Capital Southwest Corp's Strategic Shift with First Out Senior Loan Joint Venture Amid Earnings Stability

CSWC delivers steady Q3 results while unveiling a structured finance JV signaling potential growth and nuanced risk navigation.

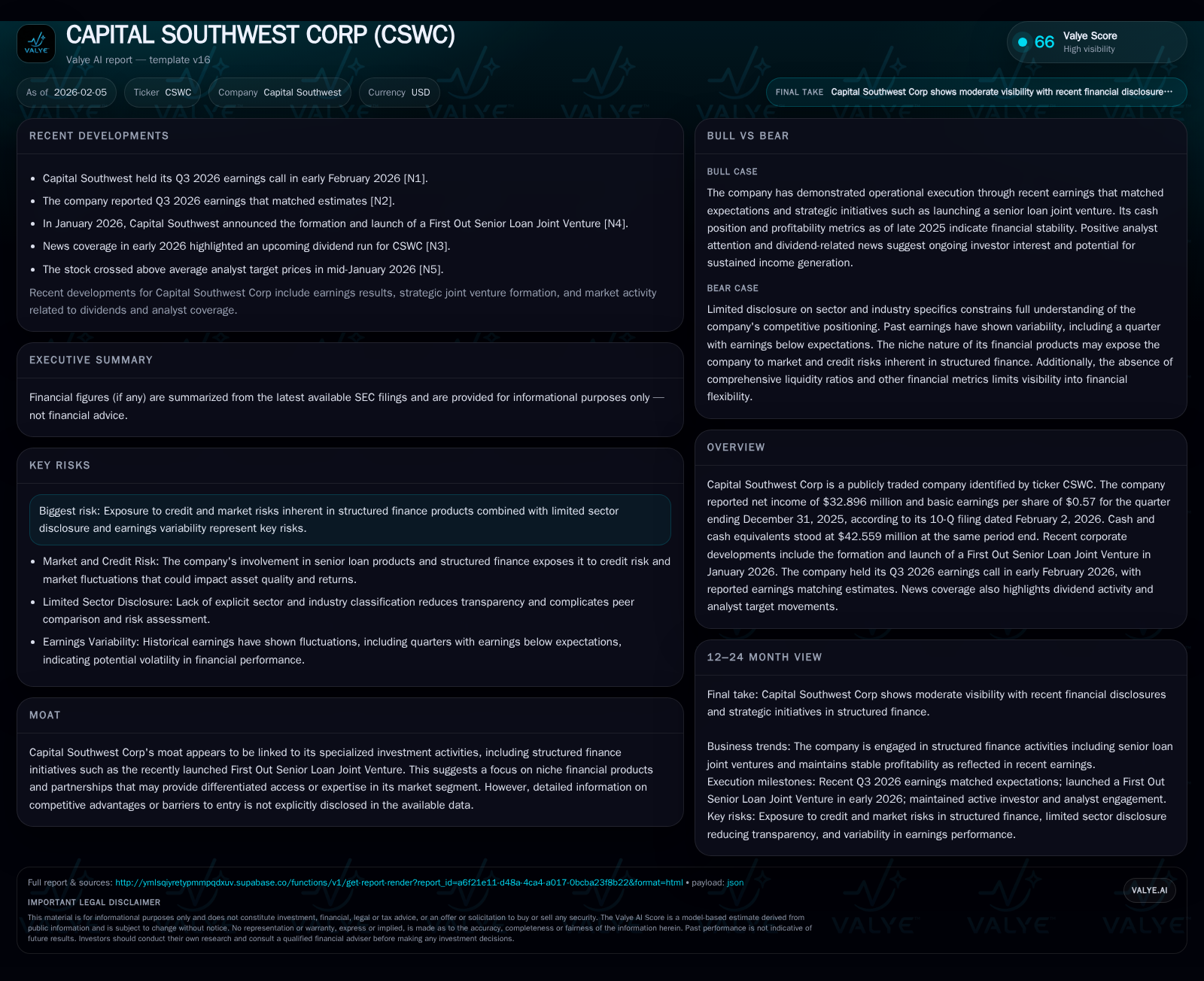

Capital Southwest Corp reported Q3 2026 net income of $32.9 million and EPS of $0.57, in line with expectations, underscoring its steady operational footing. The recent launch of its First Out Senior Loan Joint Venture marks a strategic pivot towards specialized structured credit products, hinting at an attempt to deepen its market niche. Dividend activity and analyst sentiment reinforce the company’s appeal to yield-focused investors, although inherent credit and market risks remain critical considerations. This analysis explores how these developments interplay against CSWC’s modestly articulated moat and capital position.

Resetting Expectations: CSWC’s Q3 Financial Pulse

Capital Southwest Corp (CSWC) entered the release of its Q3 2026 financials as a picture of consistency. Reporting net income of approximately $32.9 million and earnings per share at $0.57, the company met consensus estimates exactly [N1][N2][F1]. These figures act as a reassuring baseline for stakeholders amid broader financial sector uncertainties that have rattled many counterparts. Notably, CSWC ended the quarter holding over $42.5 million in cash and cash equivalents [F1], highlighting ample liquidity, which can serve as a bulwark against volatility or fuel selective growth initiatives.

Management’s commentary during the earnings call maintained a tone of measured confidence, emphasizing disciplined capital deployment and prudent underwriting standards [N1]. The steady execution is significant given CSWC’s identity as a specialty finance entity navigating complex structured products.

Unpacking the First Out Senior Loan Joint Venture: Catalyst or Cautious Step?

Arguably the most consequential development surfaced earlier in January 2026, when CSWC announced the formation and launch of its First Out Senior Loan Joint Venture (JV) [N3]. This arrangement is positioned not just as an incremental expansion but as a deliberate pivot into more granular layers of senior secured lending.

From an industry perspective, "first out senior loans" typically represent tranches that receive payment before others in the capital structure but might carry relatively higher risk or complexity due to loan terms or underlying borrower profiles. By partnering in this JV, CSWC potentially broadens its access to structured credit niches distinct from traditional direct lending or equity stakes [N3].

While explicit operational details remain scant publicly, this move may reflect both an attempt to deepen competitive differentiation — weaving expertise in layered credit instruments — and seek enhanced yield profiles amid persistent low-rate environments [S2]. However, it also introduces nuanced risk exposures anchored in credit quality and deal structure complexity, warranting close investor scrutiny.

Dividend Movements and What They Signal for Income Investors

Dividend whispers have surrounded CSWC lately, culminating in speculation about an upcoming dividend run [N4]. Historically known for steady distributions aligned with generated earnings, the dividend narrative here acts as both signal and tool: signaling management’s intent to maintain shareholder income appeal while reflecting confidence in underlying cash flow sustainability.

For income-focused investors, such dividend constancy amidst strategic expansions like the JV can be reassuring — implying that while CSWC explores new revenue streams, it remains committed to returning capital reliably [N4]. However, investors should watch payout ratios carefully relative to evolving earnings volatility stemming from novel investment vehicles.

Analyst Sentiment: Crossing New Thresholds

External market observers appear increasingly upbeat toward CSWC following recent developments. The company's crossing above average analyst price targets indicates a shift toward valuation optimism [N5]. Analysts are likely factoring in not only baseline earnings stability but also growth prospects from ventures like the First Out Senior Loan JV.

This elevation in sentiment subtly underscores how strategic innovation can recalibrate external perception — shifting CSWC from perceived yield play toward potential total return opportunity. Still, analyst revisions should be contextualized within the broader landscape of specialty finance firms where regulatory changes and credit cycles often temper exuberance.

Risk Factors in the Spotlight: Navigating Credit and Market Complexities

The complexities embedded within structured finance are front and center among CSWC’s identified risks [S2]. Credit risk — particularly linked to borrower defaults or deterioration in loan collateral quality — looms prominently given exposure through layered senior loan positions.

Market risk compounds these concerns; volatility in interest rates or secondary loan markets can affect valuations unpredictably. Earnings variability linked to mark-to-market adjustments or realized losses further accentuates uncertainty.

Importantly, disclosures stress these risks candidly without alarmism but underscore that returns are far from simplistic or guaranteed—reiterating that intricate credit structures demand both rigorous internal oversight and informed external appraisal.

The Moat Mystery: Evaluating CSWC’s Niche Edge

CSWC’s moat — its sustainable competitive advantage — is enigmatic yet tentatively identifiable through its specialized investments. The launch of the joint venture epitomizes this dynamic: pursuing niche market segments that require specific underwriting competencies, relationship networks, or structuring capabilities unavailable broadly within commoditized lending markets.

Absent detailed public data on barriers such as proprietary deal flow or exclusive syndication rights, the moat appears more conceptual than structural [valye_report_excerpt]. Nonetheless, successfully managing complexity in bespoke senior loans could function as a differentiator if coupled with disciplined risk management.

This specialization may afford CSWC resilience against commoditization pressures but equally may limit scaling agility compared to larger financiers with diversified platforms.

Cash Position and Capital Allocation: A Balance Sheet Snapshot

Liquidity strength remains an anchor point for CSWC’s operational flexibility. Maintaining roughly $42.6 million in cash equivalents at quarter-end equips management with optionality—enabling opportunistic investments or buffers against short-term adversities [F1][S2].

Capital allocation decisions amid launching specialized joint ventures will be pivotal going forward. Whether this cash reserve supports incremental JV funding needs or other portfolio diversification strategies will shape both near-term results and longer-term capital structure health.

This financial cushioning also tempers some risk concerns by signaling preparedness rather than overextension at a key strategic juncture.

Strategic Outlook: Where Does CSWC Go From Here?

Synthesizing these threads presents a portrait of a company balancing stable income generation with tactical transformation. Q3 earnings affirm operational steadiness; meanwhile, the First Out Senior Loan Joint Venture embodies calculated exploration into advanced structured credit domains where differentiated know-how might translate into incremental yield enhancement [N1][N3][valye_report_excerpt].

Dividend signals and analyst upward target revisions collectively endorse confidence in management's strategy execution ([N4],[N5]). Yet embedded credit market risks caution against complacency—this is not a linear trajectory but one requiring nimble governance and vigilant risk controls.

Looking ahead, CSWC's ability to articulate clearer competitive moats around these niche endeavors and demonstrate consistent performance within them will govern whether this pivot crystallizes into sustained differentiation versus episodic initiative.

In sum, Capital Southwest stands at an inflection point where stable footholds meet emergent ambitions—a blend compelling enough for attention but demanding comprehensive evaluation across financial resilience, strategic coherence, and risk discipline.

This analysis is informational only and does not constitute investment advice or endorsement.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments