S3]. The competitive position thus depends heavily on execution rigor.

Expansion Frontiers: GCC, KSA, and UK Market Penetration Strategies

Swvl's geographic footprint has widened significantly with dedicated expansions into the GCC countries including UAE, deeper penetration into Saudi Arabia (KSA), plus new initiatives in the UK market [S1][S2]. These expansions bring both opportunity—through access to more stable corporate clients with dollar-pegged payment streams—and complexity stemming from local regulatory environments, logistical infrastructure variances, and currency translation challenges.

Contracts secured in these new regions underpin NDR figures above industry averages: for instance, GCC & UK regions posted an NDR of approximately 135%, evidencing successful upsell/cross-sell activity among existing corporate customers alongside organic growth [S6]. This highlights Swvl's ability to replicate its platform model effectively across diverse regulatory and cultural contexts.

Regulatory hurdles related to licensing requirements for passenger transport operators vary significantly between jurisdictions like Saudi Arabia and the UK; Swvl's capacity to navigate these will be crucial for sustaining growth momentum without incurring compliance penalties or market entry delays .

Growth Enablers and Constraints: Contract Depth versus Liquidity and Controls

Enterprise client onboarding pace remains a primary growth lever supplemented by upselling expanded route coverage or premium services. The rich backlog of signed customer agreements—estimated at $38.2 million including anticipated renewals—is testimony to pipeline strength [S11]. Recurring revenues improve visibility amidst cyclical demand fluctuations common in transportation sectors.

Conversely, Swvl faces notable constraints. Its current ratio hovers around a precarious 0.24—a reflection of limited liquid assets relative to short-term liabilities—underscoring persistent liquidity pressure [F1][S4][S14]. This factor constrains flexibility for aggressive capex or talent acquisition despite modest capital expenditure forecasts tied mainly to office infrastructure enhancements rather than fleet ownership given the asset-light model [S5][S9].

Another critical challenge is operational risk stemming from identified internal control deficiencies regarding accounting knowledge gaps and segregation of duties that were outlined as material weaknesses in its filings [S3]. While management has initiated an audit firm change (from Grant Thornton to Bansal & Co LLP) signaling efforts toward remediation, this ongoing issue poses risks around financial reporting accuracy during scaling.

Strategically rationalizing portfolio assets through divestitures—e.g., Urbvan sale realized proceeds partially reinvested—demonstrates financial discipline aimed at focusing resources on core profitable markets [S8][S12].

Key Catalysts to Monitor: Contract Wins, Internal Controls Remediation, Cash Flow Trajectory

Looking ahead, several execution milestones warrant close observation:

- Announcements of new large-scale enterprise contracts particularly within GCC/UAE or UK markets could accelerate recurring revenue streams further.

- Progress updates on bolstering internal controls framework post external audit transition will be critical for safeguarding governance credibility.

- Cash flow trends driven by working capital management including receivables collection improvement would signal operational gearing out of liquidity pinch [S10][S14].

- Customer retention metrics embedded within NDR evolution remain key early indicators of sustainable demand amid evolving product mix dynamics.

CEO Mostafa Kandil’s signature across regulatory disclosures underscores management accountability during this period of transformation and scale-up efforts [S2][S3].

Financial Performance Snapshot: Revenue Trends, Profitability Turnaround, and Balance Sheet Health

Swvl closed FY 2025 with positive net income of $1.31 million compared with a loss exceeding $10 million in FY 2024—a noteworthy turnaround nonetheless set against aggregate accumulated losses nearing $339 million historically [F1][S1][S7].

Revenue grew robustly by approximately $7 million year-over-year (+40%), reflecting successful execution on strategic repositioning toward enterprise clients:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2024 | 17 | -10 | -24.7% | -436.0% |

| 2023 | 23 | 3 | -55.6% | +102.5% |

| 2022 | 51 | -124 | +34.3% | -187.3% |

| 2021 | 38 | 141 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2024 | 1492.8 |

| 2023 | 51.7 |

| 2022 | -4700.3 |

| 2021 | -157.7 |

Source: SEC companyfacts cache [F1].

General administrative expenses declined by nearly 40%, partially attributable to non-recurrence of discrete stock-based compensations from prior years alongside ongoing cost optimization measures [S21]. Meanwhile selling & marketing spend grew slightly aligned with increased investment into client acquisition channels supporting B2B growth.

Balance sheet liquidity figures remain strained with cash & equivalents modestly under $5 million yet supported by manageable lease liabilities (~$1.48 million total contractual obligations within five years) [F1][S8][S14]. Credit facilities remain underutilized offering some buffer but longer-term financing or equity raises may be necessary if rapid expansion continues without commensurate cash generation.

In summary, financials validate the strategic pivot’s early benefits yet spotlight necessity for vigilant working capital management amid structural operating risks inherent in emerging economies mobility services platforms.

This analysis synthesizes recent quarterly SEC filings alongside annual disclosures up to April 2026 supplemented by forensic examination of financial statements without extrapolation beyond publicly filed data points per policy guidelines.[F1][S1][S2][S3] No investment recommendation expressed; readers should consider their own diligence requirements before forming conclusions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments