Curbline Properties: Navigating Convenience Real Estate Through Early 2026’s Retail and Economic Currents

Curbline’s focused niche on curblines convenience centers offers a resilient edge amid inflation and occupancy headwinds in the retail property sector.

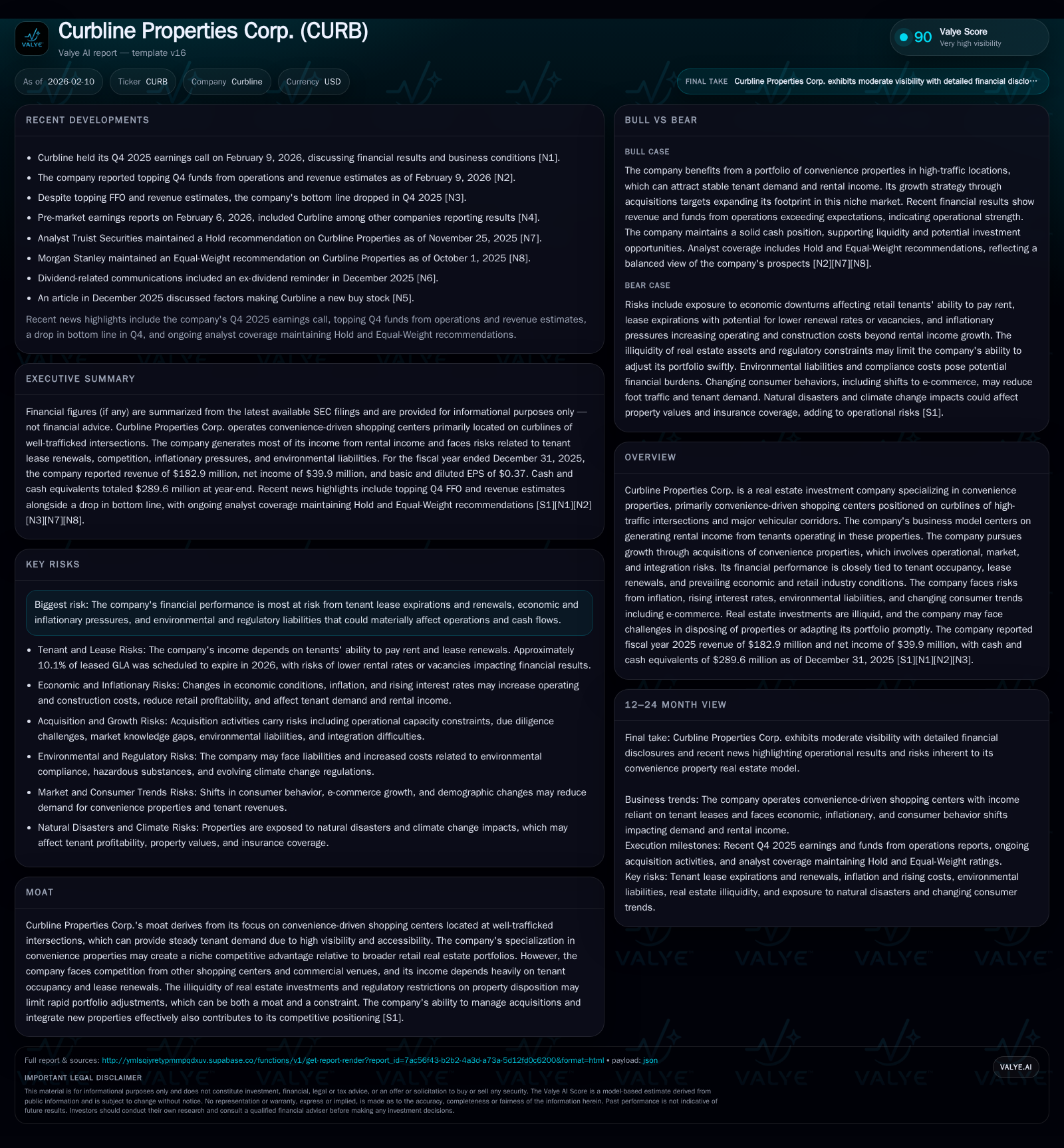

Curbline Properties Corp. operates a distinctive portfolio of convenience-driven shopping centers positioned at high-traffic curblines, underpinning a durable competitive moat. Despite industry-wide pressures such as rising inflation, interest rates, and shifting consumer patterns, its Q4 2025 earnings revealed revenue and funds from operations surpassing estimates, though net income faced some contraction. Tenant lease renewals and occupancy remain focal risks to cash flow continuity, while acquisition pursuits are tempered by integration challenges and capital cost inflation. The company’s strategy balances an entrenched advantage in prime location retail real estate with the inflexibility posed by illiquid assets and regulatory constraints. Looking ahead into 2026, cautious optimism prevails as Curbline navigates environmental liabilities and broader macroeconomic uncertainties that shape its growth trajectory.

Niche Focus: The Strategic Edge of Curblines

Curbline Properties owns a distinct corner of the commercial real estate world—a portfolio anchored exclusively on convenience-driven shopping centers placed on busy curblines intersecting major traffic corridors. These locations serve as magnets for retailers seeking visibility and accessibility that directly translate into foot traffic. This strategic positioning varieties Curbline from broader retail portfolios filled with more commoditized or sprawling retail assets. The company’s moat emerges from this precision focus: tenants covet these curblines for their persistent draw, enabling steady rental demand that buffers against wider retail sector fluctuations.

Yet this moat resembles a double-edged blade. While the well-trafficked curblines offer competitive defense against less visible centers, they do not immunize Curbline from the broader competitive arena brimming with alternative venues vying for retailers. Moreover, such specificity limits agility; repositioning or diversifying away from this narrow segment demands heavy capital redeployment or incremental acquisitions rather than nimble asset swapping. Thus, this niche both fortifies Curbline’s standing and constrains its tactical flexibility [S1].

Earnings That Defy Retail Headwinds

Against a backdrop of mounting inflationary pressures and retail sector uncertainty during Q4 2025, Curbline delivered financial results that bucked some industry trends. The company surpassed consensus estimates for both revenues and funds from operations (FFO), signaling robust top-line momentum from its rental income streams [N2][F1]. Reported revenue reached approximately $183 million by year-end, underpinned by stable rent collections from tenants occupying these coveted curblines.

However, net income contracted somewhat compared to prior periods—as covered in reports—reflecting perhaps higher operating costs or non-cash charges impacting the bottom line [N4][F1]. This bifurcation between revenue strength and diminished net earnings underscores underlying cost pressures squeezing margins even as core operations hold steady.

Importantly, the earnings call transcript clarifies management’s pragmatic tone emphasizing cautious optimism grounded in strong rent roll performance but tempered by anticipated expense inflation—including taxes and utilities—and ongoing tenant renewal negotiations [N1]. The rhythmic pulse of traffic flows mirrored in these results captures a business navigating steady lanes amid bumpier economic roads.

Tenant Dynamics: Occupancy and Lease Renewal Risks

A critical pivot influencing Curbline’s near-term financial stability revolves around tenant lease expirations—a substantial fraction (roughly 10.1% of total leased gross leasable area) is poised to expire during the current year [S1]. Lease renewal outcomes here will significantly sway occupancy levels and thus rental income consistency.

Renewal rates may face downward pressure in light of evolving economic conditions that curb tenants’ willingness or capacity to sustain rents at prior levels. Should select tenants opt against renewal or face solvency struggles—risks heightened by sector-wide consumer discretionary spending trends—vacancies could rise.

Re-letting vacated spaces may entail downtime coupled with capital expenditure commitments for renovations or tenant-specific buildouts—the consequent gaps threaten cash flow predictability. This tenant turnover dynamic represents more than just operational background noise; it forms a crucial challenge demanding vigilant leasing strategies to maintain portfolio health [S1].

Inflation and Interest Rate Pressures on Growth Plans

The empire of curblines does not expand unaffected by macroeconomic crosswinds. Inflation infuses upward pressure on construction costs when adding new properties or refurbishing existing ones—materials become pricier; labor shortages can delay projects; supply chains remain vulnerable—all swelling capital requirements beyond initial projections [S1].

Simultaneously, rising interest rates exacerbate borrowing costs tied to acquisition financing or general corporate debt servicing. This tighter capital cost environment chills appetite for aggressive portfolio expansion even when attractive properties surface.

Retail-sector profitability sagging under consumer spending caution may also blunt landlords’ ability to raise rents sufficiently to offset escalating expenses. Together these forces compress margins and can slow growth trajectories despite management’s focus on opportunistic acquisitions within their niche domain [S1].

Acquisition Strategy and Integration Challenges

Growth through acquisitions remains at the heart of Curbline’s expansion playbook—adding complementary convenience properties to augment footprint along key intersections enhances scale benefits.

However, each addition arrives bundled with integration complexity risks; assimilating new assets involves aligning property management standards, tenant services, maintenance protocols, and local market dynamics—mismatches can erode expected returns.

In today’s more constricted lending environment marked by higher interest rates, deal valuations also require greater scrutiny to ensure accretive outcomes rather than value dilution. The company must weigh acquisition prospects against operational risks lest growth ambitions morph into resource-draining endeavors lacking swift payoff [S1].

Portfolio Liquidity and Regulatory Constraints

Real estate’s very nature cements liquidity limitations. Curbline confronts these constraints squarely—shifting out of or repositioning properties swiftly is hindered by regulatory frameworks governing commercial property transactions plus inherent market friction.

Such impediments serve as moat components protecting steady income streams by deterring impulsive portfolio churn which might destabilize tenant relations. Yet simultaneously this illiquidity forms a bottleneck restricting nimble responses to shifting market landscapes or sudden tenant defaults.

This duality accentuates the company’s strategic balancing act: safeguarding predictability at some cost to flexibility—a tension embedded deeply in real estate investment fundamentals but accentuated here due to niche concentration [S1].

Navigating Environmental and Operational Risks

Amidst traffic signals of economic variables lurk environmental factors—a less visible but material dimension affecting property valuations and operating costs.

Potential environmental liabilities tied to land usage history or compliance burdens impose financial uncertainties requiring ongoing vigilance. Remediation obligations could arise unpredictably inflating maintenance budgets or impairing asset appeal to prospective tenants.

Operationally, steadily climbing expenses spanning property taxes, utilities, insurance premiums, repairs also weigh heavily on margins. Management must therefore calibrate budgets carefully ensuring upkeep standards do not erode longer-term asset viability while containing cost escalations within sustainable bounds [S1].

Analyst Perspectives and Market Sentiment Shifts

Despite external headwinds coloring some cautionary tones across real estate sectors generally, recent analyst activity highlights pockets of endorsement specifically toward Curbline’s strategy.

Wolfe Research elevated its outlook on the company early in 2026 citing confidence in the differentiated approach anchored by convenience-oriented shopping centers – an endorsement signaling market respect for Curbline’s targeted model amid broader retail volatility [N5].

Such upgrades inject positive sentiment counterbalancing cautious narratives enabled by transparency around risk considerations voiced during earnings discussions.

What Lies Ahead: Outlook Into 2026

Looking forward into 2026 reveals a terrain marked by opportunities warmly lit but shadowed by complexities stemming from inflationary currents, evolving consumer behavior amid rising e-commerce prevalence, occupant churn risk, plus regulatory constraints surrounding asset fluidity.

Curbline enters this conjuncture leveraging advantages rooted in curated location selection yet recognizing the tightrope walked between growth aspirations and operational pragmatism laid bare during recent quarters [S1][N1].

Success will likely pivot on deft execution managing tenant relationships closely to maximize renewals while tactically calibrating selective acquisitions mindful of inflated costs. Balance will be key—as it often is where highways meet at bustling curbsides—charting courses that blend stability with calculated ventures amidst shifting economic patterns.

Disclaimer: This analysis is based solely on publicly available information as cited without predicting future performance nor offering investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments